💳 Credit Card Late Payment Calculator

📊 Charges Estimate

📉 Credit Score Impact

⚠ Calculator Assumptions

Minimum Due: Usually 2–10% of statement balance.

Interest: Estimated ~3.5% per month.

Grace Period: Banks usually allow ~3 days.

Credit Reporting: 30+ days delay may affect CIBIL score.

In Axis Bank, what are the Late Payment Charges on Credit Card?

When you use a credit card and receive your monthly bill, Axis Bank usually gives you two payment options to clear it =

- Pay the full statement amount

- Pay the Minimum Amount Due (MAD)

If you pay the full amount, no interest is charged, and your credit card continues to enjoy the interest-free period for around 40 to 55 days.

But if you don’t pay the full bill, Axis Bank still allows you to keep the card active by paying the Minimum Amount Due. This amount is usually around 5% of the total outstanding balance, although it may vary slightly depending on the card and billing cycle.

Now the important part.

If the Minimum Amount Due is also not paid before the due date, the bank treats it as a missed payment and applies penalties. Here, the late payment fee applies to you.

What Charges Can Apply

- Late payment fee based on the total outstanding balance slab

- 18% GST on the late payment fee

- Finance charges (interest) on the unpaid balance

The late fee itself depends on the Total Payment Due shown in the statement. The higher your outstanding balances, the higher the penalty slabs + GST + Interest you will get. So if you miss the payment deadline, the next statement can include late fees, tax, and interest together, which increases the total amount payable.

Axis Bank Credit Card Late Payment Fee Slabs (2025–2026)

Axis Bank follows a slab-based late payment fee system. The penalty depends on the Total Payment Due shown in the monthly credit card statement. Simply put, the higher your outstanding balance, the higher the late payment fee if the Minimum Amount Due is not paid before the due date.

Also, remember, all late payment charges attract 18% GST, which increases the final penalty amount.

| Total Payment Due (Balance) | Late Payment Fee | Total Fee (Including 18% GST) |

|---|---|---|

| Up to ₹500 | Nil | ₹0 |

| ₹501 – ₹5,000 | ₹500 | ₹590 |

| ₹5,001 – ₹10,000 | ₹750 | ₹885 |

| Above ₹10,000 | ₹1,200 | ₹1,416 |

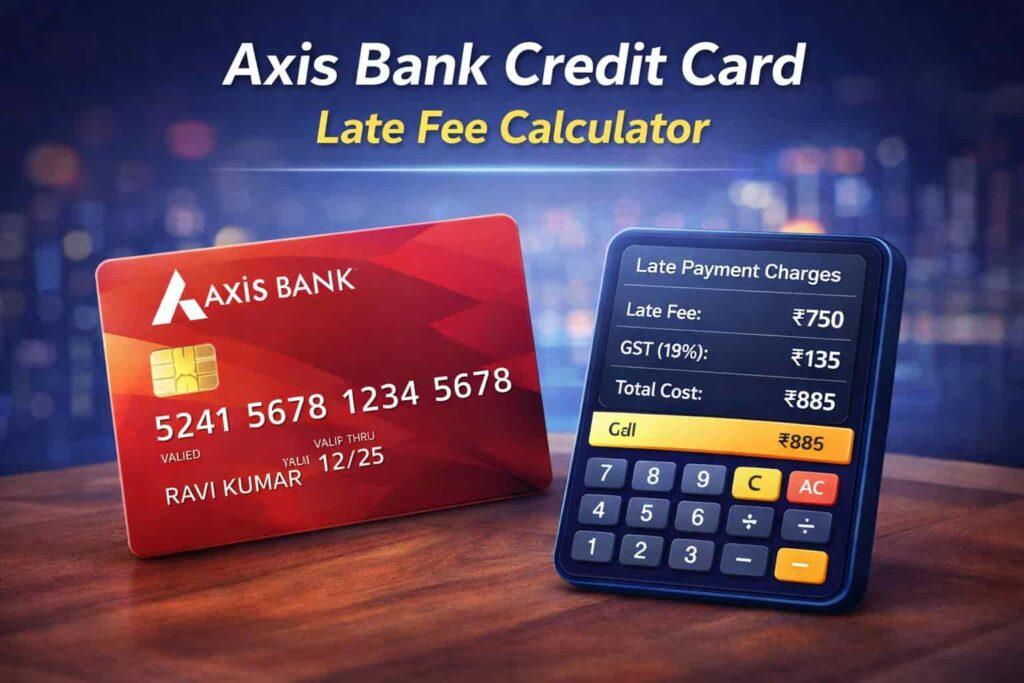

Simple Example

Suppose your credit card bill is ₹8,000 and you miss the payment deadline.

