The MICR (Magnetic Ink Character Recognition) code is a unique 9-digit number printed at the bottom of every cheque leaf. It helps banks process and clear cheques automatically using machine-readable magnetic ink technology.

If you are new to cheque banking, first understand how a cheque works in India .

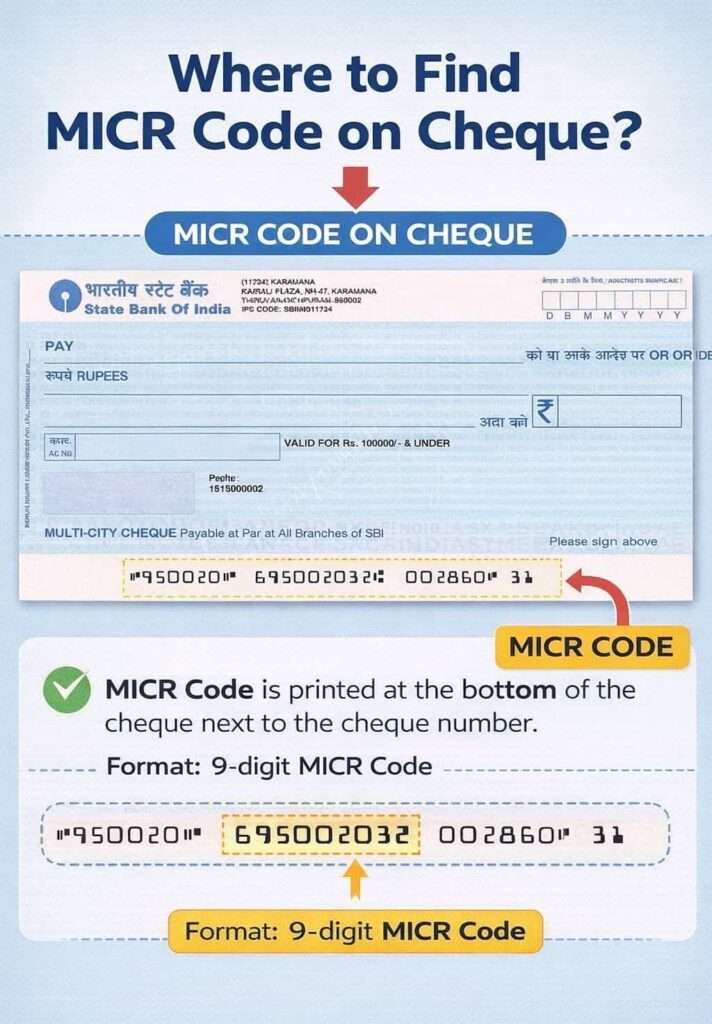

📌 How to Find MICR Code on a Cheque

💡 Quick Tip: On older cheque books, the last cheque leaf often has the cleanest MICR print because earlier pages may become faded or smudged over time.

⚠️ Important: If the MICR code is damaged, unclear, or missing, banks may reject or delay cheque processing during clearing.

📌 Banking Insight: Many people focus only on the cheque amount and signature, but bank staff often first verify the bottom MICR line because it controls automated cheque sorting and branch identification.

📖 Read below: Structure of a 9-Digit MICR Code, MICR vs IFSC difference, and common cheque mistakes banks see daily.

Structure of a 9-Digit MICR Code Explained

The MICR code is divided into three equal parts:

- City Code (Digits 1–3): Matches the first three digits of the location’s PIN code (e.g.,

110for New Delhi). - Bank Code (Digits 4–6): A unique identifier assigned to the banking institution by the central bank (e.g.,

002for State Bank of India). - Branch Code (Digits 7–9): Identifies the specific physical branch where the account is hosted.

These numbers help banks and cheque machines identify the correct bank and branch automatically. The system does not check who you are or how much money is written on the cheque.

It only checks one thing clearly: “Which branch should this cheque reach — without a human touching it?”

How MICR Works: The Technology Behind the Ink

MICR stands for Magnetic Ink Character Recognition. The special thing is not the MICR number itself, but the magnetic ink used to print it. This ink contains iron particles, which help cheque processing machines read the code properly.

Even if the cheque has stamps, signatures, or small pen marks, the MICR line usually still works if it is not damaged badly.

This is why MICR is considered reliable in banking systems.

1. What MICR Helps With

- Machines can read cheques automatically

- Small pen marks normally do not affect scanning

- Old or slightly damaged cheques can still be processed

- Cheque clearing becomes faster and more accurate

Most people think machines read MICR numbers like humans read digits. Actually, machines read:

- Magnetic signals

- Wave patterns

- Character spacing

That is why MICR became an important part of cheque clearing in India even before digital banking became common.

