A bearer cheque allows anyone holding it to withdraw cash directly at the bank without strict identity verification.

- No fixed RBI limit: but banks apply checks above ₹50,000

- Risk factor: if lost, anyone can encash it

In simple terms, a bearer cheque lets anyone holding it withdraw cash, which makes it fast but risky if lost or misused. Banks apply risk controls like ID checks for higher amounts to prevent misuse.

Real-life Example

Akhil writes a cheque of ₹20,000 and leaves the payee line as “Cash or Bearer.” He hands it to Naman. Naman walks into Akhil’s bank branch, presents the cheque, the signature matches, the funds are available, and cash is paid on the spot.

If Naman gives the same cheque to Ravi, Ravi can legally encash it too. Possession equals entitlement. Unlike order cheques, bearer cheques don’t require the payee’s signature on the back for transfer.

Key Features of a Bearer Cheque

- Highly Transferable – It can be transferred simply by handing it over—no paperwork needed, and no ID proof required; however, basic KYC happen if the amount is higher than 50k.

- No Mandatory Endorsement– Usually, the payee’s signature on the back is not required if it bearer (sometimes, most PSU banks or RRBs may still ask for a signature for records and risk factor).

- Immediate Cash Payment – Bearer cheques can be encashed over the bank counter. It is commonly used as a self-cheque to an instant cash withdrawal at a branch, and it is easy to give.

Important Rules Most People Miss

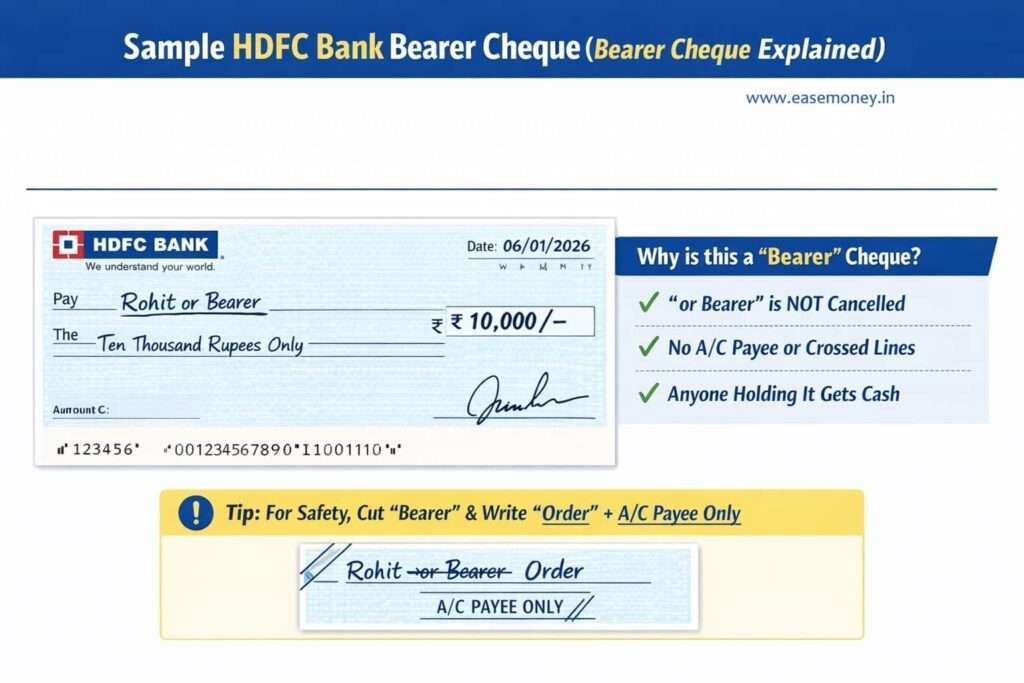

- Writing a name does not stop it from being a bearer cheque if “Bearer” is still allowed. If you are writing a cheque and want to limit it to only 1 bearer, simply strike out the or bearer printed section.

- Leaving the payee line blank is legally acceptable for bearer cheques.

- Banks depend far more on signature integrity than on who you are.

This is why bearer cheques feel fast and why they make compliance teams uncomfortable.

Bearer Cheque Limits and RBI Rules in India

1. No hard legal ceiling

The Reserve Bank of India (RBI) has never prescribed a fixed maximum legal amount for bearer cheques. A cheque of ₹5,000 and one of ₹5,00,000 are both legally valid instruments, and banks have to accept them and cash them for any bearer. But the risk control system starts here.

