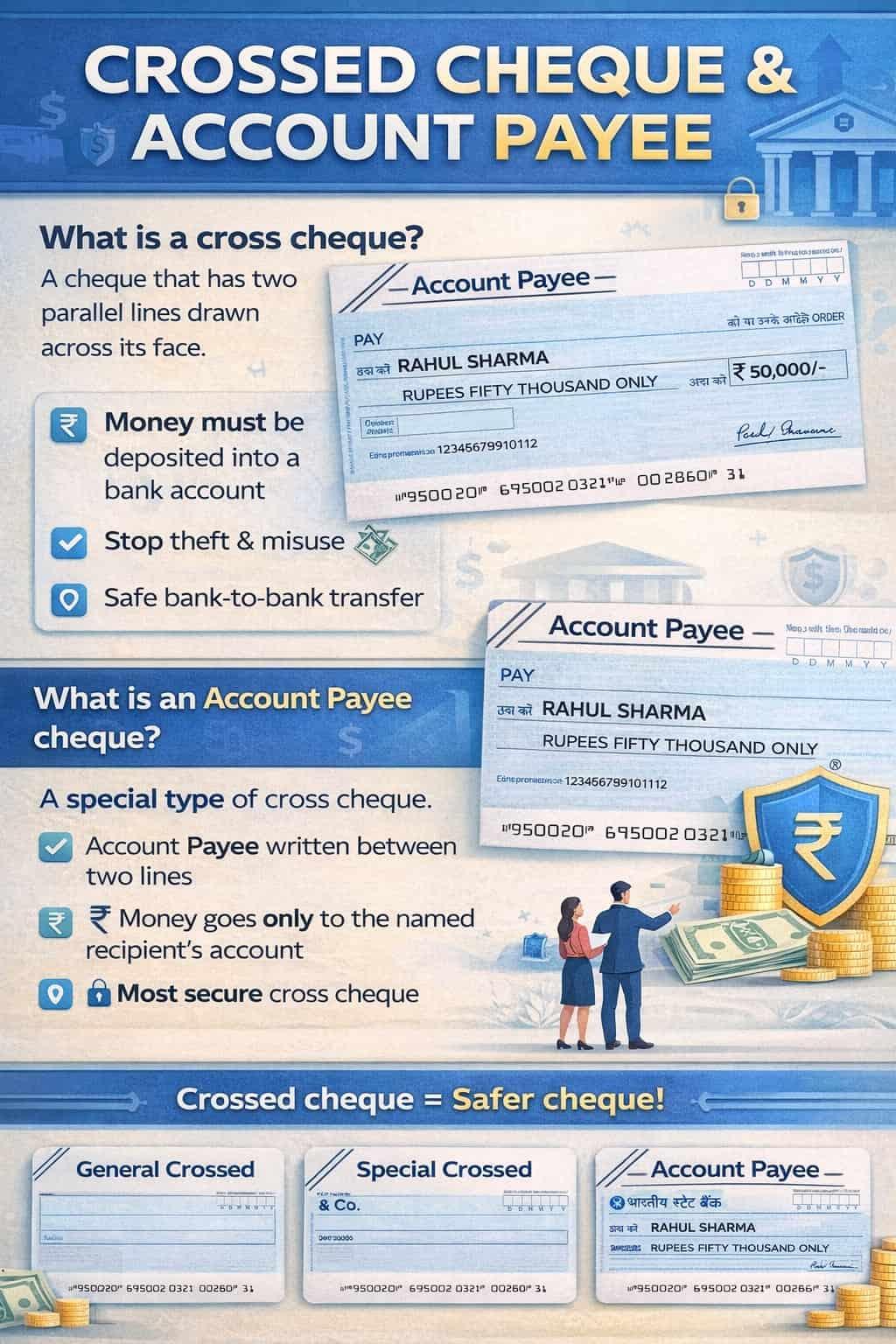

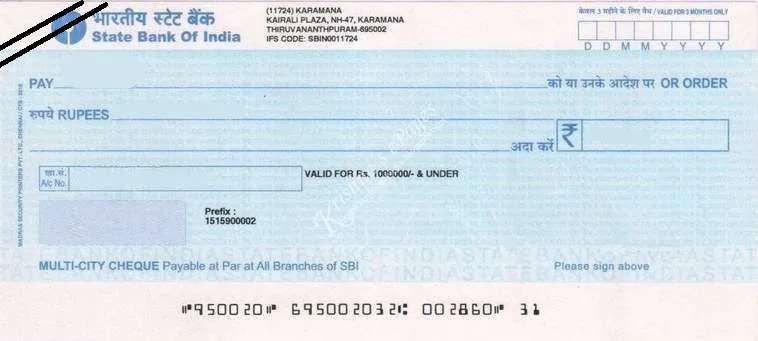

A cross cheque is a cheque with two parallel lines drawn on the top-left corner. These lines instruct the bank that the cheque amount must be credited only into a bank account and cannot be paid as cash over the counter.

If you are new to cheque banking, first understand how a cheque works in India .

⚠️ Legal Point: Cross cheque rules are recognised under the Negotiable Instruments Act, 1881 and processed through RBI cheque clearing systems.

📖 Read below: Types of crossed cheques, Account Payee cheque meaning, and how to correctly cross a cheque in India.

Types of crossing a cheque in India

Let’s understand the common types of crossed cheques used in the banking system –

1. General Crossing

- What it does: It restricts Cash Payments and counters instant cash immediately.

- How it appears: It is too simple to do, just put two parallel lines, nothing else is required than.

- Bank Effect:

- A Cheque can be deposited in any bank account in the payee’s name.

- The cash counter or branch will suggest using drop boxes for faster processing.

- Ownership verification is minimal

This is the most common crossing used by individuals.

2. Special Crossing

- What it restricts – It will block the other banks for deposits

