Many RBL customers feel the starting limit is small compared to their salary, but this is actually normal. RBL works on a “trust first, limit later” approach. When you are a new cardholder, the bank does not know your repayment habits yet. So instead of giving a big limit immediately, they start with a controlled amount and quietly watch how you manage it.

The bank observes mainly: you pay on time, use good utilization, and how much of the limit you use every month. After a few months of good behaviour, the bank becomes comfortable and increases the exposure.

They increase your card limit; however, this is not fixed. Sometimes, they offer 3X and above with your income or something, just a 3 to 5 thousand more than the total existing limit.

What RBL Credit Card Limit Increase mean?

An RBL credit card limit increase simply means the bank raises the maximum amount you can spend on your existing card. Your card number, rewards, and features remain exactly the same — only the approved spending capacity becomes higher.

The increase can happen in two ways:

- Automatic (Pre-Approved): The bank offers an upgrade after observing your usage. This works as an invite-only feature.

- Manual Action: You request a review and submit income proof

- loan on the card: This is a temporary loan feature, work on your card; this is not a permanent limit, it is also an invite-only feature with a minimal interest rate.

In short, the first low limit is not rejected. It is just the bank testing reliability first, and once trust is built, the higher limit follows.

Example: If your current card limit is ₹25,000 and RBL upgrades it to ₹60,000 as a pre-approved offer without paperwork, your available spending space becomes higher, and transactions stop declining during bigger purchases.

The Key factors that decide your approval (Automatic)

RBL usually does not increase the limit quickly like some other banks, such as Kotak OR IDFC. Typical timeline: rarely within the first 6 months, commonly after 7–12 billing cycles, earlier only if the profile is very strong. But before increasing your limit, RBL quietly studies your card behaviour for some months. They are not only looking at income — they want to see how you handle credit in real life.

- Low usage (CUR below ~30%) = If you keep spending within a small portion of your limit, bank feels you are managing comfortably. Using almost full limit every month makes you look dependent on credit.

- Repayment discipline = Paying full bill before due date for 6–12 months builds strong trust. Only paying minimum due reduces approval chances.

- Debt vs income (DTI ratio) = Even with good salary, if many EMIs or loans already running, the bank hesitates to give higher exposure.

- Regular and natural spending = Fuel, groceries, bill payments, and normal shopping look healthier than rare big transactions. Small but important point, Consistent activity over 1–2 months sometimes triggers automatic offers.

- Income improvement (for manual request) = Salary hike, new job, or higher business income helps a lot — especially when you submit proof.

- Card history length = Older cards with a clean repayment record are considered safer customers, so higher limits become easier.

Important Things Many Customers Don’t Know

- Add-on cards share the same limit = If your family member uses an add-on card, the increased limit is shared between both of you.

- Loan-on-card reduces available limit = If you converted purchases into EMI or took a loan on card, that amount temporarily blocks part of your limit until repaid.

- Bank can also decrease limit = If payments become irregular or financial condition weakens, RBL may reduce the limit for safety.

- You will be notified = Approval or rejection normally comes by SMS or appears in the monthly statement.

- RBL RuPay Shared limit Card = Just like an Add-on, if you have any shared limit RBL card, such as UPI based, the limit also increase same as your primary card.

RBL is not asking “how much you earn.” They are checking “how safely you use credit.”

What are the RBL Invite-Only Limit Increase Eligibility Rules (Pre-Approved)

This type of increase you cannot apply for. RBL’s system itself selects customers after observing behaviour. When the bank feels you are a safe and valuable user, an invite SMS or app notification appears.

What actually triggers the invite

- Card age around 6–12 months = Before this, the review normally doesn’t start. Bank first wants to see how you use the card in real life.

- Clean payment history = You can pay anytime, but it should always be before due date. Even one late payment can pause the invite for months.

- Regular but controlled usage = Use the card monthly, but don’t run to full limit. Unlike very low usage or full usage, moderate spending looks healthier.

- No over-limit transactions = If you ever crossed your limit, system reads pressure. If you always stayed inside limit, trust improves.

- Improving CIBIL score = Bank checks your report quietly. If your score became better than when you first got the card, it often helps trigger review.

- Relationship with the bank = If you keep savings balance, FD, or salary account in RBL, the system treats you like a stable customer.

- Spending behaviour = Sometimes you can do a bigger purchase and clear it fully. Bank understands you can manage higher exposure, but you are not struggling.

How can I increase my RBL limit by SMS?

As per RBI guidelines, even if RBL approves a higher limit, it stays paused. Your old limit continues until you personally accept it. You must enter MPIN/OTP and give consent. If you don’t approve, nothing changes — so accept only when you know you can manage the higher limit comfortably.