2. How Banks Actually Process a Cheque

At bank level, MICR scanning usually happens first.

- If the MICR line fails, the cheque may stop processing

- If MICR is successful, then the bank checks:

- CTS cheque image

- Signature verification

- Other security checks

So MICR is not just a printed code. It works like the first entry gate of cheque processing.

Key Features to Observe on Major Bank Cheques (SBI, ICICI, HDFC)

In 2025, the Reserve Bank of India (RBI) continued to classify these banks (SBI, ICICI, and HDFC Bank) as Domestic Systemically Important Banks (D-SIBs).

In simple words, these are banks considered critical to India’s banking system because they handle a huge share of the country’s daily banking and cheque transaction value.

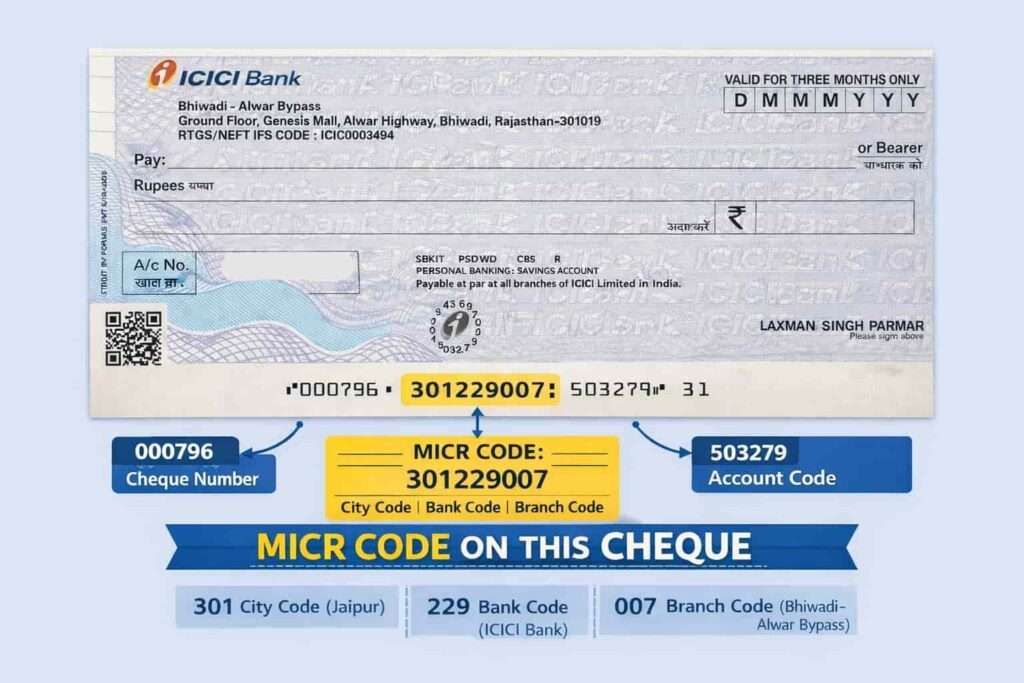

1. ICICI Bank Cheques

ICICI prints MICR codes with clear spacing, making them easier to identify even for first-time users. This reduces rejection during CTS scanning.

