Most people do not wake up one fine morning and decide, “Let me close my HDFC account for fun.” Usually it starts with something like this:

- The bank keeps cutting “non-maintenance charges”.

- Salary shifted to another bank, so this account is just sitting idle.

- For six months, you haven’t used the account, but charges still continue.

At some point, the frustration reaches a level where you say: “I’m done. I want to close this account properly.” In simple words, there is always a reason for closure. let’s explore what the process HDFC offers for closure is, and what the limitations you may face are –

What are the Terms and Conditions Before You Even Think of Closure

Unlike what many customers assume, banks don’t close an account just because you verbally ask. A few basic conditions must be satisfied.

The bank will not close your account if:

- There is a negative balance or unpaid dues.

- There are active standing instructions, ECS mandates, EMIs, SIPs, or auto-payments linked to that account.

- There are linked products like a Demat/trading account, a loan repayment account, an FD sweep-in, or a locker mapped to this account.

- Your KYC documents are not in order (for example, a mismatch, an expired ID, or a missing PAN).

- Dormant account and old documents pending.

- Multiple Subscriptions are linked, such as Netflix or Spotify.

In simple terms: first settle down the account, then close it. If you skip this and directly walk into the branch, there is a high chance the staff will simply say, “Please sort this and come again.”

What are the charges for closing HDFC Bank account?

Two things are different:

- Account closure charges (selective)

- Non-maintenance OR minimum balance charges

Closing charges usually depend on how old the account is. Broadly:

| Account Age | Typical Closure Treatment |

|---|---|

| Closed within 14 days of opening | Usually no closure fee |

| Closed between 15 days and 12 months | Closure fee may apply – All citizens (Rs. 500 + GST) – Senior Citizens (Rs. 300 + GST, depending account type like BSBDA) |

| Closed after 12 months | Generally no closure fee |

Non-maintenance charges are separate. Those are deducted whenever you don’t maintain the required average balance or stop using AMB-fixed account without the balance. Over time, these deductions can push your account into the negative. This is where most people get stuck.

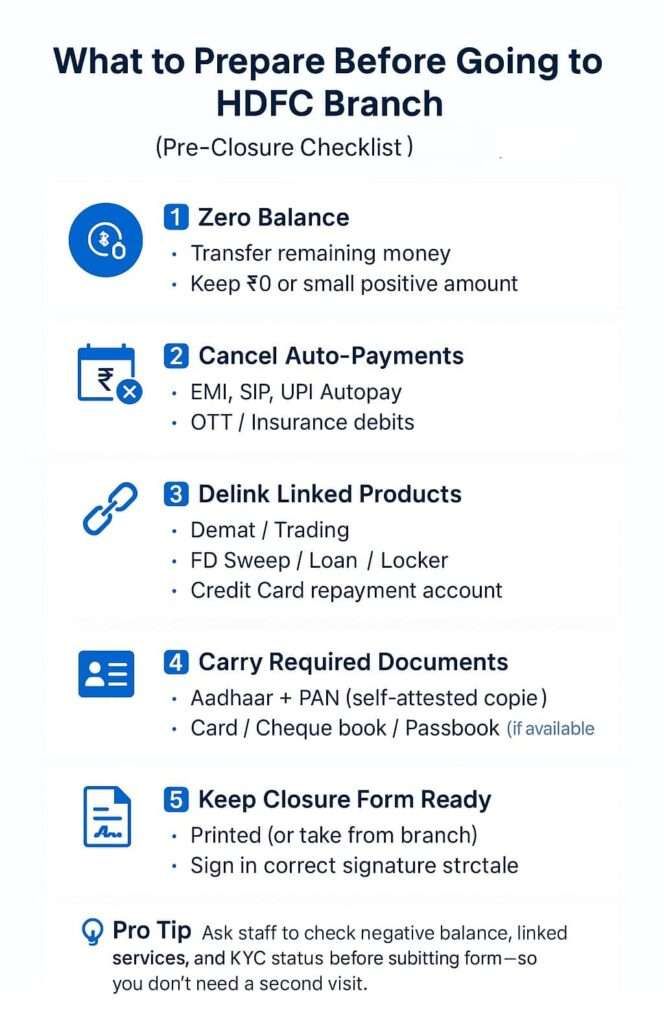

What You Should Prepare Before Going to the Branch

If you want a single-visit closure, treat this as your pre-closure checklist.

