A cheque bounce happens when a bank refuses to process a cheque and returns it unpaid. Common reasons include low balance, signature mismatch, account closure, expired cheque, stop-payment request, or pending KYC issues.

If you are new to banking, first understand how a cheque works in India .

📌 Most Common Reasons for Cheque Bounce

Important Legal Point: A cheque bounce itself does not immediately make someone a criminal. Under Section 138 of the Negotiable Instruments Act , legal trouble usually starts only when the payment is still not made after receiving a formal legal notice.

Read below: Section 138 punishment, cheque bounce notice rules, legal timeline, How to Escape, and How to File a Cheque Bounce.

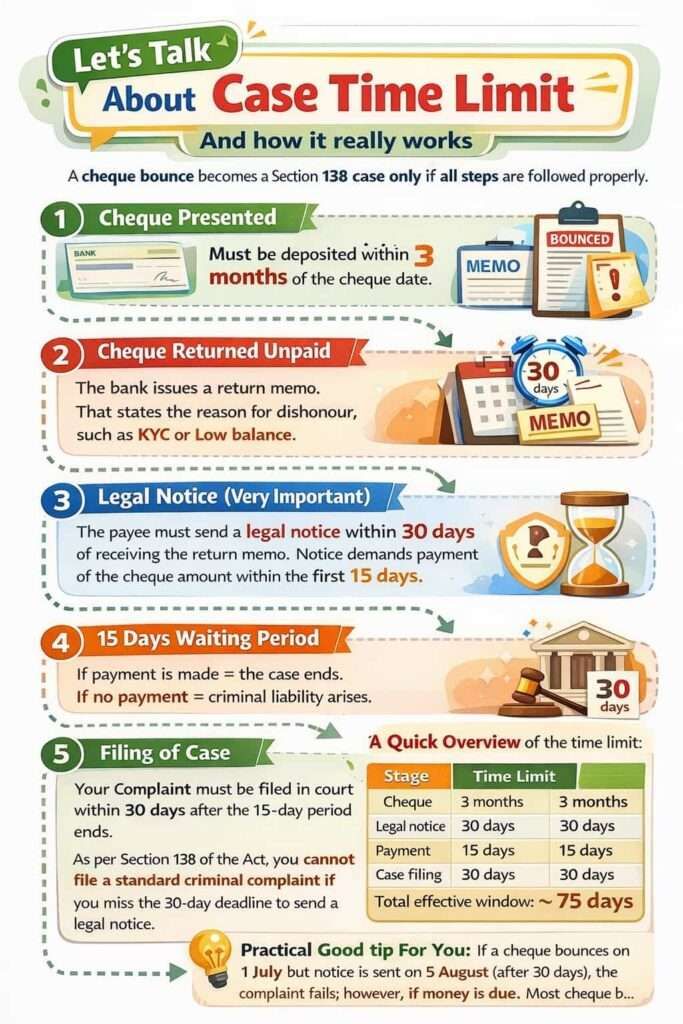

Cheque Bounce Case Time Limit Explained

A cheque bounce becomes a Section 138 case only if all steps are followed properly.

1. Cheque Presented

- Must be deposited within 3 months of the cheque date.

2. Cheque Returned Unpaid

- The bank issues a return memo. That states the reason for dishonour, such as KYC or Low balance.

3. Legal Notice (Very Important)

- The payee must send a legal notice within 30 days of receiving the return memo.

- Notice demands payment of the cheque amount within the first 15 days.

4. 15 Days Waiting Period

- If payment is made = the case ends.

- If no payment = criminal liability arises.

5. Filing of Case

- Your Complaint must be filed in court within 30 days after the 15-day period ends. As per Section 138 of the Act, you cannot file a standard criminal complaint if you miss the 30-day deadline to send a legal notice. This timeline is mandatory.

💡Practical Tip: If a cheque bounces on 1 July but notice is sent on 5 August (after 30 days), the complaint fails; however, if money is due. Most cheque bounce cases are lost not on merit, but on delay.