2. What the RBI actually does

Unlike just blocking the bearer cheques, the RBI set rules depending on the amounts and bearer identity –

- KYC-based verification for higher-value cash withdrawals at the home branch or any nearby branch. means, now, there is a risk control safety layer if the amount is higher.

- Monitoring and reporting of large cash movements under income-tax and AML norms

- Bank-level discretion to deny cash and force account credit when risk is high

This is an important distinction: bearer cheques are not illegal; uncontrolled cash movement is the concern.

2. The ₹50,000 and ₹2 lakh thresholds (real practice)

In all banks of india, RRB, commercial, and your PSU Banks. This works the same rule.

- Below ₹50,000: Cash payment is usually smooth; your branch may not ask for ID. (It is still subjective.)

- ₹50,000 and higher: Your Banks may ask for your govt-approved ID, PAN, or hold the right to refuse cash payment.

- ₹5 lakh and any big amount, even crores: The Positive Pay System (PPS) becomes critical. As per the RBI CTS, it is fully mandatory if the amount is near or higher than 5 lakh.

Positive Pay System (PPS) for High-Value Cheques

PPS requires the cheque issuer to pre-confirm details (cheque number, date, amount, payee). If PPS is mandatory and not submitted, the cheque can be rejected. even if it’s genuine and well-funded. The cheque issuer can confirm via the mobile banking app or net banking that, in the event of a non-submission or mismatch, the bank is likely to return or reject the cheque, even if there are sufficient funds in the account.

A ₹20,000 bearer cheque does not trigger PPS. A ₹5,00,000 cheque almost certainly will.

How to Write a Bearer Cheque Correctly

Writing a bearer cheque is simple, but mistakes can quietly kill its encashability.

1. Correct method

- Date: Use the current date (cheque validity is 3 months).

- Payee line: Write “Cash”, “Bearer”, or “Name or Bearer”. and not strike if already printed. When you order a chequebook, the bank gives bearer cheques by default in india.

- Amount in words: Write clearly, end with “Only.”

- Amount in figures: Match it exactly. You can put “/-” at the end, such as Rs 20,000/-.

- Signature: Must match bank records—this is non-negotiable. Confirm with your branch, most PSUs and RRBs ask for the backside cheque signature for double check.

2. What to do

- Use clear handwriting

- Keep amounts modest

- Prefer the home branch for faster cash; however, now, it works at all branches of the issuer bank.

3. What not to do

- Do not cross the cheque if you want cash

- Do not write “Account Payee”

- Do not overwrite amounts or dates

One overwrite can convert “fast cash” into a rejected instrument

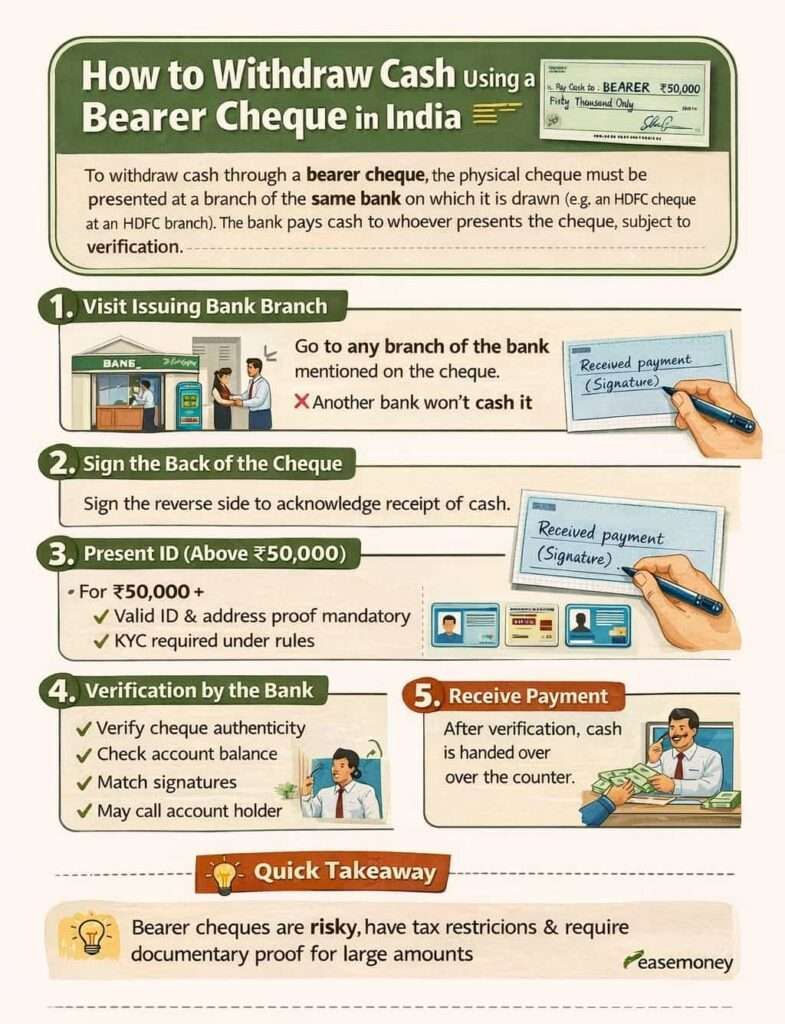

How to Encash a Bearer Cheque (Step-by-Step)

