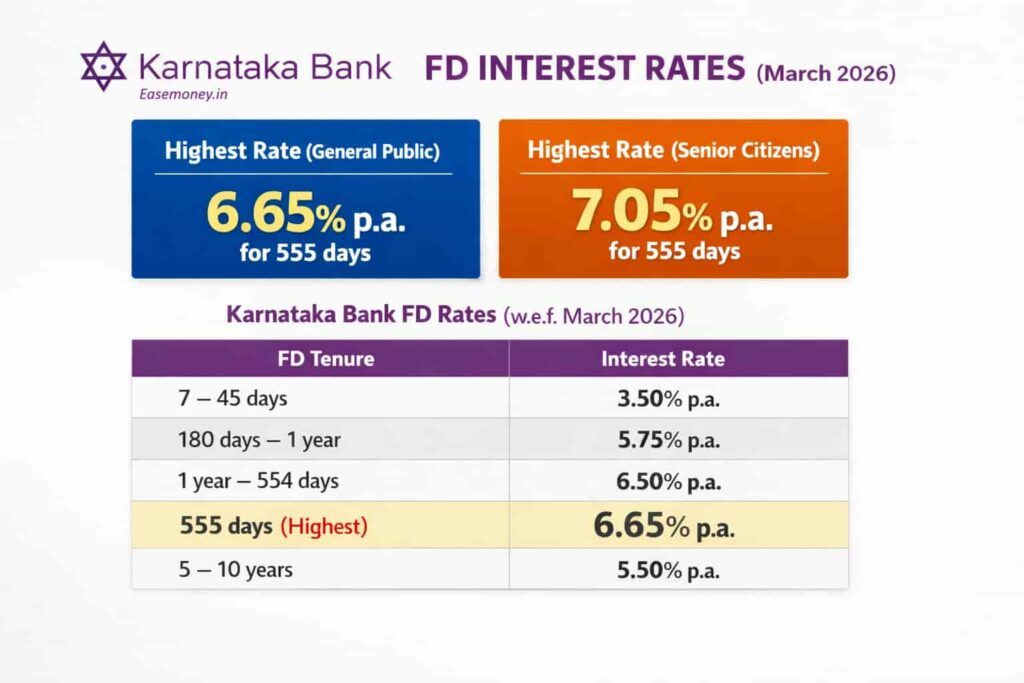

Karnataka Bank revised its Fixed Deposit (FD) rates from 1 March 2026. The new rates apply to deposits below ₹3 crore and bulk deposits as well. The bank has kept different returns based on tenure, deposit type, and customer category.

For regular customers, the interest now ranges between 3.50% and 6.65% per year. But if the depositor is a senior citizen, the return can go slightly higher — up to 7.05% annually.

Unlike many banks, where special schemes have separate rates, Karnataka Bank mostly follows the same interest slab across its FD schemes for all general indian customers. The difference usually comes from the tenure length or customer category, not the scheme name.

| Customer Type | FD Interest Range | Maximum Rate |

|---|---|---|

| General Public | 3.50% – 6.65% p.a. | 6.65% |

| Senior Citizens | 3.75% – 7.05% p.a. | 7.05% |

So if someone is planning an FD now, the highest return window sits around mid-tenure deposits, where banks usually place their peak rates.

Also, Karnataka Bank offers multiple FD options depending on deposit duration and customer needs. But the base interest structure stays largely the same across these schemes.

Updated: Karnataka Bank FD Interest Rates

Karnataka Bank applies these interest rates for Domestic and NRO callable term deposits below ₹3 crore. If the deposit size goes above ₹3 crore (up to ₹10 crore), the bank slightly adjusts the rates for bulk deposits.

Unlike many banks, where the best FD rate comes around the 1-year mark, Karnataka Bank’s peak return actually sits at exactly 555 days, which is an interesting strategy. Banks sometimes do this to control liquidity — they attract deposits for a specific tenure window instead of a common 1-year maturity.