- From your registered mobile, open the SMS app and send CLI to 5607011

- Works only if a pre-approved offer already exists

- You will receive a confirmation SMS and activation steps

This is the simplest option because no app login is needed.

How do I increase my credit card limit online?

To increase your RBL credit card limit, you have a couple of online options. You can either open the RBL MyCard app on your phone or, if you don’t want to install anything, simply open Google Chrome and use the RBL Cares chatbot on the bank website.

1. How to Increase using the RBL Card App

Follow these properly on mobile:

- Firstly, open the RBL MyCard app

- Log in using your 4-digit MPIN or Fingerprint

- Look at the bottom menu bar, just aside from the home button.

- Tap Exclusive Facilities.

- Scroll near the EMI Subscription section

- You will see the limit increase offer (if eligible)

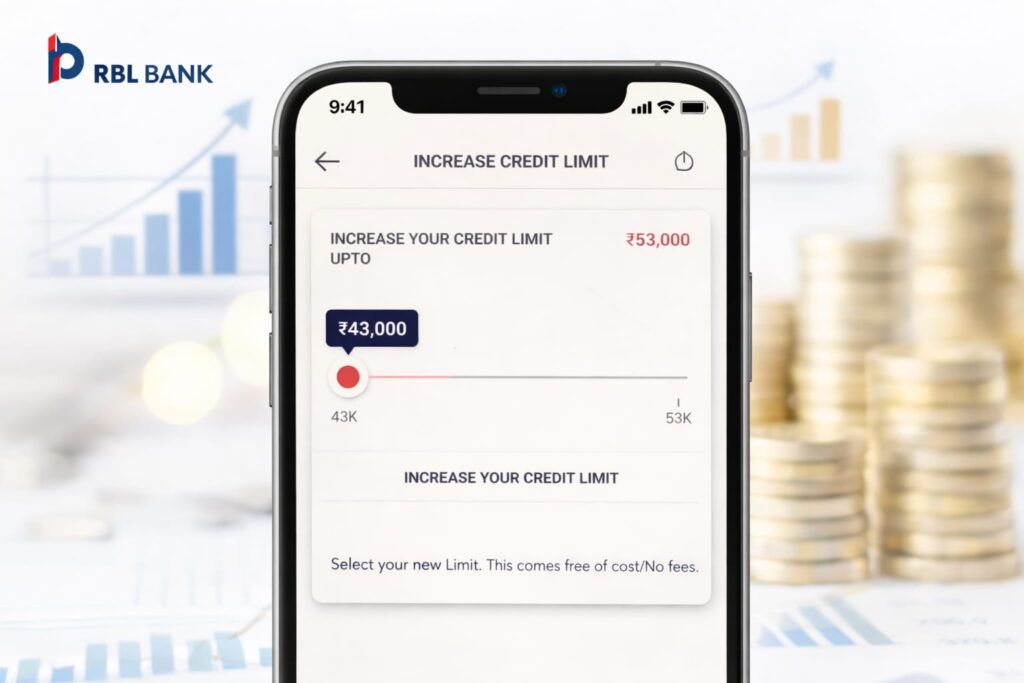

- Tap the option

- A slider appears (minimum → maximum range). Here, you can select your new.

- Select the limit you want and confirm with MPIN + OTP.

- This consent is done, your limit increase will be within 7 to 15 minutes.

You can choose a smaller or higher amount — it is your choice. There are no charges for accepting a limit increase. If the option is not showing, it means the bank has not approved yet. Then only the manual income-proof method works.

2. RBL Cares Chatbot (Website)

- Open rbl.bank.in in the browser, remember RBL recently update there domain URL as per the new RBI rules.

- Tap the floating chat icon (RBL Cares)

- Just type Hi

- Go to the Credit Card Services section.

- Select Increase Limit

- Enter card details

- Verify using mobile OTP and MPIN

- Confirm the offer

This is helpful if you don’t want to install the app.

After You Accept (What Changes), = Your spending capacity increases, the credit utilisation percentage reduces, and also, your credit profile usually improves over time. Sometimes the bank may do a credit check during review, but normally it does not harm your score when payments remain proper.

When You Should Choose Manual Limit Increase (RBL)

A manual request is useful when the bank has not sent any invite even after 12 to 18 months, but your financial position has improved. Invite offers depend on the RBL internal system, but manual review lets you show your updated earnings yourself.