- Where to go: Prefer the drawer’s home branch (branch printed on the cheque). Simply, go to the bank teller (cashier). The bearer usually signs the back of the cheque to confirm they received the funds.

- What to carry: The original cheque; ID if the amount is large, such as Rs. 50,000 or above.

What the bank checks:

- Signature match

- Cheque validity

- Balance sufficiency

- The system will scan the MICR, Cheque number, and printed information.

Outcome:

- Small amounts → instant cash

- Large amounts → ID check, delay, or deposit-only decision, PPS required if the amount is 5 lakh or higher.

What not to do

- Don’t assume any branch will pay cash instantly without question.

- Don’t argue “it’s legally allowed”—branches have discretion

- Bearer cheques live at the intersection of law and branch policy.

Bearer Cheque vs Order Cheque (Key Differences)

The difference is not academic; it’s about who bears the risk. The key real-world change is the level of security and transferability

1. Bearer cheque

- Paid to whoever presents it at the branch counter

- Cash-friendly and instant if the amount is lower.

- High risk if lost

- Minimal traceability

2. Order cheque

An order cheque is meant for one person only—the name written on it. The bank checks the identity before releasing money, and the cheque can’t be used by just anyone holding it. This extra step makes it far safer than a bearer cheque and reduces the risk of misuse.

- Paid only to the named person

- Usually deposited, not cashed, but if a crossed cheque

Strong audit trail and CTS clearing time - Far safer for the issuer

In practice, most businesses avoid bearer cheques for accounting clarity. Individuals still use them for urgency, for self-cheque, and for quick withdrawal.

Why Bearer Cheques Are Still Used in India

If they’re risky, why do they survive?

1. Speed beats everything

No clearing cycle. No waiting. In emergencies, time matters more than audit trails.

2. Cash-driven use cases

Small traders, transport payments, rural transactions—cash still rules many micro-economies.

3. Simplicity

No need to collect bank details. No failed transfers. No technical dependency.

4. Trust-based exchanges

Between family, friends, or known parties, risk feels manageable.

Bearer cheques thrive where trust substitutes technology.

Insight: In India, Bearer cheques behave less like banking instruments and more like legal cash or banknotes. A single signed slip can still unlock real money at a bank counter, and no need for OTP, no clearing cycle, and no digital trail. What makes this even more fascinating is that the Reserve Bank of India has never capped their legal value.

Frequently Asked Questions

Which is better, bearer cheque or order cheque?

An order cheque is better for safety because money goes only to the named person. A bearer cheque is faster for cash but risky, since anyone holding it can withdraw the money.

What is a specimen bearer cheque?

A specimen bearer cheque is a sample or cancelled cheque used for learning or KYC purposes. It shows how a bearer cheque looks but cannot be used for withdrawal or deposit.

How long is a bearer cheque valid?

A bearer cheque is valid for three months from the date written on it. After that period, banks will not honor it, even if the signature and balance are correct.

How to convert a bearer cheque into an order cheque?

To convert it, simply strike off the word “Bearer” on the cheque. Once crossed out, the cheque becomes an order cheque and can be paid only to the named person.

Can a bearer cheque be encashed without ID?

For small amounts, banks usually don’t ask for ID. However, if the amount is high or looks risky, the bank can still ask for identification before paying cash.

Is it safe to leave the payee name blank on a bearer cheque?

Legally it’s allowed, but practically it’s risky. If the cheque is lost, anyone can encash it. Writing a name adds slight control, though it remains a bearer cheque.

Why do banks discourage large bearer cheque payments?

Because bearer cheques have no ownership trail. Large cash payouts increase fraud and tax risks, so banks prefer deposits, ID checks, or safer payment methods for higher amounts.

What are bearer cheques also called?

Bearer cheques are called open cheques or uncrossed cheques, as they can be encashed directly by the holder at the bank counter.

Hope you liked the content. Explore smart options below 👇

🔥 Recommended