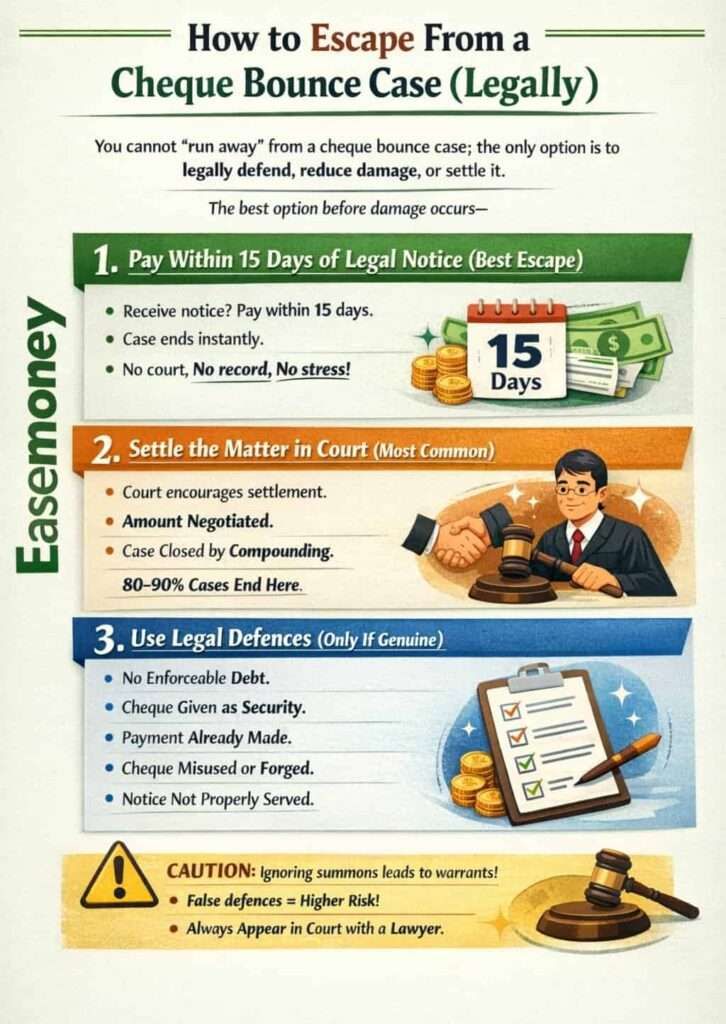

How to Escape From a Cheque Bounce Case (Legally)

The direct answer I can give is – You cannot “run away” from a cheque bounce case; the only option you have is to legally defend, reduce damage, or settle it. The best option before damage occurs –

1. Pay Within 15 Days of Legal Notice (Best Escape)

- Once you receive a legal notice, you get 15 days, arrange the amount and pay it

- If you do it within 15 days, your case ends instantly and automatically

- This is the safest and cleanest exit. No court, no record, no stress.

2. Settle the Matter in Court (Most Common)

Even after the case is filed:

- The court encourages compromise, which is still the finest and least damaging state.

- You can ask for the Amount negotiated

- The case is closed through compounding

- In india, 80–90% cheque bounce cases end this way

3. Use Legal Defences (Only If Genuine)

You may escape conviction if you prove:

- No legally enforceable debt

- A cheque was given as security

- Payment already made

- Cheque misused or forged

- Legal notice not served properly

- Timeline not followed

Note: Accept any of the three, because ignoring summons leads to warrants, or False defence can be higher risk later. If you choose 2 option, appearing through a lawyer is enough. avoid non-Appearance.

If someone’s cheque bounced to you:

1. How to File a Cheque Bounce Case (Step-by-Step)

- 1 Step: Your bank will issue a return memo with the reason why it was dishonoured.

- 2 Step: You have 30 days. You can send a legal notice to him or the firm. It allows 15-day demand payment. You can talk to a professional lawyer for that.

- 3 Step: Now, wait for 15 days for the payment has been received or not. If not, it leads to offence.

- 4 Step: You have to file a case against the company via the Magistrate Court and prepare your documents, such as the original cheque, Bank return memo, proof of delivery and legal notice photocopy.

- 5 Step: The Court will issue a summons, and your accused needs to appear with a lawyer.