- Bring the balance close to zero – The mandatory step, simply, transfer your remaining account balance to your another bank account. Ideally, leave a very small positive balance or zero. The bank will adjust a few rupees either way. Avoid walking in with a large balance, such as Rs. 10,000, and expecting to solve everything in cash. You may find your available balance, will refund you after 5 to 6 working days, or more.

- Cancel or move auto-payments – Any EMI, mutual fund SIP, OTT subscription, insurance premium, or UPI autopay linked to this account should be switched to another account or cancelled. After closure, those instructions will fail, and then people will blame the bank.

- Check for linked products – If this is the primary account linked to a Demat/trading account, loan, credit card, FD sweep, or locker, discuss delinking or changing the primary account before closure. Otherwise, HDFC will not simply shut it.

- What documents will you require – At minimum:

- Aadhaar (original + self-attested photocopy)

- PAN (original + self-attested photocopy)

- Debit card (if you still have it, not mandatory)

- Cheque book with any unused cheques (if available)

- Passbook (if issued), Some branches may check (Optional)

A quick summary in table form:

| Item | Status Before Closure |

|---|---|

| Account balance | Zero or if you closing after 15 days and before 12 months, you may have to maintain charges with GST for closure without delay. |

| Auto-payments or EMIs | Cancelled or moved, you can use form for that. don’t worry. |

| Linked Demat / loan / locker | Delinked or planned |

| Aadhaar + PAN copies | Ready and scanned copy (Xerox is okay) |

| Closure form (optional) | Printed and signed or you can ask from branch as well. |

When all this is ready, then you start the formal process.

Official Options to Close Your HDFC Account

There are only two real routes that HDFC accepts for closing a regular savings or current account:

- Online but limited. (not roll out yet completely like payments bank)

- Branch visit with form and documents

- PhoneBanking & customer care can generate a request token, but final documentation and signatures still require a branch visit.

That’s it. No hidden option, no secret online shortcut. The branch is always involved at the final stage –

1. How to close HDFC Account “online”

Many people think: “I saw a closure form online. That must mean I can close my account online.” Despite digital banking growing rapidly in India but most of indian banks does not providing online feature, recently, IDFC First Bank and Axis Bank, they roll out basis feature for online closure.

Here’s what you can do online:

- Download the official account closure form.

- Fill it on your computer (editable PDF).

- Print it and sign it.

Here’s what you cannot do:

- You cannot press any button in the HDFC mobile app to close the account.

- You cannot find any “close account” option in HDFC NetBanking for savings/current accounts.

- You cannot simply email a filled form and get closure done without physical verification.

So we can call it “online preparation, offline closure.” You use the internet to get the form and fill it neatly, but the bank will close the account only after identity verification and physical submission at a branch. As per the HDFC chatbot, an In-person visit to a branch for account closure is primarily due to security measures, fraudulent activity control, banking KYC, and legal compliance. Also, to collect unused bank materials such as debit cards and chequebooks.