- The pattern: It also has two parallel lines, but in between, there is one specific bank’s name written. such as HDFC or Bank of Baroda.

- What Bank got the signal:

- This gives a direct call, the Cheque must pass only through the named bank

- Any other bank must reject it

- Adds an accountability layer by fixing responsibility

This is more Special crossing that is frequently used by institutions and corporations. Most of the time, for salaries or making other payments.

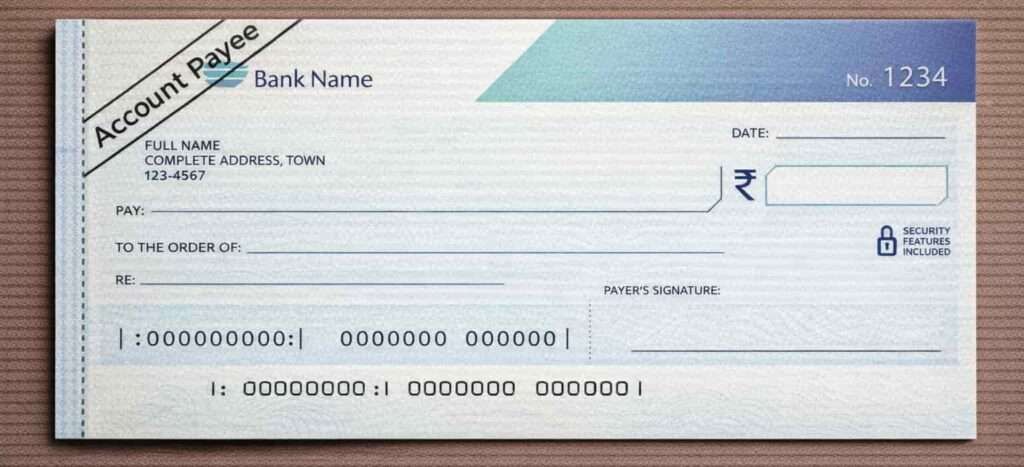

3. Account Payee Crossing

- Meaning: It restricts the beneficiary, or it gives a direct signal, and this is most common in india.

- Look Like: Words like “Account Payee” or “A/C Payee Only” written between crossing lines. only that, not the payee name in between.

- It allows:

- Money must be credited only to the named payee’s account

- Third-party credit is not permitted

- Highest level of misuse prevention

Although not separately defined in statute, banks treat this as a mandatory instruction. This is legal in indian law regulations.

4. Not Negotiable Crossing

- What is it all about: It blocks the title transfer. Not Negotiable Crossing means a cheque can be transferred, but the receiver does not get better legal rights than the giver.

- How it appears: The words “Not Negotiable” are added to a crossed cheque.