- Late payment fee: ₹750

- GST (18%): ₹135

- Total penalty: ₹885

This amount will be added to the next credit card statement, along with any interest charges if the balance remains unpaid.

Special Case

As per the Axis Bank Terms PDF, some premium cards, like the Axis Bank Burgundy Private Credit Card, may have no late payment fee. However, interest on the unpaid balance can still apply if the full bill is not cleared on time.

What are the Axis Credit Card Interest Rates?

Axis Bank credit cards charge interest when the full statement bill is not paid by the due date. This interest is called finance charges. The rate is not the same for every card. It depends on the card tier or variant you are using.

In general, Axis credit card interest ranges between 1.5% and 3.75% per month, which roughly converts to about 19.56% to 55.55% per year. As per IndiaTimes News, Around December 2024, Axis revised the standard interest for many retail cards from 3.6% to about 3.75% monthly.

Here are the Credit Card-wise Interest Rates =

| Credit Card Tier / Variant | Monthly Interest | Annual Rate |

|---|---|---|

| Primus Credit Card | 1.00% | 12.68% |

| Burgundy Private Credit Card | 1.50% | 19.56% |

| Pride Platinum OR Pride Signature | 2.95% | 41.75% |

| Magnus/Reserve/Olympus | 3.00% | 42.58% |

| Secured OR Easy Cards (Insta Easy, My Zone Easy) | 3.40% | 49.36% |

| Mainstream Cards (Flipkart, Ace, My Zone, Airtel) | 3.75% | 55.55% |

| Other Axis Credit Cards | 3.75% | 55.55% |

GST of 18% also applies to the interest amount. Axis usually calculates interest using the average daily balance method. In simple terms, interest keeps building day by day until the outstanding balance becomes zero.

Why Credit Card Interest Confuses Many Users

A lot of people think interest is charged only when they completely skip a payment. But that’s not always true. Even if a cardholder pays something, interest can still apply depending on how much of the bill was cleared.

Two common situations cause finance charges.

Situation 1: When You Pay Only the Minimum Amount

Paying your Minimum Amount Due helps avoid the late payment penalty, but it does not stop interest. Example:

| Detail | Amount |

|---|---|

| Statement bill | ₹10,000 |

| Minimum amount due | ₹500 |

| Remaining balance | ₹9,500 |

| Estimated monthly interest | ₹330 – ₹420 |

So even though the late fee is avoided, the bank still charges interest on the ₹9,500 balance until it is fully paid. During this time:

- The interest-free period disappears

- New purchases can start attracting interest immediately

Situation 2: When No Payment Is Made

If the cardholder does not pay anything after the due date, the cost becomes higher because several charges appear together. Example:

| Detail | Amount |

|---|---|

| Statement bill | ₹15,000 |

| Late payment fee | ₹1,200 |

| GST (18%) | ₹216 |

| Estimated interest | ₹525 |

| Approx extra charges | ₹1,941 |

So the next statement becomes significantly larger because late fee, GST, and interest all add up together.

Real Example: ₹20,000 Axis Credit Card Bill

Let’s look at a practical situation. Suppose you get a ₹20,000 credit card bill and do not pay it on time.

| Detail | Value |

|---|---|

| Credit card bill | ₹20,000 |

| Late payment fee | ₹1,200 |

| GST (18%) | ₹216 |

| Estimated interest | ₹700 |

| Total additional charges | ₹2,116 |

Because of the delay, the next statement may rise to around ₹22,116 if the balance is not cleared quickly. This is why credit card payments need attention. Missing a payment may look small at first, but interest plus penalties can slowly push the bill higher every month.

When Axis Bank Actually Applies the Late Payment Fee

Many credit card users think the late fee appears immediately after the due date, but in reality, the process usually follows a simple sequence. If the Minimum Due is not paid before the due date mentioned in the statement, the account becomes overdue, and the penalty is applied in the next billing cycle.

What Usually Happens After the Due Date

| Stage | What Happens |

|---|---|

| Payment due date passes | Card account becomes overdue |

| Next statement generated | Late payment fee is added |

| Balance carried forward | Interest begins on the unpaid amount |

If the MAD is paid before the due date, the late payment fee normally does not apply, even if the full bill is not cleared. However, the remaining balance still starts attracting interest until it is fully paid.

Simple Example

Suppose your Axis Bank credit card bill is ₹12,000, and the Minimum Amount Due is ₹600.

- If you pay ₹600 before the due date, no late payment fee is charged.

- But the remaining ₹11,400 will start attracting interest until it is cleared.

