💳 Credit Card Late Payment Calculator

📊 Charges Estimate

📉 Credit Score Impact

⚠ Calculator Assumptions

Minimum Due: Usually 2–10% of statement balance.

Interest: Estimated ~3.5% per month.

Grace Period: Banks usually allow ~3 days.

Credit Reporting: 30+ days delay may affect CIBIL score.

Does HDFC provide a Credit Card Late Payment Fee Calculator?

No, HDFC Bank does not provide any official Late Payment Charges Calculator on its website or credit card portal. Instead of a calculator, the bank follows a fixed slab-based late fee structure depending on the total outstanding balance in the monthly statement.

Because of this system, most financial websites also don’t provide an exact HDFC calculator. They usually show static charge tables or manual formulas to estimate the late payment fee and interest amount.

If someone wants a quick estimate, tools like the Easemoney Late Payment Calculator can help calculate possible charges using the latest late-fee slabs and payment delay details.

Now, let’s check the latest charge slabs provided by HDFC below.

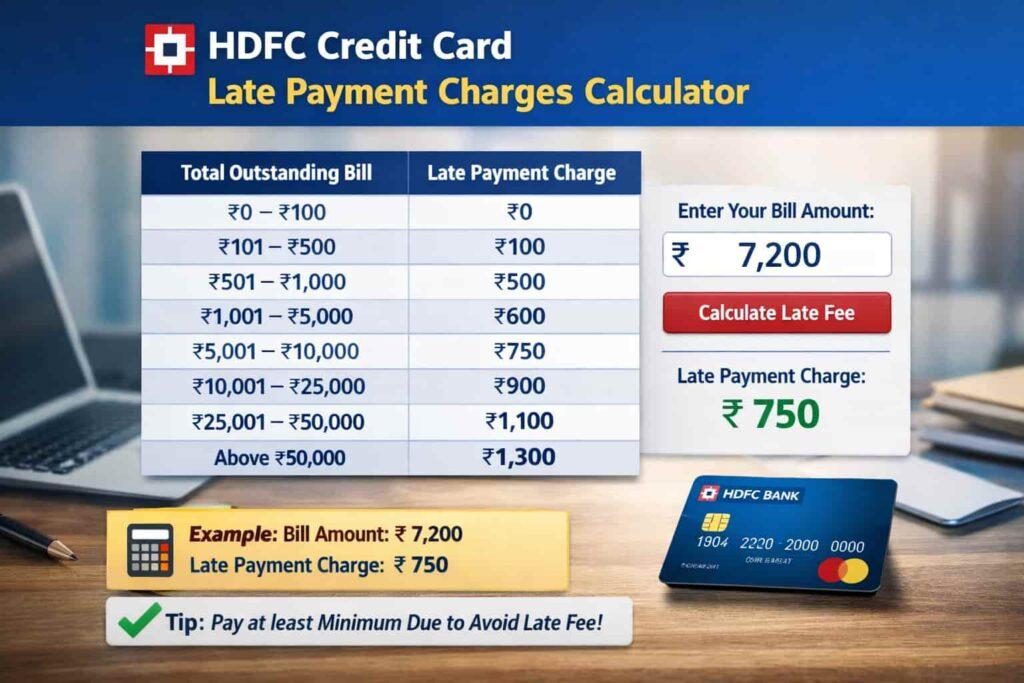

What is the Latest HDFC Card Late Payment Fee Structure?

HDFC Bank applies a slab-based late payment fee if the Minimum Amount Due (MAD) is not paid before the credit card due date. The charge mainly depend on the total outstanding balance shown in the monthly statement. If MAD paid on time, late fee usually not applied.

Fee Slabs (March and April 2026)

| Total Outstanding Balance | Late Payment Fee |

|---|---|

| Up to ₹100 | Nil |

| ₹101 – ₹500 | ₹100 |

| ₹501 – ₹1,000 | ₹500 |

| ₹1,001 – ₹5,000 | ₹600 |

| ₹5,001 – ₹10,000 | ₹750 |

| ₹10,001 – ₹25,000 | ₹900 |

| ₹25,001 – ₹50,000 | ₹1,100 |

| Above ₹50,000 | ₹1,300 |

Important Rules to Know

- Trigger condition = If even Minimum Amount Due (normally around 5% of the balance or ₹200) not paid, late fee apply according to slab.

