You should always pay the full “Total Amount Due” before the due date to avoid heavy interest charges and maintain a healthy credit score.

Paying only the Minimum Amount Due (MAD) may stop late fees temporarily, but banks still charge very high interest on the remaining balance — often around 40% to 50% annually.

🤔 Is paying only the minimum due a good idea?

💸 It keeps your card active, but interest starts compounding daily on unpaid balances and many new transactions.

🎯 If you are facing a cash shortage, converting the balance into EMI is usually safer than staying trapped in revolving credit interest.

📌 Understanding Your Credit Card Bill

- Total Amount Due: The complete bill amount for your current billing cycle

- Minimum Amount Due: Usually around 5% of the total bill required to keep the account active

- Current Outstanding: Your live balance including recent unbilled transactions

- The Debt-Reduction Choice: Paying more than the minimum due — even if you cannot clear the full bill — helps reduce interest costs faster and lowers your credit utilization ratio over time

💡 Nanne’s Core Insight: Try paying your credit card bill at least 3–5 days before the due date. Sometimes UPI, BBPS, or bank settlements get delayed, and even a short delay may trigger penalties or affect your repayment history.

⚠ Important: If the full bill is not cleared, banks can charge finance charges around 3.5%–4.2% per month plus GST, along with late payment fees that may go up to ₹1,300.

You can also read the official RBI credit card guidelines for billing practices, penalties, and customer protection rules.

Read Below: Minimum vs Total Due • Avoid Late Fees • Credit Score Impact

1. Breakdown: Total Due vs Minimum Due vs Current Outstanding

When your monthly credit card statement gets generated, the bank usually shows three different payment figures. Many users confuse these numbers, and that confusion often leads to unnecessary interest charges.

Understanding how each amount works can easily save thousands of rupees over time –

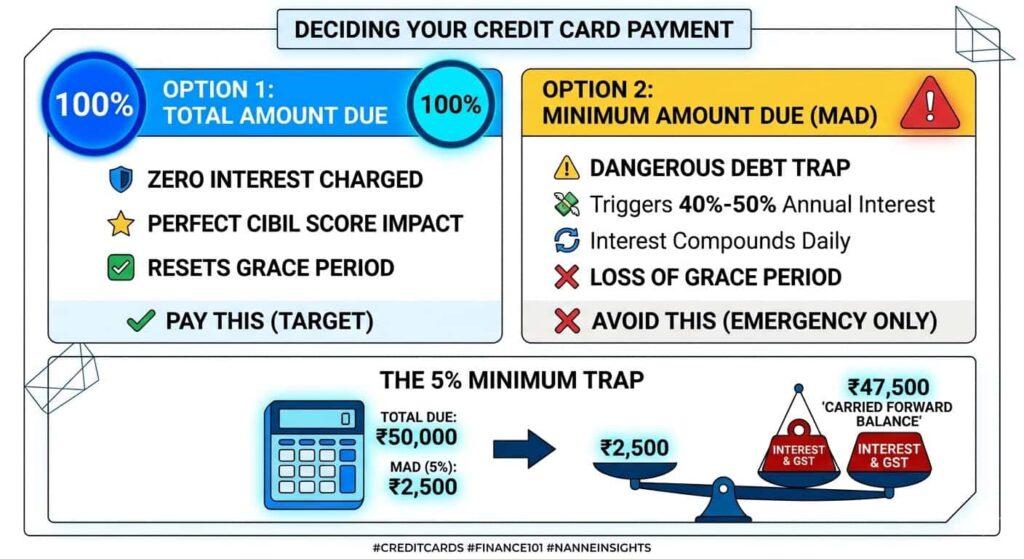

1. Total Amount Due

This is your complete billed amount for the previous 30-day statement cycle, including purchases, taxes, EMIs, or any unpaid balance carried forward from last month.

If you pay the full Total Amount Due before the due date:

- Your interest charges stay at ₹0

- Your grace period continues normally

- New purchases remain interest-free until the next cycle

In simple words, this is the safest amount to pay every month.

2. Minimum Amount Due (MAD)

This is usually around 5% of your total bill or a fixed minimum amount like ₹250, along with EMIs or overdue balances if applicable.

- Paying only the Minimum Due helps you avoid:

- Late payment fees

- Immediate negative reporting to CIBIL

But this is where many users make a costly mistake. The remaining unpaid balance immediately starts attracting very high daily interest charges, often around 35%–45% annually.

For example, if your bill is ₹50,000 and you only pay ₹2,500 as MAD, interest can start building on the remaining ₹47,500 from the next day itself.

3. Current Outstanding

This is your live card balance. It includes:

- Your statement bill

- Plus any new spending done after the statement date

You do not need to clear the entire Current Outstanding to avoid interest. Paying the statement’s Total Amount Due is usually enough.