Karnataka Bank FD Interest Rates Table (General Public) =

| Maturity Period | Retail FD (< ₹3 Cr) | Bulk FD (₹3 Cr – ₹10 Cr) |

|---|---|---|

| 7 – 45 days | 3.50% (Average) | 3.50% |

| 46 – 90 days | 4.00% | 4.00% |

| 91 – 179 days | 4.75% | 4.75% |

| 180 days – <1 year | 5.75% | 5.75% |

| 1 year – 554 days | 6.50% (Good, if you are looking 1 year) | 6.30% |

| 555 days | 6.65% (HIGHEST) | 6.50% |

| 556 days – 2 years | 6.40% | 6.20% |

| Above 2 years – 3 years | 6.15% | 6.10% |

| Above 3 years – 5 years | 6.15% | 6.10% |

| Above 5 years – 10 years | 5.50% | 5.50% |

Quick insight: If someone wants the maximum return in Karnataka Bank FD, the 555-day tenure gives the top rate of 6.65% for retail deposits.

Karnataka Bank Callable vs Non-Callable FD – Simple Meaning

Most deposits above follow the callable FD structure. A callable FD means you can withdraw or break the FD before maturity, but the bank will charge a small penalty on interest. So flexibility is there, but returns stay normal.

But if someone is okay with locking money fully, then banks offer a non-callable FD.

Non-callable FD means:

- No premature withdrawal allowed

- Money stays locked till maturity

- The bank gives a higher interest rate

Unlike small deposits, non-callable FD usually starts from ₹2 crore or higher, because banks prefer stable long-term funds from large deposits. For example, Karnataka Bank currently offers a special 555-day non-callable FD:

| Deposit Type | Interest Rate |

|---|---|

| Regular customers | 6.90% For 555 days for deposits of 2 cr or below 3 cr. |

| Senior citizens | 7.30% (additional 0.40% benefits.) |

So if someone has large deposits and no need to touch the money, the non-callable option can give higher returns. You can verify the official rates directly on the bank website: https://www.karnatakabank.bank.in/deposit-interest-rates

Karnataka Bank FD Premature Closure Penalty

If you break a Karnataka Bank callable FD before maturity, the bank applies a penalty on the interest rate. This rule applies to Domestic, NRO, and NRE callable deposits.

| Deposit Amount | Penalty |

|---|---|

| Below ₹2 crore | 0.50% |

| ₹2 crore – ₹25 crore | 1% |

| Above ₹25 crore | Nil |

So, if your FD rate was 6.65%, after premature closure, the bank will first apply the applicable tenure rate and then reduce the penalty. Government deposits above ₹10 crore currently have no penalty. Non-callable can’t have a premature closure feature; however, some special cases can enable it. such as death, court order, OR bankruptcy.

Karnataka Bank FD Rates for Senior Citizens (from 1 March 2026)

Karnataka Bank gives extra interest benefits to resident senior citizens (age 60+) under Domestic FD and ACC schemes. But this benefit applies only to resident deposits, not for NRE, NRO, or FCNR accounts.

For short tenures 7 days to below 1 year, seniors get 0.25% extra above the regular FD rate. But if the FD tenure is 1 year to 10 years, the extra benefit becomes 0.40% per year.

Unlike normal depositors, senior citizens clearly get the best return at the 555-day FD, where the bank currently offers the highest rate of 7.05%.

Karnataka Bank Senior Citizen FD Rates

| FD Tenure | Rate (<₹3 Cr) | Insight |

|---|---|---|

| 7 – 45 days | 3.75% | Short-term parking only |

| 46 – 90 days | 4.25% | Slightly better short deposit |

| 91 – 179 days | 5.00% | Okay for 6-month planning |

| 180 days – <1 year | 6.00% | Good short-term FD |

| 1 year – 554 days | 6.90% | Strong return zone |

| 555 days | 7.05% | ⭐ Highest senior FD rate |

| 556 days – 2 years | 6.80% | Still strong |

| 2 – 5 years | 6.55% | Stable long-term return |

| 5 – 10 years | 5.90% | Lower return but longer lock |

Important note = Senior citizen extra interest does not apply to deposits above ₹5 crore anymore. Karnataka Bank removed that benefit from 1 September 2019.

Super Senior Citizen Benefit (Age 80+)

Karnataka Bank also offers a special benefit for super senior citizens aged 80 years and above.

- Designed for regular income support

- Option to receive monthly interest payouts

- No discount on interest, even with a monthly payout

But unlike regular senior FD benefits, this super senior scheme does not apply to bulk deposits or basic FD slabs. The main benefit seniors currently receive is still the 0.40% extra interest advantage above standard FD rates.

Types of Karnataka Bank FD Options (For Regular Indian Residents)

If you are a regular Indian resident, Karnataka Bank actually gives multiple FD choices. Not just the normal FD. Some are made for monthly income, some for long-term growth, and some are designed for flexible withdrawal.