You should go for a manual review if:

- You got a salary hike (around 20–30% or more)

- Recently, you changed to a better job/company

- If you need a higher limit for travel, hospital, or a big purchase

- Your CIBIL improved (around 750+ with no late payments)

- You regularly use a big portion of your current limit, but repay fully

How Manual Channel is Different

- Pre-approved invite = system decision (automatic)

- Manual request = human credit officer decision

In manual review, RBL does not rely only on card usage. They actually verify your income documents and repayment capacity, like a small loan assessment.

How to Apply (Ways Available)

- You can call helpline 022-6232-7777 and request limit enhancement. They provide you with an email ID to give a scanned copy of your salary slip and other documents.

- You can use Email from registered ID to cardservices@rblbank.com

- Submit the request through the RBL website card settings

- Visit the branch and submit a written application (for bigger limit approval)

After your request, the bank creates a service ticket and asks for documents.

Documents Required (Checklist)

| Applicant Type | Mandatory Documents | Why Bank Needs It |

|---|---|---|

| Salaried | Last 3 salary slips | Confirms current monthly income |

| Salaried | Latest Form 16 | Checks annual income stability |

| Self-employed | Latest ITR | Verifies declared earnings |

| Self-employed | Financial statements (2 years) | Business consistency |

| Both | 3–6 months bank statement | Confirms salary/business credits actually received |

| Both | PAN & ID proof (sometimes) | Identity verification during review |

How the Bank Actually Decides (Internal Steps)

- Service request created

- Documents uploaded and verified

- The officer checks the payment history on your card

- CIBIL and other loans reviewed

- Income vs existing credit calculated

- Risk score generated

- Final approval or rejection is decided

- Then you receive SMS/email.

Possible outcomes: higher limit approved, card upgrade offered, OR rejected, it all depends on your CIBIL.

Manual request is treated almost like giving you a fresh credit exposure. Bank must ensure you can repay comfortably, so they compare your income, EMIs, and credit history — not just your card usage.

How Much Time Does It Take to Increase

| Method | What Happens | Typical Time |

|---|---|---|

| SMS Invite (CLI to 5607011) | You accept pre-approved offer | Few minutes to 1 hour |

| App / Chatbot Acceptance | OTP confirmation after slider selection | Instant to same day |

| Customer Care Push | Agent checks pending offer and activates | Same day (sometimes few hours) |

| Manual Request (Email/Upload) | Documents reviewed by credit officer | 3–5 working days |

| Branch Submission | Physical documents go to card department | 5–7 working days |

Note: If documents are unclear or a verification call is missed, manual cases can take longer. Pre-approved offers are always the fastest because the bank has already internally approved your profile.

How to Increase RBL Card Limit — Real Life Do’s & Don’ts

Below are practical habits the bank actually watches. You can follow these, and the invite normally comes faster. But if you ignore them, the system keeps delaying review.

What you should do (What Helps You)

- Keep EMI load reasonable — try below ~40% of limit so bank sees breathing space

- Inform salary hike by sending latest payslip, don’t just wait

- Always pay full bill, not minimum due

- You can use multiple RBL cards, but keep overall usage low

- Wait about 6 months before asking again

- Clear outstanding balance before requesting increase

What to avoid (What Blocks Increase)

- Too many EMIs running on one card, this hurt internal system payments.

- Heavy add-on/family card spending

- Cash withdrawal from ATM using card

- Ignoring pre-approved SMS invite

- Applying many other bank cards together

- Crossing your credit limit

If usage looks controlled and repayment steady, RBL usually becomes comfortable and the higher limit follows.

FAQs

How can I increase my RBL limit by SMS?

Send CLI to 5607011 from your registered mobile number. It works only when a pre-approved offer already exists. You’ll receive confirmation SMS, then approve using OTP. No login required.

How to get a ₹5 lakh limit credit card?

Not immediate. Maintain 750+ CIBIL, 12–18 months clean repayment and income above roughly ₹60k–₹80k monthly. Banks slowly raise limits over time, unlike giving ₹5 lakh directly on new cards.

Why did RBL give me a small starting limit?

Bank first tests behaviour. For 3–6 months they watch payment timing, utilisation and penalties. If you repay full bills regularly, they normally increase automatically after trust builds.

Is there any charge for RBL credit card limit increase?

No fee for accepting limit enhancement in 2026. Charges only happen if you cross limit, delay payment or withdraw cash. The increase itself is free once approved by bank.

Does increasing the limit improve my credit score?

Yes, if spending stays same. Example: ₹20k usage on ₹40k limit equals 50% utilisation; on ₹1 lakh limit it becomes 20%. Lower utilisation generally helps CIBIL score gradually.