- Bank effect:

- A cheque can be transferred

- But the transferee cannot obtain a better legal title than the transferor

- Protects the true owner if the cheque is stolen or misused

💡 Quick Example – Rahul gives a “Not Negotiable” cheque to Amit. If Rohit (Amit’s friend) steals and deposits it, the money can still be recovered and returned to Amit. This crossing removes normal legal protection for third-party holders.

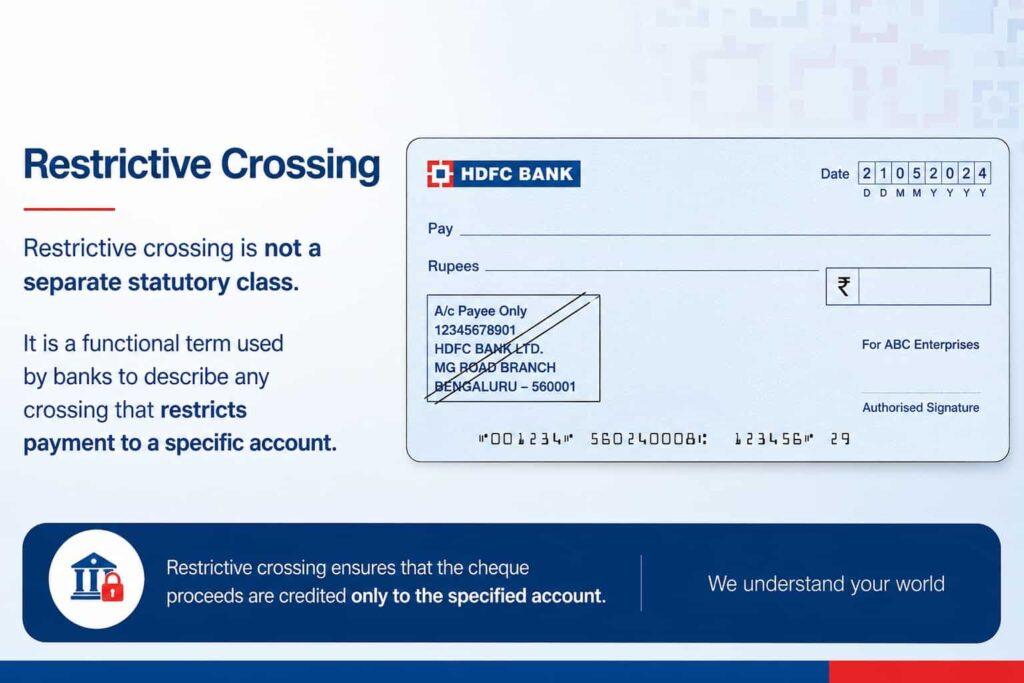

5. Restrictive Crossing

Restrictive crossing is not a separate statutory class. It is a functional term used by banks to describe any crossing that restricts payment to a specific account.

In practice:

- Account Payee crossing is the most common restrictive crossing

- Banks follow restrictive instructions strictly

How to Cross a Cheque in India

Crossing a cheque is simple and does not need bank approval. You can do it yourself while writing the cheque.

Step 1: Draw Two Parallel Lines

- Draw two parallel lines on the top-left corner of the cheque using the same blue or black pen. This is the standard method followed in India.

Step 2: Write Crossing Instruction

- Between the two lines, you can write:

- “Account Payee” for better security

- Bank name if required

- This tells the bank how the cheque should be processed.

Step 3: Fill Normal Cheque Details

- Now complete the cheque normally:

- Date

- Payee name

- Amount in numbers and words

- Signature or thumb impression

📌 Real Branch Level Tip – Some PSU bank users also sign on the back side of the cheque for extra safety. No extra stamp or special form is required.

Who can cross a cheque

A cheque can be crossed by:

- Drawer (Person issuing the cheque – the account owner)

- Holder (Person legally in possession of cheque)

- Banker (in limited circumstances while collecting)

This flexibility exists to allow safety enhancement even after issuance.

How to Deposit a Crossed Cheque

A crossed cheque cannot be encashed directly at the bank counter. It must be deposited into a bank account.

- Verify the Name: The name on the cheque must match the name on the bank account exactly.

- Complete a Deposit Slip: Provide the account number and cheque details on the bank’s deposit form.

- Endorse the Back: It is standard practice to write the account number and contact information on the back of the cheque.

