The fastest way to remove an “Amount on Hold” in HDFC Bank is to clear any pending EMI, credit card dues, ECS payment, or charges linked to your account.

After payment, HDFC usually releases the blocked amount automatically within 24–48 hours.

If the hold still remains after two days, contact HDFC support or visit your home branch for manual verification.

📞 HDFC Quick Support

1800 2600 or 1800 1600

For customers abroad:

+91 22 6160 6160

📌 Quick Steps to Release Hold Amount

💡 Real Customer Example: One customer missed an EMI auto-debit by one day. After manually paying the EMI, the hold amount disappeared automatically within 24 hours even though support initially estimated 3 working days.

⚠️ Important: If the hold amount is linked to suspicious transactions, cyber complaints, or compliance checks, HDFC may require branch verification before releasing the funds.

📌 Escalation Help

📖 Read below: Why HDFC shows “Amount on Hold” and how to check hold details in the HDFC app.

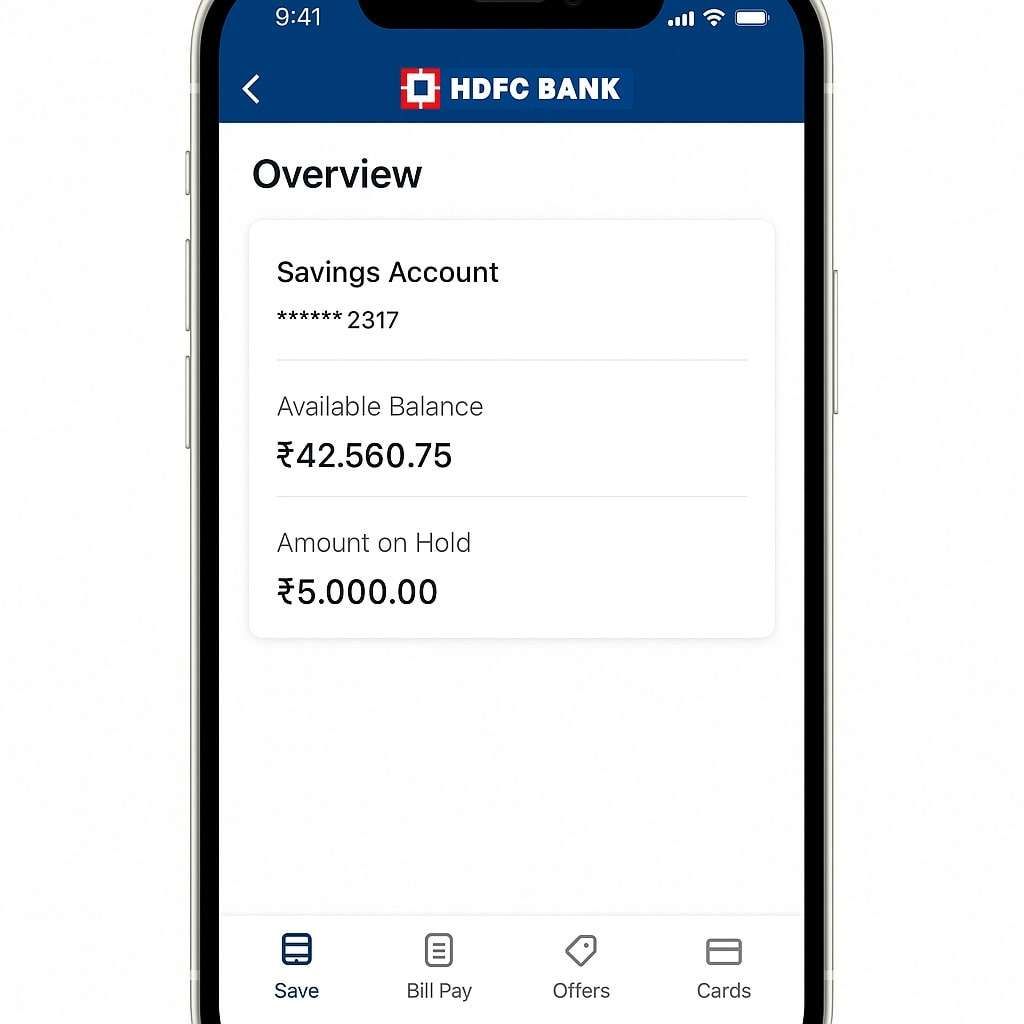

How to Check the Hold in the HDFC App

Here’s the exact place you will find it, just using your phone –

- Open your HDFC Mobile Banking app and log in using 4-digit mpin or Face ID.

- Tap on “Save” at the bottom.

- Choose your Savings or Salary Account.

- Tap on “Show Account Details”.

- You will see a line that says “Amount on Hold.”

That number is the exact amount you can not use right now — even if your total balance looks higher.

Why Does This Amount on Hold Happen in HDFC?

