💳 Credit Card Late Payment Calculator

📊 Charges Estimate

📉 Credit Score Impact

⚠ Calculator Assumptions

Minimum Due: Usually 2–10% of statement balance.

Interest: Estimated ~3.5% per month.

Grace Period: Banks usually allow ~3 days.

Credit Reporting: 30+ days delay may affect CIBIL score.

Credit card penalties often confuse people because the extra cost does not come from just one charge. When a payment is missed, the bank may add multiple costs at the same time. These usually include a late payment fee, GST on that fee, and interest (finance charges) on the remaining balance.

So when someone checks their next statement, the total amount often looks higher than expected.

This page explains how an ICICI credit card penalty calculator works and how you can estimate the extra charges that may appear after a missed payment. By entering your outstanding credit card balance, you can get a rough idea of how much a penalty may be added in the next billing cycle.

As of 2026, most ICICI Bank credit cards follow a slab-based late payment fee system. On top of that, the bank applies monthly interest rates between 3.40% and 3.75% on unpaid balances.

This combination is the reason why even a single missed payment can quickly increase the bill.

How Late Payment Charges Work

For ICICI Bank credit cards, late payment charges depend on the Total Amount Due (TAD) mentioned in your monthly statement.

Every credit card statement shows two important numbers:

- Total Amount Due (TAD) – the full amount you need to pay

- Minimum Amount Due (MAD) – the smallest payment required to avoid late fees

The Minimum Amount Due is usually around 5% of the total outstanding balance, although the exact figure is printed in the statement each month.

If the cardholder does not pay at least the minimum amount before the due date, the bank usually adds three types of charges:

- Late payment fee

- GST on the late payment fee

- Finance charges (interest) on the remaining balance

Because all these charges apply together, the total penalty can increase faster than many cardholders expect.

ICICI Credit Card Interest Calculation Formula

When a credit card bill remains unpaid, interest is calculated on the outstanding balance. A common way to estimate the interest is through the following formula:

Interest = (Outstanding Amount × Annual Interest Rate × Number of Days) ÷ 365

This formula shows how interest builds up when the bill is not fully paid. Three factors affect the calculation:

- The total outstanding balance

- The monthly finance charge rate

- The number of days the payment is delayed

Since credit card interest is calculated daily, even a small delay can slowly increase the amount you owe.

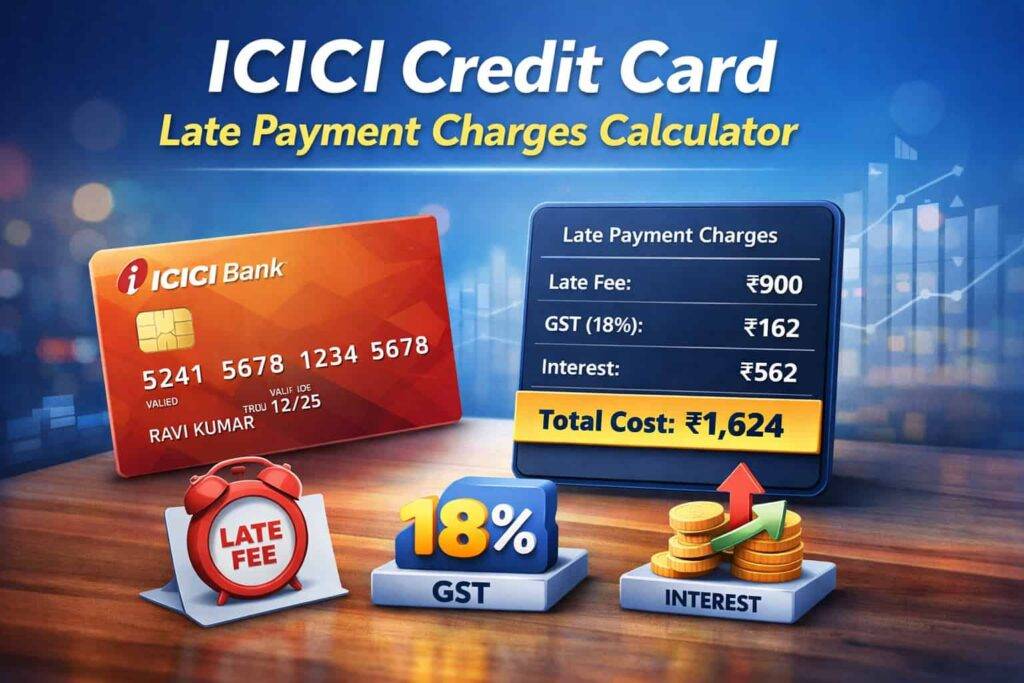

Example: ₹15,000 Credit Card Bill Not Paid

To understand this better, consider a simple example. Suppose a cardholder named Akhilesh Sharma misses the minimum payment on a ₹15,000 ICICI credit card bill.

The estimated charges could look something like this.

| Component | Amount |

|---|---|

| Late payment fee | ₹900 |

| GST on fee (18%) | ₹162 |

| Interest (~3.75% monthly) | ₹562 |

| Estimated extra charges | ₹1,624 |

So instead of paying ₹15,000, the next statement balance may increase to around ₹16,624, even if the cardholder has not made any new purchases. This example shows how quickly charges can build up once a payment is missed.