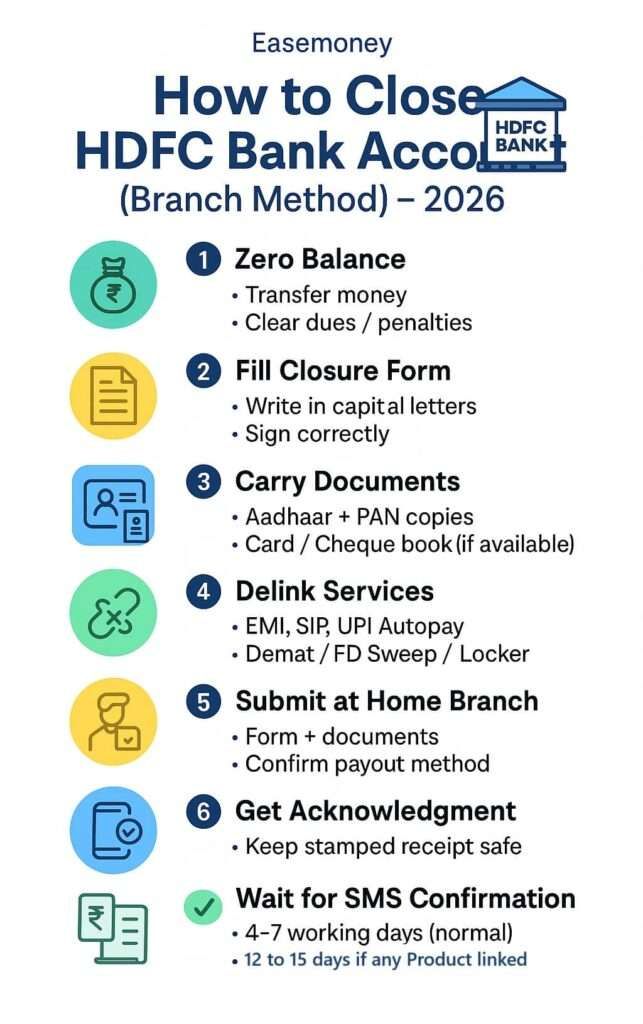

How to close an HDFC Account Correctly by visiting a Branch (step by step)

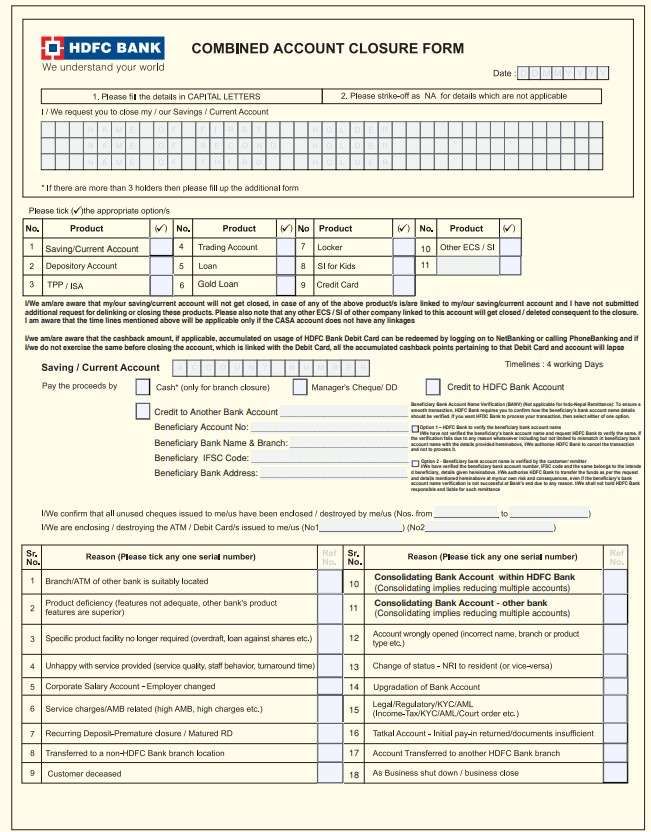

The core of the entire offline account-closing process in HDFC is one document: HDFC Combined Account Closure Form. You will need this form. This single form is used to:

- Capture all signatures and closure reasons in one place

- Close your savings or current account

- Handle linked products like Demat/trading (if any)

- Declare how any remaining balance should be paid out

You just need to fill it and submit it, here are the link to download it, HDFC offers this form in two formats:

| Form Type | Description | Best Use | Direct Link |

|---|---|---|---|

| Editable OR Fillable PDF | You can type using a PC and then print | Clean, professional filling | Original HDFC Account Closure PDF |

| Non-fillable or Static PDF | Must be printed and filled by hand | Handy for direct print and pen filling | HDFC Account closure Form (Non Editable) |

You can also ask for the same form at the branch counter. In many locations, they have it available in regional languages as well, which is helpful for family members who are more comfortable in Hindi, Gujarati, Marathi, etc.