Axis Bank New Rule: Extra ₹100 Consecutive Default Charge

Axis Bank may also add a small additional penalty if payments are missed repeatedly. If the Minimum Amount Due is missed for two consecutive billing cycles, the bank can apply an extra ₹100 consecutive default charge.

This charge can continue every billing cycle until the overdue balance is cleared.

Why This Matters

Repeated missed payments can trigger other actions from the bank, such as:

- Temporary card usage restrictions

- Credit limit reduction

- Additional monitoring of the account

For example, if someone skips payments for two months in a row, the statement might include:

- Normal late payment fee

- GST on the penalty

- Finance charges on the balance

- Extra ₹100 consecutive default charge

So the total cost slowly increases if the delay continues.

What is the RBI 3-Day Grace Window, and how does it help you?

Many customers don’t realise that banks usually allow a small buffer window after the due date. As per the Reserve Bank of India credit card guidelines, there is typically a short grace period before banks report a payment delay to credit bureaus.

What This Means in Practice

- Payments made within about 3 days after the due date may avoid negative credit reporting.

- But interest calculations can still begin from the original due date.

Example

If your due date is May 10 and the payment reaches the bank on May 12, the account may still avoid a negative credit report. However, interest may still apply for those extra days.

This grace window mainly exists to protect customers from situations like:

- Payment gateway delays

- Bank processing time

- Public holidays or weekends

But it should not be treated as an extended due date, because charges can still start building even during those few days.

Understanding: Axis Bank Credit Card Late Fee Calculator (Online Tool)

Axis Bank does not currently offer a separate late fee calculator on its official website. So if someone wants to quickly check how much a missed payment may cost, they usually have to estimate it manually, using pen and paper, but

To make things easier, many users use the Axis credit card late fee calculator available on Easemoney. The idea is simple — instead of guessing charges, the tool gives a quick estimate based on your bill amount.

Once you enter your statement balance, the calculator shows a rough picture of how the next bill might increase if the payment is missed. The tool usually calculates three things – your GST, interest, fee and CIBIL impact.

How to Use the Late Fee Calculator

Using the calculator is simple. Most people can estimate the penalty in less than a minute.

Follow these steps:

- Enter your total credit card bill amount from your statement

- Choose what you paid the Minimum Amount Due, or missed it completely

- The calculator automatically applies the Axis Bank late fee slab

- It then adds GST and estimated interest charges

- Finally, it shows the estimated new outstanding balance

So instead of waiting for the next statement, you can quickly see how much the bill may increase.

Simple Do’s and Don’ts for Credit Card Payments

Do’s

- Try to clear the full credit card bill whenever possible, because that keeps the interest-free benefit active.

- When the full payment isn’t possible, pay the Minimum Amount Due before the due date so the late fee is avoided.

- Setting auto-debit through Axis mobile banking helps a lot, especially when you forget payment dates.

- Paying 2–3 days before the due date is a smart habit, since bank processing can sometimes take time.

Don’ts

- Relying on a minimum payment every month slowly increases the interest on the remaining balance.

- Using a credit card for cash withdrawal becomes expensive because interest begins immediately.

- Repeated missed payments can lower your credit score and may lead to card restrictions later.

FAQs

What happens if I am 3 days late on my credit card payment?

If payment is 3 days late, Axis may start charging interest, but credit bureau reporting usually doesn’t happen immediately. Example: ₹10,000 balance may start adding about ₹35–₹40 interest daily. You will get the RBI 3-day grace.

How much charges for Axis Bank credit card late payment?

Axis late payment fee depends on bill size. Example: if statement balance is ₹8,000, bank may charge ₹750 late fee plus ₹135 GST, making the penalty around ₹885 total.

Who pays the 3% credit card fee?

The 3% fee usually appears when merchants add surcharge for credit card payments, especially for utilities or small shops. For example, ₹5,000 payment may add about ₹150 extra.

How much does a credit card charge for late payments?

Most Axis credit cards charge between ₹500 and ₹1,200 as late fee. Along with GST and interest around 3.5% monthly, the real cost can cross ₹1,500 quickly.

What are Flipkart Axis Bank credit card late payment charges?

Flipkart Axis credit card follows the same slab rules. Example: ₹12,000 bill missed may trigger ₹1,200 late fee plus ₹216 GST and interest charges on remaining balance.

Can Axis Bank reverse a late payment fee?

Sometimes yes. If it’s the first delay and payment history is good, customers can request a reversal. Banks occasionally waive ₹500–₹900 penalty as a goodwill gesture.

Does RBI allow banks to charge late payment penalties?

Yes. RBI allows banks to apply late payment fees if Minimum Amount Due is missed. But banks must clearly disclose charges in the credit card terms and monthly statement.

Hope you liked the content. Explore smart options below 👇

🔥 Recommended