- 3-day buffer window: Bank generally give around a 3-day grace period as per RBI after due date. If payment done quickly, penalty sometimes avoided.

- GST: All late fees and finance charges attract 18% GST.

- Credit score effect: If the delay becomes longer, the bank reports the payment behaviour to TransUnion CIBIL, which may reduce credit score.

Note: Unlike a late fee, which is flat, there is also interest that starts applying on your card due. learn below.

After the Flat Fee – Interest (Charges) on HDFC Credit Card Late Due

After the late payment fee is added, HDFC Bank also starts applying finance charges (interest) on the unpaid balance. But unlike the flat late fee, this interest calculated using a daily reducing balance method.

This means interest not charged only for the delay days. Instead, calculation usually start from the original transaction date until the full outstanding balance cleared.

Simple formula idea: Interest = Outstanding Amount × Monthly Interest Rate × (Days ÷ 30)

Another important thing — if payment missed or only Minimum Amount Due paid, the interest-free period normally stops. If new purchases happen after that, interest may start from the purchase date itself.

HDFC Monthly Interest Rates (2026)

- Premium cards (Infinia, Diners Black): around 1.99% per month (~23.88% yearly)

- Standard cards (Regalia, Millennia, MoneyBack): around 3.60%–3.75% per month (up to ~45% yearly)

| Card Variant | Monthly Interest Rate | Annual Rate (APR) |

|---|---|---|

| Infinia / Infinia Metal Edition | 1.99% | 23.88% |

| Diners Club Black / Black Metal | 1.99% | 23.88% |

| Tata Neu Infinity | 3.49% | 41.88% |

| Regalia / Regalia Gold | 3.60% – 3.75% | 43.2% – 45% |

| Millennia | 3.60% – 3.75% | 43.2% – 45% |

| MoneyBack / MoneyBack+ | 3.60% – 3.75% | 43.2% – 45% |

| Freedom | 3.75% | 45% |

| IndianOil HDFC | 3.49% – 3.75% | 41.88% – 45% |

| Paytm HDFC Mobile OR Tata Neu Plus | 3.75% | 45% |

Example Scenario

If the ₹10,000 balance from a purchase made 30 days earlier still unpaid:

- Late Fee: ~₹600

- Interest: ~₹355

- GST (18%): ~₹172

Total penalty: ~₹1,127

Real Example

Atma Ram Bhide from Mumbai used HDFC credit card for a ₹10,000 electronics purchase. Due date missed because payment reminder overlooked. Unlike paying on time, delay caused late fee plus interest, and final statement amount increased by around ₹1,100, including GST.

Credit Card Late Fee Calculator – Top HDFC Features

- Calendar-Based Date Selection = Billing date and payment date can be selected using a simple calendar picker. This makes it easier to track delay days and manage payment timing without confusion.

- Manual Minimum Due Entry = Minimum Amount Due can be entered manually if the exact MAD from the statement is known. This helps get a closer estimate of possible charges.

- Automatic Slab Detection = The calculator follows the latest HDFC late payment slab structure and automatically applies the correct late fee based on the outstanding balance.

- Interest Estimation = It calculates approximate finance charges based on the delay days and the typical monthly interest range used by HDFC cards.

- GST Included in Estimates = The tool also adds 18% GST to late fees and interest, so the final number looks closer to the real statement impact.

- Credit Score Impact Indicator = It shows a possible credit score risk level, helping understand whether the delay is minor or could affect the credit profile.

- “What If” Scenario Testing = You can test scenarios like not paying the Minimum Amount Due, paying late, or clearing only part of the bill to see how the total cost may change.