- 6 Step: Your court may ask for a Settlement encouraged and a Trial only if the settlement fails

2. Typical Court and Advocate Fees

cheque bounce case under Section 138 is a criminal complaint, so court fees are minimal.

| Item | Approx Cost |

|---|---|

| Complaint filing | ₹10 – ₹200 |

| Affidavit & stamps | ₹50 – ₹300 |

| Misc. charges | ₹100 – ₹500 |

Total court fees usually below ₹1,000 and your Cheque amount does NOT affect court fees

3. Advocate Fees

| Stage | Fees (₹) |

|---|---|

| Legal notice drafting | 1,500 – 5,000 |

| Reply to notice | 2,000 – 6,000 |

| Filing case (complainant) | 5,000 – 20,000 |

| Defending accused (trial) | 10,000 – 50,000 |

| Settlement drafting | 3,000 – 10,000 |

Most lawyers push for early settlement because it saves costs for both sides. The fee is subjective and depends mostly on the cities and all process.

What Changed in Cheque Bounce Law in India?

By 2025, courts and banks started treating cheque bounce cases as a system overload issue, not just a legal dispute. Millions of cases are already pending, so the focus is now on faster settlement and quicker recovery.

Major Changes and Updates

- Cheque bounce cases under Section 138 can still lead to up to 2 years of jail or a penalty up to double the cheque amount.

- Courts now take stricter action against repeat cheque bounce offenders.

- Some banks may temporarily restrict account operations in repeated default cases.

- Legal notices can now be sent through email and WhatsApp in many cases.

- Online filing and virtual hearings have made the process faster.

- Courts try to complete many cheque bounce matters within 90 days where possible.

- Courts can order up to 20% interim compensation during the case.

- Delaying settlement now increases legal costs and penalties.

- Banks usually send cheque bounce alerts within 24 hours, reducing “late information” excuses.

Cheque Bounce vs Civil Recovery: What’s the Actual Difference?

Unlike what many people think, a cheque bounce case is not just about getting money back — it is a criminal pressure mechanism, while civil recovery is different.

Let’s break it clearly:

| Factor | Cheque Bounce Case (Section 138) | Civil Recovery Case |

|---|---|---|

| Nature | Criminal case | Civil case |

| Goal | Force payment via legal pressure | Recover money through court decree |

| Time | Faster (if done correctly) | Slow (can take years) |

| Jail Risk | Yes (rare but possible) | No jail |

| Settlement | Very common (80–90%) | Less flexible |

Real Insight –

- Many smart businesses use both strategies together:

- First → File cheque bounce case (to create pressure)

- Then → Parallel civil suit (to secure recovery legally)

- This dual approach increases chances of recovery significantly.

Practical example: If someone owes ₹2 lakh and cheque bounces, filing only civil case = slow recovery But cheque bounce + legal notice = faster settlement chances

Tip: If amount is large (₹5 lakh+), always consider both routes after talking to a lawyer.

Frequently Asked Questions

Can a cheque bounce case be decided in favour of the accused?

Yes, courts do dismiss cheque bounce cases when timelines are violated, notice is defective, the debt is not legally enforceable, or evidence rebuts statutory presumptions. Procedure matters more than sympathy in such cases.

How serious is a cheque bounce case in India, realistically?

Legally it’s a criminal offence, but practically courts focus on recovery and settlement. Jail is rare. Seriousness increases only when notices, summons, or court directions are repeatedly ignored.

Is there any minimum or maximum cheque amount for a cheque bounce case?

No. The law sets no minimum or maximum amount. Even a ₹500 cheque can lead to a case if legally enforceable, while a ₹1 crore cheque can fail if procedure is defective.

Can a cheque bounce case be cleared without going through full trial?

Yes, and most are. Payment within notice period, settlement during court proceedings, or compounding even after conviction can lawfully close the case without a prolonged trial.

How is a cheque bounce case in Dubai different from India?

Cheque bounce in Dubai involves local criminal and civil laws, not Indian law. Clearing it usually requires settlement, fines, or court compliance there—Indian courts cannot resolve UAE cheque disputes.

What happens if the accused lives in a different city or state?

Distance doesn’t stop proceedings. Appearance through a lawyer is usually sufficient. Courts now allow practical measures like dasti service and online payments to reduce unnecessary travel.

Can police directly arrest someone in a cheque bounce case?

No, police cannot directly arrest in cheque bounce cases because it is a complaint-based offence. Arrest happens only if court orders are ignored repeatedly, like non-appearance or warrant issuance.

What happens if cheque bounce case is filed after delay by mistake?

If timelines like 30-day notice or filing window are missed, the case can be dismissed technically. However, you can still recover money through civil recovery or fresh legal strategy depending on facts.

Hope you liked the content. Explore smart options below 👇

🔥 Recommended