A credit card is not like deleting a social media app account. It is actually a running loan account in the banking system. Until you officially request closure, the card remains active in the bank database. Many people expect a direct “Deactivate Card” button online in the RBL Card Mobile Banking App, but a credit card is not a simple profile.

It is a regulated financial product, so Indian banks must follow RBI KYC and billing verification rules before closing it.

You have to close it properly; if not, Many cardholders ignore unused cards. The problem starts after 8–12 months. Here is what usually happens:

- An annual fee is charged

- GST added on fee

- Statement not checked by the user

- Late fee added

- Interest keeps compounding

After some months, a ₹500 fee becomes ₹2,000–₹4,000 outstanding. Then recovery calls begin, and the CIBIL score drops.

Good news: You do NOT need to visit a branch, and you also don’t need physical paperwork at RBL for card closure. The bank accepts a closure request through:

- Email Support

- Customer Care Support

However, as per the RBL Cares AI chatbot, there is no direct option via the RBL Card mobile app to stop it.

Things to do before closing your RBL Bank Credit Card (Important points)

Before you send closure mail, just check these points once. Many customers close fast and later face charges or a CIBIL drop. Do these first:

1) Clear full outstanding = Pay not only the billed amount, but also unbilled swipes, EMI interest and late fees. The bank only accepts closure when your balance becomes ₹0.00 in the system.

2) Close running EMIs = If “Split-n-Pay” or merchant EMI is active, first foreclose it. Normally bank charges around 3% foreclosure fee + GST on remaining principal.

3) Use or redeem reward points = After closure request, points immediately expire. Redeem them (voucher, recharge, shopping). Usually minimum 500–1000 points needed and about ₹99 + GST redemption fee.

4) Stop AutoPay & subscriptions = Remove the card from OTT apps, electricity bill, insurance and SIP payments. Closing card does not stop the service — payment will fail and company may add late penalty.

5) Download last statements = After closure, MyCard app access stops. Save at least 6–12 months’ statements for proof, tax record or dispute checking later.

6) Check credit score impact = If this is your oldest card, closing may reduce credit history and increase utilisation ratio. Try to keep overall usage below 30% to protect CIBIL score.

7) Take No-Dues Certificate = After the bank confirms closure, ask for a written NOC via email. Keep it safely — this is your legal proof if any charge appears later.

RBI rule (Good rule for customers)

As per the RBI Master Direction for cards, once you give a proper closure request and zero dues, the bank must close the card within 7 working days. If delayed, the bank has to pay about ₹500 per day penalty to you.

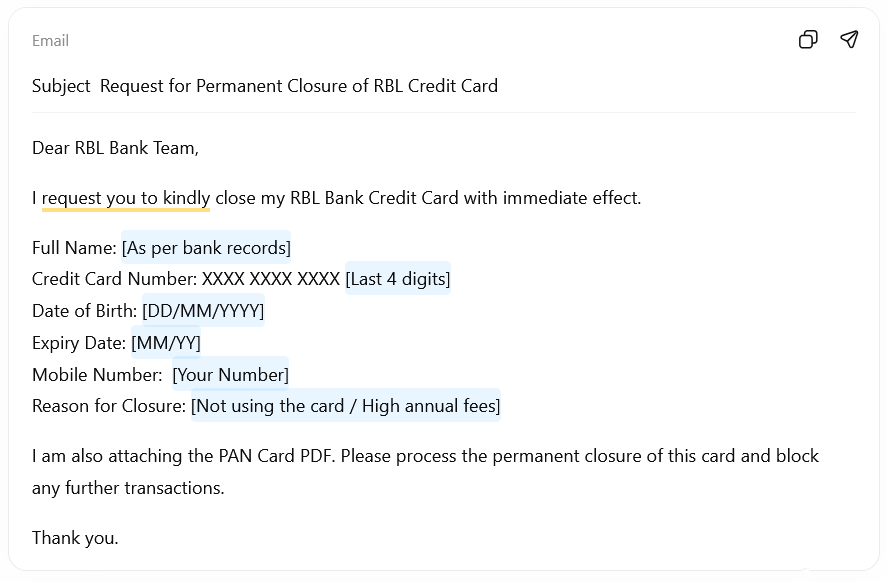

Method 1: How to Close via Email Request (Direct RBL Card Closure Method)

RBL Bank has updated its official email domain according to RBI banking domain guidelines. Earlier credit card communication was handled on @rblbank.com, but now the bank shifted to the protected banking domain.

So, for credit card closure requests, you should now send the mail to:

Official Email: 📧 cardcancellation@rbl.bank.in

Using the correct domain is important because banks are moving to “.bank.in” addresses to prevent phishing and fake support emails. Sending to the old address may delay or ignore the closure request.

Just follow this once properly, and you won’t have to call customer care again and again.

1) Open your email (Gmail/Outlook) = Create a fresh mail. Don’t reply to old promotional emails. New mail gives proper ticket creation.

2) Put the correct email address = To: cardcancellation@rbl.bank.in and Cc: cardservices@rblbank.com (Optional, but a good idea to do it) (CC helps in faster tracking from the backend team.)

3) Write a clear subject = Example subject: Subject: Request for Permanent Closure of RBL Credit Card

4) Mention your personal details (very important) = Bank identifies card only using these. Without details they will not process.

5) Ask for acknowledgement = Always request a complaint or service request number. This becomes your proof if a delay happens.

6) Send from your registered email = Try to send from the same email ID you gave while applying for the card. Otherwise bank may ask for verification again.