Unlike many banks where FD options look almost the same, Karnataka Bank splits deposits based on how you want to use the money.

Main Karnataka Bank FD Schemes

| FD Type | What It Means | When It Makes Sense |

|---|---|---|

| Regular Fixed Deposit | Standard FD where you earn interest periodically. from 7 days to 10 years. | Good if you want a monthly or quarterly income. yes, you can set as a monthly income. |

| Abhyudaya Cash Certificate (ACC) | Interest is compounded and paid only at maturity. | Better for long-term savings growth. |

| KBL Tax Planner | Special 5-year tax-saving FD under Section 80C. | Useful if you want a tax deduction up to ₹1.5 lakh. |

| Soulabhya (Flexi FD) | Allows withdrawal in ₹1,000 units while the rest keeps earning interest. | Helpful if you want FD returns but some liquidity. |

For example, if someone wants regular interest income, a regular FD works better. But if the goal is growing money quietly for a few years, ACC usually makes more sense.

Special FD Tenure Options

Karnataka Bank also runs some special tenure FDs.

| Tenure | Why People Notice It |

|---|---|

| 444 Days FD | Mid-term FD with decent return. |

| 555 Days FD | Currently, the highest interest FD (6.65%) for general customers. |

Quick but Important FD Features

- FD deposits are insured up to ₹5 lakh under DICGC. Yes, but try to make multiple FDs of 5 lakh in banks for better safety.

- You can usually take a loan of up to 90% of your FD amount.

- If you forget to close the FD, the bank may auto-renew it for the same tenure.

So okay, if someone is choosing a Karnataka Bank FD, the real decision is simple — income, tax savings, or flexible money access. The scheme depends on that.

Karnataka Bank FD Interest Rate Calculator – What It Does

Karnataka Bank provides an online FD interest calculator that helps you estimate how much your deposit will grow before you actually invest. It is a simple tool, but useful if you want to compare different tenures and returns.

Unlike guessing maturity values manually, the calculator shows total interest earned and final maturity amount based on three main factors:

- Deposit amount

- FD tenure

- Applicable interest rate

So if someone is planning an FD, this tool quickly shows which tenure gives better returns.

How to Use the Karnataka FD Calculator

- Investment Amount: Start by entering the amount you plan to deposit. Karnataka Bank FDs can technically start from ₹100, but most people calculate using ₹10,000 or ₹1 lakh to see realistic returns. The simple logic — the higher the deposit, the higher the maturity value.

- Tenure: Choose the FD duration, which can range from 7 days to 10 years. Interest rates vary across tenures, so selecting the right period helps estimate the correct return.

- Interest Rate: Enter the applicable rate for that tenure. For example, the 555-day FD currently offers around 6.65%, which is one of the higher slabs.

- Compounding: Some deposits, like ACC, use quarterly compounding, meaning interest keeps adding to the principal, slightly increasing the final maturity value.

Real Example

Let’s say Sandeep Sharma deposits ₹2,00,000 in a 555-day FD at Karnataka Bank.

| Detail | Value |

|---|---|

| Deposit Amount | ₹2,00,000 |

| Tenure | 555 days |

| Interest Rate | 6.65% |

| Approx Maturity | Around ₹2.20 lakh (depends on compounding and payout type) |

So if Sandeep keeps the FD till maturity, he earns around ₹20,000 interest. if we compare with savings accounts, where interest is small, FD calculators show clearly how tenure and rate affect returns, which helps depositors choose the best FD option before investing.

FAQs

What is the Karnataka Bank FD rate for 1 year?

For around 1-year deposits, Karnataka Bank currently offers roughly 6.50% for general customers and about 6.90% for senior citizens, based on the interest rate table effective 1 March 2026.

How much interest will ₹1 lakh earn in Karnataka Bank FD?

If someone deposits ₹1 lakh for 555 days at 6.65%, maturity may reach roughly ₹1.10 lakh–₹1.11 lakh, depending on compounding method and payout option chosen during FD booking.

What is the interest rate for Karnataka Bank 555-day FD?

The 555-day FD currently offers the highest rate in Karnataka Bank. Regular customers earn about 6.65%, while senior citizens receive around 7.05% under the revised March 2026 interest slab.

Is FD safe in Karnataka Bank?

Yes, Karnataka Bank FDs are considered safe for most depositors. Deposits are insured up to ₹5 lakh under DICGC, the RBI-backed deposit insurance system covering bank failures in India.