How to Use and Fill the HDFC Account Closure Editable Form

The editable form makes your life easier if you are comfortable with a computer.

- Open the editable link in Chrome or Firefox on a computer. (smartphone does not support)

- Click on each field and type in CAPITAL LETTERS only.

- If any section or particular question does not apply to you, simply write “N/A” or strike it off later after printing.

- After filling, simply, double check your account number, spelling, and contact details.

- Tap on Print button and the form on A4 paper. (Edited Form)

- Do your physical signatures in all required places.

- Now, add your self-attested copies (Xerox) of your documents such as your Aadhaar and PAN,

- keep your original documents ready for verification at the branch. (if required)

If you use the non-fillable form, the steps are the same, except everything is handwritten and by a blue or black pen.

How to Fill the HDFC Account Closure Form (With Screenshots)

Let’s go through the important parts of the form, the fill up is way simple than it looks, here are quick steps –

Page 1 — “Customer Request” Section

| Field in Form | What You Should Enter | Example | Tips (Very Important) |

|---|---|---|---|

| Customer Name | Full legal name as per bank records | NANNE PARMAR | Use CAPITAL LETTERS only |

| Date | The date you are giving the form at the branch | 27/11/2025 | Write date in DD/MM/YYYY format |

| Type of Account to Close | Tick the correct product | Savings Account ✔ | Do not tick Credit Card or Demat if you don’t want those closed |

| Customer ID | 8-digit or 9-digit Customer ID | Found on passbook or netbanking | Do not confuse with Account Number |

| Account Number | 12–14 digit account number | 50100123456789 | Double-check digits carefully |

| Balance Handling | Tick cash or transfer or cheque | Transfer to another bank a/c | If balance is ZERO → write “N/A – Zero balance” or confirm with branch first |

| Cheque Book details | Write last issued cheque number | 000987 | If missing, write “Not Available – N/A” |