7) After sending, check SMS/email = Normally, within 24 hours bank generates a service token. In many cases, they block the card within 2–3 days and complete closure in about 5–6 working days.

Small Easemoney Tip: Before sending the mail, make a ₹1 small payment (or check app) to ensure a ₹0 balance. Many closure requests get rejected only because ₹100–₹200 interest is posted the next day.

Method 2: How to Close via Customer Care Call

You can also close the card by directly calling customer care. This is faster for many people because request gets registered immediately.

- RBL Bank Credit Card: +91 22 6232 7777

- Bajaj Finserv RBL SuperCard: +91 22 7119 0900

Step-by-Step Process

Step 1 — Call the helpline = Dial the number and select the Credit Card option in IVR menu.

Step 2 — Connect to executive = After IVR, your call will go to a customer care officer.

Step 3 — Ask clearly = Tell them: “I want permanent credit card closure.”

Step 4 — Verification process = They will confirm your identity. Usually they ask:

- Date of Birth

- Address

- PAN details or last 4 digits of card

Step 5 — Retention offer (very common) = The executive may try to stop you from closing. They can offer:

- lifetime free conversion

- annual fee reversal

- extra reward points

This is called a retention offer.

Step 6 — If you still want closure = Say clearly and politely: “I want permanent closure. I do not want an upgrade or replacement.”

Step 7 — Request registration =

After confirmation, the executive raises a closure request and gives you a service request number. Note it down or ask for SMS/email confirmation.

What happens next: Usually, the card is blocked the same or next day, and final closure normally completes within 5–6 working days after dues become zero.

How long does RBL Bank take to close the credit card

After you submit the request (email or call) and your dues are ₹0, the closure follows a normal sequence.

Typical Timeline

| Stage | Approx Time |

|---|---|

| Card gets blocked | 2–3 days |

| Full account closure | 5–7 working days |

| CIBIL report update | 30–45 days |

The bank is required to close the card within 7 working days once a valid request and zero balance are confirmed. After closure, always ask for a No Due Certificate (NOC) by email and save it. This is your proof if any charge appears later.

What can delay the closure?

- Pending balance = Even ₹100–₹200 interest or an unbilled EMI keeps the account active. The 7-day period starts only after all dues become zero.

- Verification call = Bank may call you to confirm identity or offer a fee waiver/retention offer. This is normal, but still, they must process closure within the timeline after confirmation.

- Secured (FD-backed) cards = If the card was issued against a Fixed Deposit, the FD lien removal usually happens about 3 working days after cancellation.

Inactive cards (important)

If a card is unused for 12 months, the bank first sends a notice. If the customer does not respond within 30 days, the bank may automatically close the card from its side.

Does closing an RBL Credit Card affect your CIBIL score?

Yes — it can affect, but not always negatively. It depends on which card you are closing and how many other loans/cards you already have. Main reasons for score changes =

1. Credit Utilisation Ratio (CUR)

- Your total credit limit reduces after closure.

- Example: you had ₹2,00,000 total limit across cards and spent ₹40,000 → usage 20%.

- After closing one card, the limit becomes ₹1,00,000 → same ₹40,000 spend becomes 40% usage, which banks don’t like.

Try to keep usage below 30%.

2. Credit history length

If the card is old (3–5+ years), it helps your score because it shows long repayment behaviour. Closing the oldest card often causes a temporary score drop.

3. Credit mix

- If you only have one card and you close it, your active credit line disappears. Lenders prefer seeing at least one running credit account.

How to check if the card is closed in CIBIL

Banks normally update credit bureaus within 30–45 days after closure.

- Step 1 — Download your report = Check your credit report from the CIBIL website or any credit score app.

- Step 2 — Find the card entry = Go to the Accounts OR Credit Accounts section and locate the RBL credit card.

- Step 3 — Confirm status = It should show: Status: Closed and Outstanding Balance: ₹0

If it still shows Active after 45–60 days

- Email or call RBL and ask if closure was reported

- Use your NOC/closure letter as proof

- Raise a dispute in the CIBIL portal (they usually resolve within about 30 days)

Practical tip

Do not close your oldest card if you have no other credit history. Instead, keep it unused with small yearly transactions (like ₹100 recharge once in 6 months). This helps maintain your CIBIL score stability.

When You Should NOT Close the Card

Do not close if:

- annual fee waived

- zero outstanding

- A high credit limit helping utilisation ratio

- good payment history

An old active card actually improves the CIBIL score because it shows long credit behaviour.

Instead of closing, you can:

- keep it unused

- Do one small transaction every 3–4 months,

- pay immediately

That keeps the account active without cost.

FAQs

How to permanently close an RBL credit card?

Send closure mail from registered email to cardcancellation@rbl.bank.in or call 022-62327777. Keep ₹0 balance first. Bank usually blocks card within 48 hours and finishes closure roughly 5–7 working days.

How can I talk to a real RBL customer care agent?

Call 022-62327777, select credit card option, then press for customer executive. Average waiting time 2–8 minutes during daytime. Evening calls after 7pm generally connect faster in most cases.

Can I close RBL credit card from the mobile app?

No full closure option inside app yet. You can block the card in MyCard app, but permanent closure still requires email or customer care request verification for security confirmation.

How to check my card is really closed?

After around 30–45 days, download your CIBIL report and see account status. It must show “Closed” and ₹0 outstanding. If still active, raise dispute using closure letter proof.