💡 Real Human Tip: A lot of people think paying the Minimum Due means their bill is “handled.” In reality, banks earn the highest profits from users who do this regularly. Even missing full payment by a few thousand rupees can slowly turn into a heavy interest cycle after 2–3 months.

2. Real-World Case Study: The 5% Minimum Debt Trap

To understand how expensive rolling over a credit card balance can become, let’s take a practical example using a typical Indian credit card charging around 42% annual interest (3.5% monthly).

Suppose your generated statement shows a Total Amount Due of ₹50,000. Your Minimum Amount Due is calculated at 5%, which comes out to ₹2,500.

1. Scenario: Paying Only the Minimum Due

You pay ₹2,500 before the due date and assume the situation is under control. Technically, the bank will not mark your account as overdue, but the remaining balance still moves into the next billing cycle. Here’s what happens next:

- Remaining unpaid balance becomes ₹47,500

- Monthly interest at 3.5% adds roughly ₹1,662

- Additional 18% GST applies on the interest amount

- Your next bill becomes higher despite making a payment

2. The Hidden Penalty Most Users Miss

The moment you fail to clear the full Total Amount Due, your interest-free grace period usually disappears completely. That means:

- Even new purchases start attracting immediate interest

- A small ₹2,000 grocery swipe can begin generating interest from day one itself

- Future bills become harder to control month after month

💡 Real Human Insight: This is exactly how many salaried users slowly enter long-term credit card debt. It usually does not start with luxury spending — it starts with repeatedly paying only the Minimum Due thinking it is financially safe.

3. Understanding the 15/3 and 2/3/4 Credit Card Rules

Experienced credit card users often follow a few timing strategies to improve approval chances and maintain a healthier CIBIL score.

1. The 15/3 Rule

This method helps reduce your reported credit utilization ratio (CUR).

- Pay part of your bill around 15 days before statement generation

- Pay the remaining balance about 3 days before the due date

Since banks usually report the statement balance to credit bureaus, this can make your utilization appear lower and may help your credit score over time.

2. The 2/3/4 Rule

This is a popular application pacing rule used to avoid frequent credit card rejections.

- Maximum 2 card applications in 2 months

- Maximum 3 applications in 3 months

- Maximum 4 applications in 4 months

Applying for too many cards quickly can trigger automatic rejections even with a strong score.

💡 Real Tip: Many users hurt their approval chances during festive “lifetime free card” offers by applying for several cards together. Slower applications usually work better.

4. Smart Ways to Handle a Credit Card Cash Crunch

If you genuinely cannot pay the full Total Amount Due, paying only the Minimum Due should usually be your last option. Safer alternatives can reduce interest costs and protect your credit score.

- Convert Big Purchases Into EMI: Apps like Axis Mobile, HDFC MyCards, or SBI Card allow you to convert large transactions into EMIs before the due date. This can reduce your effective interest burden from 40%+ annual rates to roughly 13%–18%.

- Use Balance Transfer Offers: Some banks let you transfer existing credit card debt to another card at a lower temporary interest rate. This can provide short-term relief if you need extra repayment time.

- Make Pre-Payments Before Large Spending: If your card limit is ₹30,000 and you want to spend ₹40,000, you can pre-pay ₹10,000 into the card account first. This temporarily increases available limit without heavily impacting your credit utilization ratio.

💡 Insight: Most long-term credit card debt problems happen when users keep delaying action for several billing cycles. Handling the issue early with EMI conversion or balance transfer is usually far cheaper than paying revolving interest every month.

Frequently Asked Questions (FAQs)

What is a good amount to pay on a credit card?

The only “good” amount to pay is the absolute Total Amount Due. If you want to optimize your credit health further, paying down your current outstanding to keep your overall utilization below 30% before the statement generation date is the ideal sweet spot.

Does paying my credit card bill early hurt my credit score?

No. Clearing your bill early reduces your overall Credit Utilization Ratio (CUR) reported to credit bureaus like CIBIL. Keeping your total utilization below 30% of your total limit is highly beneficial for improving your score.

Can I pay more than the Total Amount Due on my card?

Yes. If you pay more than your bill, your account will show a negative/credit balance (e.g., -₹5,000). This extra amount acts as an advance credit and will automatically offset your future transactions.

What should I do if I cannot afford the Minimum Amount Due?

If you cannot pay the minimum, contact your card-issuing bank immediately before the due date. Ask them to convert your outstanding balance into a personal loan or a flexible 3-to-12-month EMI plan to shield your credit history from a permanent default flag.

Best tool to Use – Credit Card Late Payment Charges Calculator

Hope you liked the content. Explore smart options below 👇

🔥 Recommended