| Debit Card No. | Last 4 digits | 6521 | Write “N/A” if lost / no card |

| Reason for Closure | Simply tick any one | High AMB charges | only tick 1 |

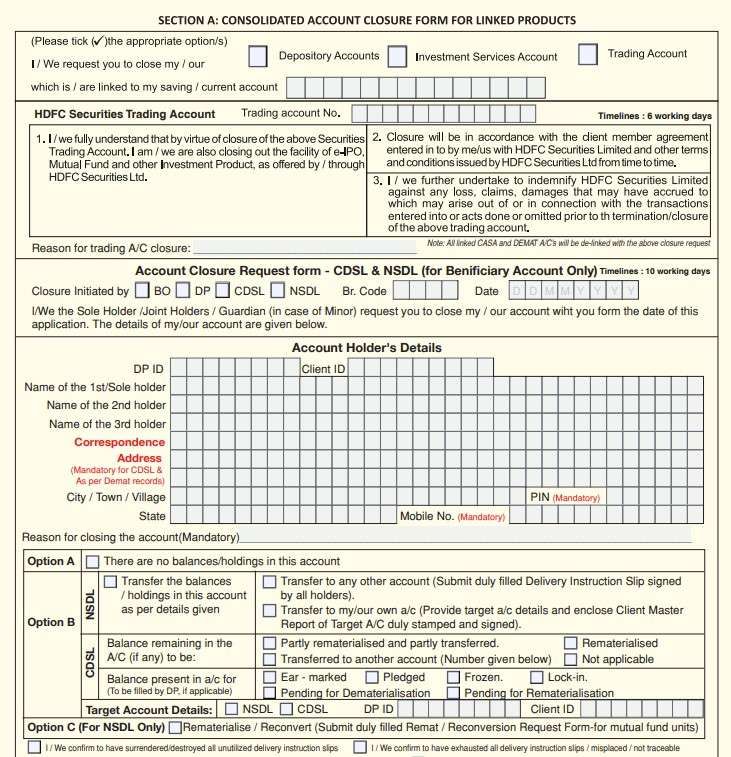

Page 2 — Section A: Linked Products & Demat

| Field | What You Should Fill | Example | Tip |

|---|---|---|---|

| Demat / Trading Account | Tick Yes/No | No | If No → write N/A in next rows |

| CDSL / NSDL DP ID | Enter only if linked | CDSL DP ID: N/A | Write N/A if you don’t trade |

| Trading A/c Number | Enter number if active | 12345678 | If unsure → ask branch first |

| Investment Products | ELSS, MF SIP, Insurance | N/A | Must delink if account supports ECS |

| Closure Type | Full closure / Delinking | Full closure | If FD sweep-in exists → bank will advise |

| Locker / Loan / Overdraft | Enter if connected | Gold Loan linked? Yes/No | Needs extra time to close if YES |

If ANY linked product is found: Closure may take 7–15 working days instead of 4 days.

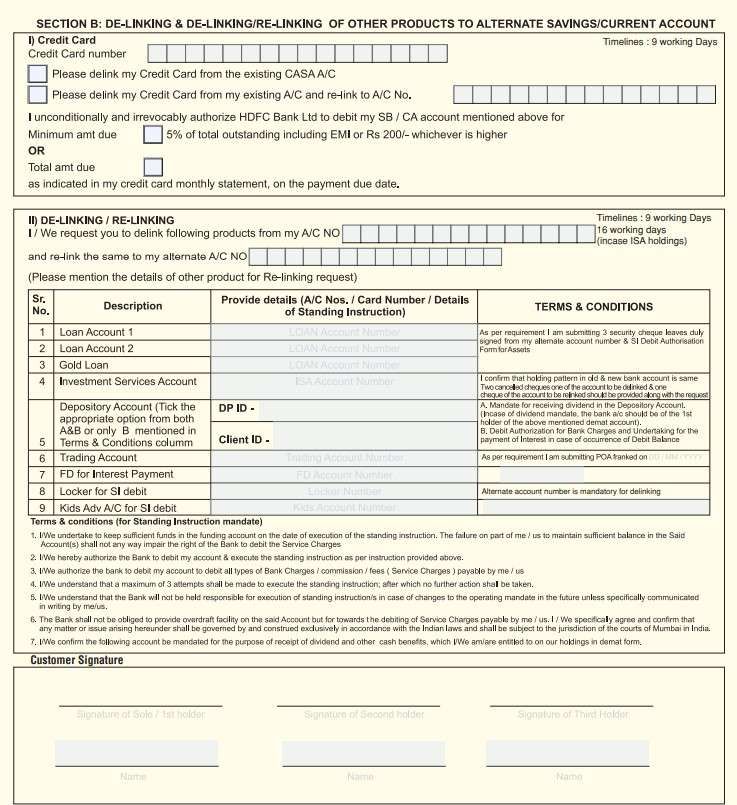

Page 3 — Section B: Delinking & Relinking to Alternate Account

This section is important only if you want to continue with Credit Card, Loan, FD, Locker while closing only the savings/current account.

| Field | Purpose | What to Write | If Not Applicable |

|---|---|---|---|

| Credit Card Number | Shift card to another account | Provide alternate account number | Write N/A if Card not linked |

| Loans (Home/Auto/Gold) | Change repayment account mandate | New account number + IFSC | Better confirm loan EMI status first |

| Deposits (FD / RD) | Sweep-in delink | Ask branch to delink | FD interest will continue unaffected |

| Other Products | Any facility tied to this account | Details if any | Write None or N/A across the rows |

Clear instruction: If you have no products to delink or relink → simply strike off the entire section and write N/A boldly.