- Submit for Processing: Place the cheque in a secure drop box or hand it to a bank teller.

- Wait for Clearing: Funds typically become available within 1–2 business days after the cheque clears.

How Banks Process Crossed Cheques

Today, banks process cheques through RBI’s CTS (Cheque Truncation System).

| # | Process | What Happens |

|---|---|---|

| Step 1 | Cheque Scan | Physical cheque image is scanned |

| Step 2 | Verification | Bank checks signature, balance, and cheque status |

| Step 3 | Clearing | Image moves through RBI clearing system |

| Step 4 | Settlement | Amount is credited to collecting bank |

Important Points

- Credit usually comes within 1–2 working days

- Cheques deposited after cut-off time are processed next working day

- Signature mismatch, overwrite, or low balance can cause cheque return instead of delay

Why People and Firms Issue Crossed Cheques

The main reason for using a crossed cheque is better payment security and proper transaction proof.

- Protection Against Loss or Theft: If a crossed cheque is lost or stolen, nobody can take cash directly from the bank counter.

- Money Goes to the Right Person: An “Account Payee” cheque sends money only to the named person’s bank account.

- Creates Payment Record: Banks keep details like who paid, who received, amount, and payment date.

- Used for Safer Business Payments: Many companies avoid bearer cheques because crossed cheques are safer and easier to track.

Real-Life Example

A contractor gives a crossed cheque of ₹18,500 to a worker.

- The worker cannot take cash directly from the counter

- He deposits the cheque into his bank account

- The bank processes the cheque through clearing

- Within 1–2 working days, the amount gets credited

- After that, the worker can withdraw cash or use UPI/ATM normally

In simple words, crossed cheques move money through bank accounts, not directly by hand.

⛔ One Drawback – Crossed cheques do not give instant cash. The cheque first goes through bank clearing, which normally takes 1–3 working days.

Crossed vs. Open Cheques: Key Differences

Crossing removes human decision-making at the teller counter, forcing secure, system-based processing.

| Basis | Crossed Cheque | Open Cheque |

|---|---|---|

| Payment Mode | Account deposit only. | Cash payout or deposit. |

| Counter Control | Strict routing; no cash allowed. | Teller dispenses cash directly. |

| Risk If Lost | Minimal; fully traceable. | Very high; anyone can cash it. |

| Processing | Clearing system (1–3 days). | Immediate cash payout. |

| Audit Trail | Permanent digital paper trail. | None if cleared via cash. |

| Negotiability | Restricted to named payee. | Transferable to third parties. |

Frequently Asked Questions

How can I withdraw a crossed cheque easily in India?

You can’t withdraw a crossed cheque directly in cash. The easiest way is to deposit it into your bank account, wait for credit, and then withdraw cash using ATM, branch, or UPI transfer.

How do I give a crossed cheque to someone correctly?

Just draw two clear parallel lines on the cheque, preferably at the top-left corner, write “Account Payee” for safety, then fill date, name, amount, sign it, and hand it over.

I received a crossed cheque but don’t have a bank account, what should I do?

You’ll need a bank account to receive the money. Crossed cheques are strictly account-credit only. Many people open a basic savings account just to deposit such cheques.

Can the bank manager allow cash on a crossed cheque if I request?

No, even a branch manager cannot override cheque crossing rules. Once crossed, cash payment is legally blocked. Banks don’t have discretion here, only compliance responsibility.

What happens if someone writes Account Payee but forgets to draw crossing lines?

Banks usually ignore “Account Payee” if crossing lines are missing. For full protection, both crossing lines and Account Payee wording should be present on the cheque.

Can I deposit a crossed cheque at any branch of my bank or only home branch?

You can deposit it at any branch of your bank, not necessarily your home branch. CTS has removed branch dependency, but you must still use your own bank.

Why do banks still issue cheques marked “or bearer” if crossing blocks cash?

Banks print standard cheque formats. The real control comes from crossing. Once crossed, “bearer” becomes irrelevant, and the cheque behaves strictly as account-credit only.

How to Deposit a crossing cheque via a branch?

If you have an HDFC Bank account and receive a crossed SBI cheque, visit any HDFC branch, fill out a cheque deposit slip with your account and cheque details, endorse the back if required, and drop it in the cheque box or submit it at the counter for account credit.

Hope you liked the content. Explore smart options below 👇

🔥 Recommended