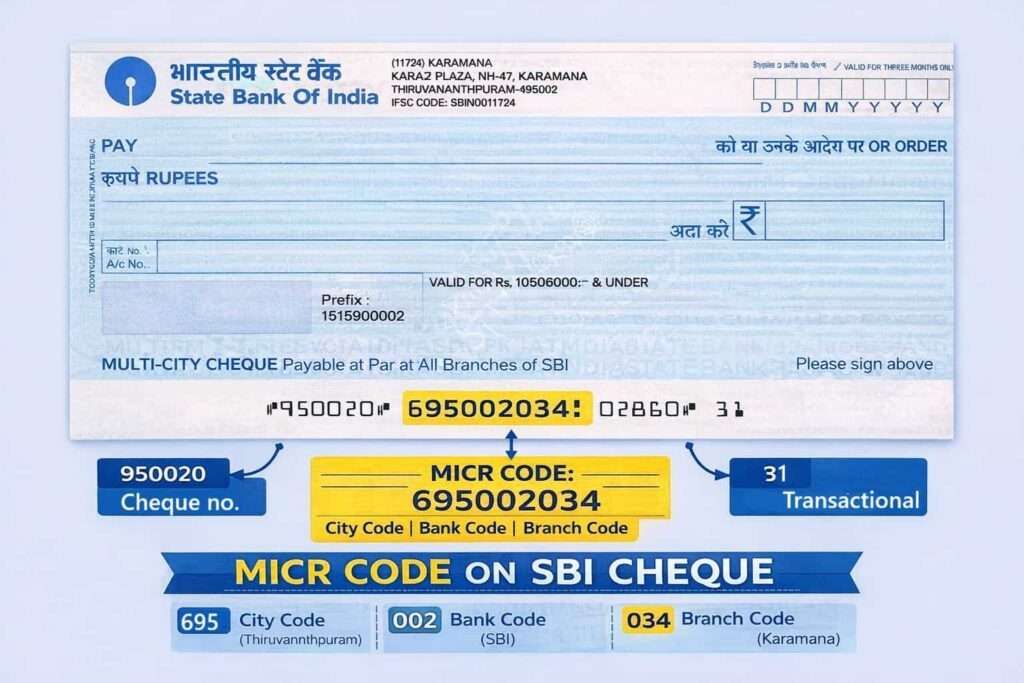

2. SBI Cheques

Given SBI’s scale, MICR accuracy is really important. Even a one-digit mismatch can route a cheque to the wrong clearing zone — which is why SBI MICR formatting is highly standardised.

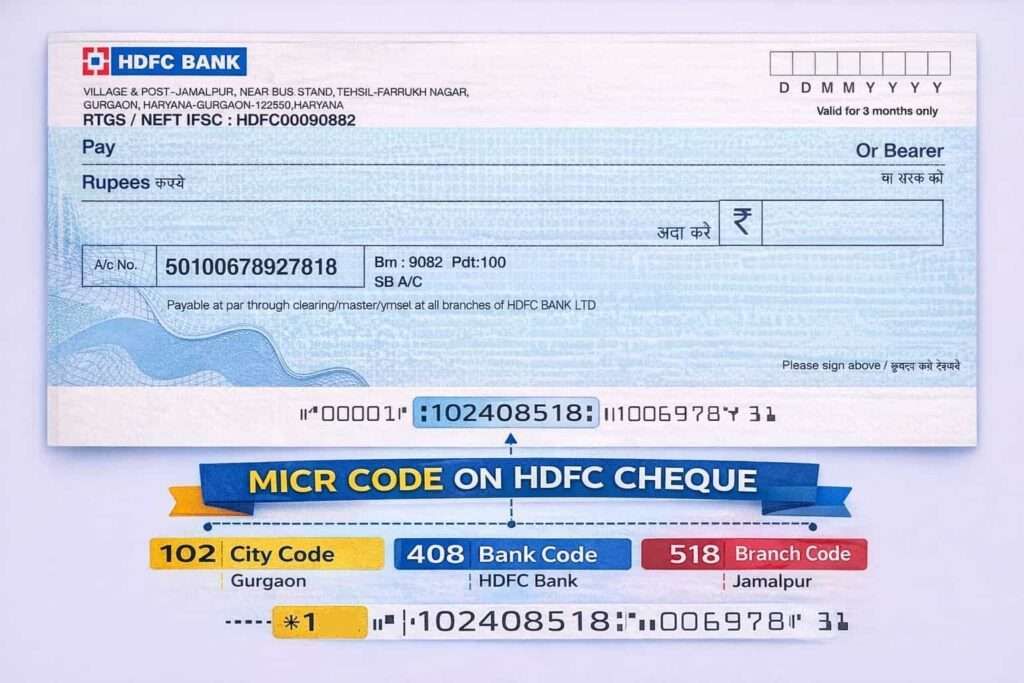

3. HDFC Bank Cheques

HDFC integrates MICR tightly with CTS image quality checks. Cheques with damaged MICR lines are flagged faster than in traditional clearing.

These differences are not visible, but they matter operationally. Also, the formatting is simple and the same, so, thing special they do at large, but they do more practical and easier for all.

MICR Code vs. IFSC: Clearing vs. Transfers

MICR and IFSC codes sometimes confuse users, but their purposes are fundamentally different, and they look different as well.

- MICR is used for cheque clearing, and it is only 9 digits

- IFSC is used for electronic fund transfers (NEFT, RTGS, IMPS) and it is 11-digits.

MICR is read by machines during physical or image-based clearing. MICR love to live quietly in the background. But IFSC is entered manually or digitally during online transfers. One does not replace the other. IFSC interacts directly with users.

Real-Life MICR Mistakes Banks See Every Day

These are some common cheque mistakes banks still see regularly during cheque processing:

- Writing IFSC code instead of MICR code

- Confusing cheque number with MICR number

- Submitting torn cheques with damaged MICR lines

- Thinking MICR is no longer important because UPI exists

- Using old branch MICR details after branch transfer or relocation

Remember, the cheque number is usually 6 digits, while the MICR code is a 9-digit branch identification number.

What Happens If the MICR Code Is Wrong or Damaged?

If the MICR line is unclear or damaged, the cheque may fail during machine scanning itself.