Acknowledgement Slip (Cut & Keep Safe)

| What Branch Will Fill | Why It Matters |

|---|---|

| Date of request | Starting point of closure timeline |

| Branch stamp + name | Proof you submitted physically |

| Account Type (CASA) | Indicates savings/current |

| Expected closure date | Usually 4–7 working days,It may goes Up to 15 days if any linked products exist |

| Reference number | Needed if follow-up is required |

Keep this slip until closure is confirmed via SMS or NetBanking.

Negative Balance in HDFC Account – Quick 6-Month Story & Solution

Many HDFC customers face this issue. The account becomes unused → minimum balance is not maintained → the bank automatically deducts non-maintenance charges + GST every month. In 6 months, the account may turn –₹800, –₹1,200 or even more. Then, when you try to close it, the branch asks you to first clear the negative balance. The bank will cancel the deactivation process if a negative balance is found.

Why this happens

- You stopped using the account

- Minimum balance not maintained

- The monthly penalty keeps increasing

- You did not notice alerts or warnings

RBI View vs Reality

| What RBI Says | What Happens in Branch |

|---|---|

| Banks can charge an AMB penalty if rules disclosed | Negative must be cleared to close |

| Dormant accounts should not keep getting penalties | Waiver is possible if you request |

| No penalty allowed on BSBDA zero-balance accounts | Applies only if your account type is BSBDA |

What You Should Do

- Ask the branch for a detailed charge statement

- Request a waiver if charges are only penalties

- If a partial waiver is given, pay the small remainder

- Submit the closure form and complete the process cleanly

If you communicate clearly and politely, most branches agree to reduce or remove the negative amount — especially when the account has been genuinely unused for months.

FAQs

Can I close my HDFC Bank account without visiting the branch?

Yes. If your home branch is far, download and fill the closure form, attach Aadhaar and PAN copies, and courier it to your home branch address printed on passbook/statement.

Is there a penalty for closing a bank account in HDFC?

Only if the account is closed within 12 months of opening. After one year, there is usually no closure fee, but negative balance must be settled first.

Can I close my HDFC account permanently through email?

No. HDFC does not accept closure through email alone. Physical form with original signatures and KYC verification is compulsory for final closure approval.

Will closing my HDFC Bank account affect my credit score?

If there is no loan, no card, and no negative dues, closure will not affect the credit score. But unpaid penalties or linked cards may trigger issues.

What if my HDFC account has a negative balance, and will it affect my credit score?

If the negative balance remains unpaid for a long time or if linked credit facilities exist, it may impact your credit profile. Clear dues or request a waiver before closure for safety.

How long does HDFC actually take to close a savings account after submission?

In most cases, HDFC Bank closes accounts within 4–7 working days. If linked products exist (FD sweep, Demat, loan), closure may stretch to 10–15 days, depending on internal verification.

Will HDFC close my account if my debit card or cheque book is lost?

Yes. Lost debit cards or cheque books don’t block closure. Simply write “Lost / Not Available” in the form. The branch may block the card internally before approving the closure.

Is courier-based account closure actually accepted by HDFC branches?

Yes, but only if documents are complete. Courier the signed closure form + self-attested Aadhaar & PAN to your home branch. Expect 3–5 extra days for manual verification.

What happens if I forget to cancel UPI AutoPay before closure?

The account may still close, but future auto-debits will fail, causing service disruption. Always cancel UPI AutoPay, ECS, and SIPs before submission to avoid merchant issues later.

Does closing an unused HDFC account stop further penalty deductions?

Only after final closure. Until the account status changes to “Closed”, AMB penalties may continue. Always keep the acknowledgement slip and confirm closure via SMS or branch follow-up.

Hope you liked the content. Explore smart options below 👇