How to Reverse HDFC Credit Card Late Payment Fee

If a late fee appears on your HDFC Bank credit card statement, you can request a reversal only it applies first weeks But first, clear the Minimum Amount Due or full outstanding balance. Banks usually consider reversal only when payment behaviour has been mostly regular.

| Step | What You Need to Do |

|---|---|

| Pay Outstanding | Clear MAD or full bill immediately to show repayment intent |

| Call Support | Contact credit card helpline: 1800-202-6161 or 1860-267-6161 |

| Email Request | Send explanation to customerservices.cards@hdfc.bank.in |

| Branch Visit | If needed, discuss with branch manager directly |

Important points

- Fee reversal normally takes 2–4 working days after approval.

- If payment history is clean and delay happened first time, chances of reversal increase.

- Tip: Keep payment screenshots ready when contacting support for faster resolution.

Managing HDFC Late Fees When Using Multiple Credit Cards

Handling many cards becomes tricky if due dates are scattered. Small discipline helps avoid unnecessary late fees and interest.

What to Do

- Set Auto-Pay for Minimum Due = Enable auto-debit through HDFC Bank NetBanking or app so at least MAD gets paid automatically.

- Keep Due Dates in One Window = Request billing cycle change so most cards fall after salary credit week.

- Track All Cards in One Place = Apps like PayZapp or a simple reminder list help see all due dates together.

- Ask for Fee Waiver Once = If payment missed first time, customer support sometimes reverses the late fee.

What to Avoid

- Don’t Depend Only on Minimum Payment = Interest up to ~45% yearly keeps adding on the remaining balance.

- Don’t Pay Exactly on Due Date = Third-party payments may settle late; try paying 3–4 days earlier.

- Don’t Overspend Across Cards = Reward chasing often creates multiple bills arriving together.

What If Utilization Is High and Multiple Cards Have Late Fees? (Snowball Method)

If credit utilisation crosses 70–80% and several cards start charging late fees, things can spiral quickly. But the snowball method helps regain control step by step.

- Stop new penalties first = Pay at least the Minimum Amount Due on every card before the due date. If you miss it, another late fee may appear in the next statement.

- Pause card spending = If the balance is already high, avoid using the cards. With interest around 3.6%–3.75% per month (≈45% yearly), even small purchases grow fast.

- List balances from lowest to highest = Example: ₹3,200 → ₹8,500 → ₹21,000.

- Attack the smallest balance = Pay minimums everywhere, but push extra money to the smallest limit card. such as your have HDFC Card for limit 25k, clear it first, than start focusing other 50k or 80k cards.

- Roll the payment forward = Once a card becomes ₹0, shift that payment to the next card.

Tip: Clearing even one card can reduce the utilisation ratio and slowly improve your **TransUnion CIBIL score over the next few months.

FAQs

What is the penalty for late credit card payment in HDFC?

Late fee depends on statement balance. Example: ₹1,001–₹5,000 balance usually attracts around ₹600 fee. But GST 18% also added. If delay continues, interest around 3.6%–3.75% monthly starts.

Is a 2-day late credit card payment bad for HDFC users?

Usually bank gives around 3-day grace window after due date. If you pay within that time, late fee may not apply. But interest from transaction date can still continue.

What is the penalty for a 1-day late credit card payment?

One-day delay normally doesn’t trigger immediate late fee because of the grace buffer. But if payment not cleared quickly, charges may appear in next statement cycle.

What is the 2.5% charge sometimes seen on a credit card?

Around 2%–2.5% fee usually appears when converting purchases into EMI or doing wallet loading. Example: ₹10,000 transaction may add ₹200–₹250 processing charge plus GST.

How much interest applies on ₹10,000 HDFC credit card balance?

If ₹10,000 remains unpaid for about 30 days, interest roughly ₹350–₹375 may appear depending on card rate, plus 18% GST on that interest amount.

Can HDFC reverse late payment charges once?

Sometimes yes. If payment history good and delay happened first time, contacting **HDFC Bank support quickly may help get one-time late fee reversal after review.

Hope you liked the content. Explore smart options below 👇

🔥 Recommended