HDFC Bank can place a lien for different reasons — sometimes for pending dues and sometimes for temporary verification or system checks. To understand it better, liens are mainly divided into two types:

1. Due Related Holds — When You Owe the Bank Something

These holds happen when there’s some charge, fee, or payment pending on your account. Here are the top real reasons HDFC does this:

- Late EMI payment: Even a 1-day delay can temporarily freeze the amount until payment is updated.

- Credit card or debit card EMI dues: Missed or delayed EMI payments may create a hold on the account balance.

- ECS or Auto-NACH bounce: Failed auto-debit payments due to low balance can trigger a lien for recovery.

- Negative balance recovery: If the account was negative earlier, the bank may adjust pending charges from new deposits.

- Debit card annual fee: Pending debit card maintenance charges can appear as a hold amount.

- Cheque return or stop payment: Money may stay blocked until cheque processing is completed.

- Pending service charges: SMS fees, penalties, or other small charges may create temporary holds.

- FD or overdraft linkage: Sweep-in FD or OD-linked accounts can show temporary internal holds.

- KYC or compliance issue: Suspicious transactions or expired KYC may trigger a regulatory hold until Re-KYC is completed.

2. Common Temporary Holds in HDFC Bank — When It’s Not Your Fault

These holds are automatic and usually clear within 24 to 48 hours without you doing anything.

- Pending UPI or card transaction: Failed UPI or POS payments may keep the amount on hold until reversal is completed.

- Cheque under clearance: Deposited cheque amounts stay on hold until the cheque clears.

- Refund processing: Refunds from apps like Amazon or IRCTC may remain on hold for some time before credit.

- ATM cash reversal: If cash was not received but the account was debited, the amount may stay on hold for 1–2 days before reversal.

- Transaction timeout or verification: Sometimes the banking system keeps money on hold for extra verification or failed transaction sync.

- Internal bank maintenance: During backend updates or maintenance, temporary holds may appear on balances.

- Merchant pre-authorisation: Hotels, petrol pumps, or travel websites may temporarily block money until the final bill is settled.

How Long Does Hold Amount Take to Clear?

The time depends on the reason for the hold. Some holds clear automatically, while legal or cyber-related cases can take much longer.

| Reason | Expected Time | What You Should Do |

|---|---|---|

| Cheque clearing | 1–2 working days | Wait for bank processing |

| EMI or credit card dues | 48–72 hours | Pay pending amount |

| KYC update | 2–10 working days | Complete Re-KYC or Video KYC |

| Failed UPI/card transaction | 5–7 days | Wait for automatic reversal |

| Merchant refund | Up to 21 days | Wait for refund settlement |

| Cybercrime or legal hold | Weeks or months | Contact cyber cell or authority |

Tips to Resolve Faster

- After paying dues, contact HDFC Bank customer care or branch with payment proof.

- Video KYC is usually faster than branch document submission.

- For cybercrime holds, the bank cannot remove the lien without official clearance from the investigating authority.

Frequently Asked Questions

My UPI keeps failing at shops even though the balance shows full — what should I do?

Try sending ₹1 first. If it fails, check “Amount on Hold” in the HDFC app. Even ₹100 on hold can block a ₹10 payment. First, reset your UPI PIN if the amount on hold is Zero and try to set it again using the ATM, or contact your HDFC customer care for any technical errors.

Can I withdraw cash if there’s an amount on hold?

No. ATM only lets you withdraw from your available balance, not your total. Wait till the hold clears — or call support if it’s stuck long. The hold amount does not work on credit, debit, or withdrawal online or offline.

Is “Amount on Hold” counted in my minimum balance for HDFC savings accounts?

Yes. HDFC counts the total balance, not the available balance. Even if ₹2,000 is on hold, it still counts toward the minimum balance, so you won’t be charged unless the total drops below the limits.

How long can HDFC legally keep my money on hold without explanation?

Usually, 24–48 hours for system holds. If it crosses 3 working days, the branch staff must explain the exact system remark. RBI norms require banks to disclose the reason on request.

Does “Amount on Hold” affect interest calculation on my savings account?

No. Interest is calculated on the end-of-day total balance. Even if ₹5,000 is blocked, HDFC still pays savings interest on that amount during the hold period.

Can a merchant or hotel hold money longer than expected in HDFC?

Yes. Pre-authorisation holds depend on merchant release, not HDFC. Hotels and fuel pumps may keep amounts blocked for 7–14 days unless they manually close the transaction.

Will closing my EMI or credit card immediately remove the hold?

Payment clears first, but the hold removal depends on backend sync. In most real cases, the hold drops within 12–36 hours, even though executives quote “up to three working days.”

What’s the fastest real-world way to confirm the exact reason for a hold?

Ask your Home OR nearest branch staff for the system narration or hold code. It shows the internal reason in seconds—much faster than guessing. Carry a debit card or customer ID for instant access.

Hope you liked the content. Explore smart options below 👇

🔥 Recommended