In real banking situations:

- The cheque may get rejected during CTS scanning

- Banks usually treat it as a technical return

- Payment processing gets delayed

- The cheque may need to be issued again

This is different from cheque bounce due to low balance.

Important Practical Point

MICR issues are considered routing or scanning problems, not fraud or payment refusal.

- No cheque bounce legal case starts immediately

- But repeated cheque issues can create trust problems

- Many businesses reject cheques if the MICR line looks damaged or unclear

Important Tip – Never fold, scratch, staple, or stamp heavily over the bottom printed line of a cheque, because that is where the MICR code is printed.

The Evolution of MICR: History & The Cheque Truncation System (CTS)

1. History and Introduction of MICR

MICR didn’t start in India. It was born in 1950s America. First developed in the 1950s, when banks began looking for ways to automate cheque handling. According to Wikipedia’s cheque history, the system was designed to handle large volumes of cheques reliably, even under imperfect physical conditions of the cheque. It came up from the feedback of the account holders, the cheque is almost like paper, so it cut, bent, wet, and more.

The success of MICR became a global standard for cheque processing

India adopted MICR much later, between 1987 and 1989. but at the perfect time. It is driven by the Reserve Bank of India. MICR-based cheque clearing was introduced in major metropolitan cities such as Mumbai, Delhi, Chennai, and Kolkata in phase 1.

Before MICR, cheque clearing in India was fully based on:

- Manual sorting

- Human verification for long weeks

- Physical movement of cheques between branches

This often resulted in delays ranging from several days to weeks. As noted by the Indian Banks’ Association (IBA), within a few years:

- clearing times dropped sharply

- inter-bank trust improved

- disputes became traceable instead of subjective

What’s important is what didn’t change: India never abandoned cheques.

2. Evolution of MICR with Cheque Truncation System (CTS)

When CTS-2010 launched, many experts and local people assumed MICR would fade out or drop sharply.

Under CTS:

- Cheque images are scanned

- MICR data is captured digitally

- Clearing occurs electronically

MICR did not become obsolete. But it successfully integrates into CTS workflows. It allows routing accuracy to remain intact even in a digital environment.

At the start of 2026, Cheque clearing with MICR, NCPI, and CTS – their bond makes cheque clearing almost the same day or within a few hours. RBI is working to launch a 3-Hour Confirmation Window for any cheque cleared in india.

Frequently Asked Questions

Why do banks still reject cheques even when the MICR code is correct?

Because MICR is only one checkpoint, not the final authority. Banks also verify image clarity (CTS), signature match, overwriting near the MICR band, and even paper quality. A perfect MICR code cannot save a cheque that fails visual or compliance checks. This surprises most people, but MICR helps routing, not approval.

What is the difference between a MICR and a non-MICR cheque?

A MICR cheque uses magnetic ink for automated clearing, while a non-MICR cheque depends on manual verification, making processing slower, riskier, and often unacceptable in modern clearing systems.

Can I cash a cheque without MICR ink?

In rare cases, banks may allow manual cashing at the home branch, but most clearing systems reject non-MICR cheques due to higher error risk and operational limitations.

Can MICR be read by humans?

Yes, humans can visually read MICR numbers, but the system is designed for machines that read magnetic signals, which banks trust more than manual interpretation.

What are the Advantages and disadvantages of MICR in cheques?

MICR enables fast, accurate cheque clearing with low fraud risk, but at same time, it requires special ink, strict formatting, and becomes unusable if the MICR line is damaged.

What are the two types of MICR?

MICR exists as physical magnetic printing on cheques and as digital MICR data captured during CTS processing, both representing the same routing information.

What happens if I print a cheque without MICR ink?

Banks usually reject such cheques because normal printing lacks magnetic properties, making them unreadable by clearing machines and invalid for standard cheque processing.

Do banks still use MICR?

Yes, banks still rely on MICR daily for cheque routing and clearing, even under CTS, especially for legal, government, and institutional cheque transactions.

Will MICR disappear as cheques decline in usage?

Unlikely in the near future. MICR is deeply embedded in legal payments, government settlements, court-mandated instruments, and institutional finance. Even if retail cheque usage falls, MICR will survive as long as cheques exist — which in India, is longer than people expect.

Why is MICR printed only at the bottom and nowhere else?

Because scanners are built for one fixed reading zone. if banks try to move MICR elsewhere would increase misreads and false rejections. This consistency is intentional and make the all process identical and fast.

Is MICR more trusted than IFSC inside banks?

For cheques — yes. IFSC relies on user input. MICR is machine-read directly from the instrument. That makes MICR less prone to customer error. Internally, banks trust system-read data more than typed data, even today.

Hope you liked the content. Explore smart options below 👇

🔥 Recommended