ICICI Credit Card Interest (Finance Charges)

The interest rate applied to your credit card balance depends on the type of ICICI credit card you are using. Below is an approx range of finance charges.

| Card Type | Monthly Interest | Annual Interest (APR) |

|---|---|---|

| Instant Platinum / FD-backed Cards | 2.49% | 29.88% |

| Amazon Pay / MakeMyTrip / HPCL Cards | 3.50% | 42% |

| Emirates Skywards / Manchester United Cards | 3.67% | 44% |

| Standard ICICI Credit Cards | 3.40% – 3.75% | 40.80% – 45% |

These finance charges are calculated on a daily basis, which means interest keeps adding up every day until the balance is cleared.

How ICICI Credit Card Interest Actually Works

Most ICICI credit cards come with an interest-free period of around 18 to 48 days. This means if the full statement amount is paid before the due date, no interest is charged. But the situation changes once a payment is missed.

Interest Starts From the Purchase Date

- Many cardholders assume interest begins after the due date, but that is not always the case.

- In many situations, interest is calculated from the original purchase date, not from the due date.

- This is called retrospective interest.

New Purchases Also Start Attracting Interest

- Once the interest-free benefit is lost, even new purchases made on the card can begin attracting interest immediately.

- So if someone keeps using the card after missing a payment, the total cost can grow faster.

Paying Only the Minimum Amount

- Paying the Minimum Amount Due helps avoid the late payment fee, but it does not stop interest charges.

- The remaining balance continues to attract interest until the full amount is paid.

- Because of this, financial advisors usually recommend paying the entire statement balance whenever possible.

Real Example: Cost of Missing a Credit Card Payment

Let’s take another practical example. Imagine a cardholder buys a laptop using an ICICI credit card.

| Detail | Value |

|---|---|

| Purchase date | April 1 |

| Amount spent | ₹20,000 |

| Payment due date | May 1 |

| Actual payment date | May 10 |

| Interest rate | 3.5% per month |

Because the payment was made 10 days after the due date, interest is applied starting from the purchase date.

Penalty Calculation

| Component | Calculation | Amount |

|---|---|---|

| Late payment fee | ₹10k–₹25k slab | ₹900 |

| Interest (40 days) | (20,000 × 42% × 40) / 365 | ₹920.55 |

| GST (18%) | On fee + interest | ₹327.70 |

| Total extra cost | Penalty + interest + GST | ₹2,148.25 |

So the total amount payable becomes roughly ₹22,148.25, even though the original purchase was ₹20,000 That’s a difference of more than ₹2,000 just because of a late payment.

Credit Score Impact of Late Payments

Apart from financial penalties, late payments can also affect your credit history. Banks share credit behavior with bureaus such as TransUnion CIBIL, which track repayment records. If a credit card payment remains overdue for several days, the report may show a delayed payment entry.

Possible effects include:

- Lower credit score

- Difficulty getting personal loans or home loans

- Higher interest rates on future borrowing

Even a single missed payment can temporarily reduce a strong credit score.

Simple Tips to Avoid Credit Card Late Payment Charges

Avoiding penalties is usually much easier than dealing with them later. Here are a few practical habits many credit card users follow.

1. Enable Auto-Debit

The easiest method is setting auto-debit payments through the ICICI iMobile app or internet banking. This ensures at least the Minimum Amount Due is paid automatically, preventing late payment fees.

2. Pay the Full Balance

If possible, set auto-debit for the full statement amount instead of just the minimum payment. This prevents both penalties and interest charges.

3. Track Due Dates

Keeping a reminder a few days before the payment due date helps avoid accidental delays.

4. Avoid Overspending

Using a credit card responsibly and keeping the outstanding balance low makes it easier to clear the full amount every month.

FAQs

What is the penalty for ICICI credit card late payment?

ICICI usually charges ₹100–₹1,300 late payment fee, depending on the bill amount. Example: if the statement balance is ₹10,000–₹25,000, the fee is around ₹900 plus 18% GST.

What is the 2.5% charge on a credit card?

The 2.5% charge usually refers to finance or transaction fees, like cash withdrawal or EMI conversion. Example: withdrawing ₹5,000 cash may add around ₹125 fee plus GST.

What happens if I pay my ICICI credit card bill one day late?

Even a 1-day delay may trigger interest because banks calculate charges from the purchase date. For example, a ₹20,000 balance at 3.5% monthly can start accumulating interest immediately.

What happens if I pay only the minimum amount due?

Paying the Minimum Amount Due (MAD) avoids late payment fees, but interest continues. Example: on ₹15,000 balance, the bank may still charge 3.4%–3.75% monthly interest.

Can ICICI credit card late payment charges be reversed?

Sometimes yes. If the delay is first time or just 1–2 days, customers can call ICICI support. Banks occasionally reverse ₹500–₹900 fees as a goodwill gesture.

What is ICICI credit card interest rate per month?

Most ICICI credit cards charge 3.40% to 3.75% monthly interest, equal to about 40%–45% annually. For instance, a ₹10,000 unpaid balance could add around ₹340–₹375 interest monthly.

Hope you liked the content. Explore smart options below 👇

🔥 Recommended