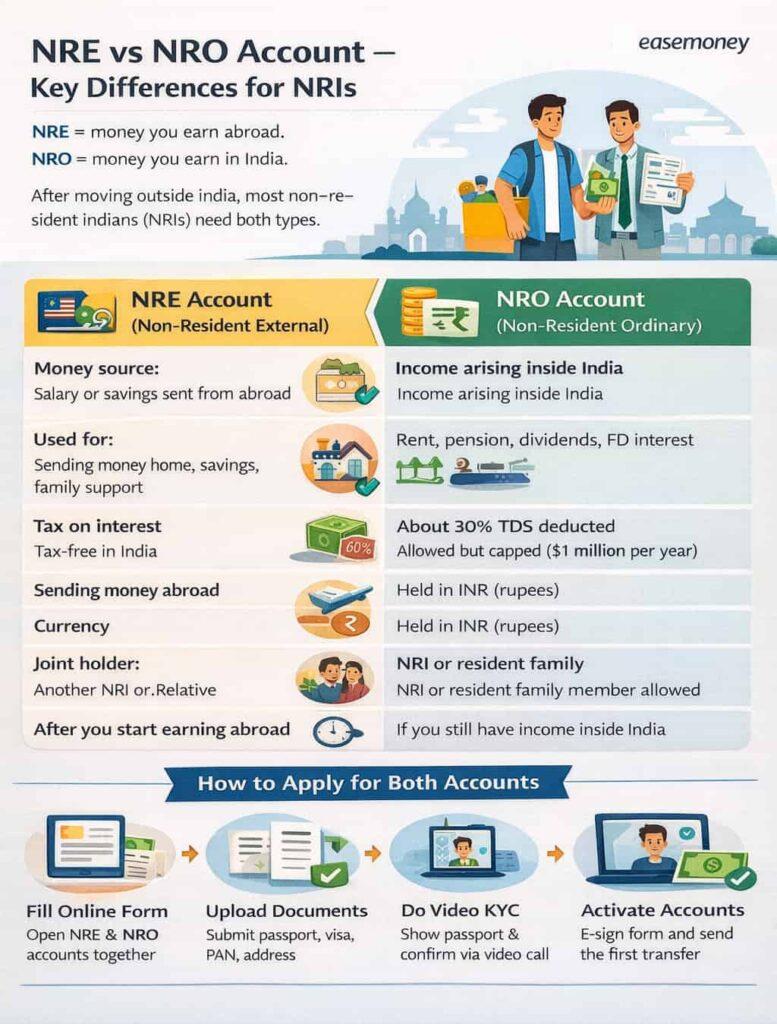

NRE and NRO accounts are designed for different types of NRI income.

An NRE account is mainly used for money earned outside India, while an NRO account is used for managing income generated within India such as rent, pension, dividends, or property sale proceeds.

Choosing the correct account helps avoid unnecessary taxes, transfer restrictions, and compliance issues.

You can also explore our detailed guide on NRI Banking in India to better understand different NRI banking options.

Below is the latest NRE vs NRO Account Comparison Table (2026).

| Feature | NRE Account | NRO Account |

|---|---|---|

| Purpose | Manage foreign income | Manage Indian income |

| Tax in India | Tax-Free | 30.90% TDS on interest |

| Repatriation | Unlimited | Up to USD 1 Million per financial year |

| Source of Funds | Foreign earnings | Indian or foreign income |

| Joint Account | Another NRI | NRI or Resident Relative |

| Currency | Indian Rupees (INR) | Indian Rupees (INR) |

📌 Important NRI Banking Rules

- NRIs must convert resident savings accounts into NRE or NRO accounts after becoming non-residents under RBI FEMA regulations

- NRE account interest is generally tax-free in India

- NRO accounts are used for rent, pension, dividends, and other Indian income sources

- Both account types are maintained in Indian Rupees (INR)

- NRE fixed deposits require a minimum tenure of 1 year; premature closure before 1 year earns no interest

💡 NRI Tax Tip: If your NRO account interest is subject to 30.90% TDS, you may be able to reduce the deduction under DTAA rules by submitting a valid Tax Residency Certificate (TRC). You can check applicable provisions through the Income Tax Department .

📌 Quick Insight: There is no restriction on maintaining both NRE and NRO accounts simultaneously. Many NRIs use an NRE account for overseas earnings and an NRO account for income generated within India.

⚠ Important: Although NRE interest is tax-free in India, it may still need to be reported under the tax laws of your country of residence, such as US FATCA or UK HMRC reporting requirements.

Read Below: NRE vs NRO • FEMA Rules • Taxation & TDS • Repatriation Limits • Account Opening Process

1. What is an NRE Account?

An NRE (Non-Resident External) Account is used for money earned outside India.

For example, if you work in Dubai, Qatar, Canada, Australia, the UK, or the USA, your salary can be sent to an NRE account. The bank converts the foreign currency into Indian Rupees and credits it to your account.

Key Points:

- Only foreign income can be deposited

- Money can be transferred from another NRE or FCNR account

- Indian income cannot be deposited

- Interest earned is generally tax-free in India

- Full repatriation is allowed

📌 Important Point: Rent income, pension, dividends, or any other income earned in India cannot be deposited into an NRE account. Doing so may create compliance issues under FEMA rules.

2. What is an NRO Account?

An NRO (Non-Resident Ordinary) Account is used to manage income earned within India after becoming an NRI. This includes:

- House rent

- Pension

- Dividends

- Interest income

- Other payments received in India

Both Indian and foreign funds can be deposited into an NRO account.

Key Points:

- Suitable for managing Indian income

- Required after NRI status is obtained

- Interest earned is taxable in India

- TDS is deducted by the bank

- Useful for paying EMIs, utility bills, maintenance charges, and local expenses

📌 Example: Rajesh moved to Dubai for work. His monthly salary is credited to his NRE account. Later, his Jaipur property started generating ₹18,000 rent per month. When the tenant sent the rent to his NRE account, the bank rejected the transaction because rent is Indian income. Rajesh then opened an NRO account, and now his rent is credited there while EMI and maintenance payments are handled from the same account.

3. Sending Money Abroad: NRE vs NRO Account Rules

One of the biggest differences between an NRE and NRO account is how easily money can be sent outside India.

(a.) NRE Account

Money in an NRE account can be transferred abroad freely.

- No upper limit on fund transfers

- Both principal and interest can be sent overseas

- No separate RBI approval is normally required

This is one reason many NRIs use NRE accounts for salary and overseas savings.

(b.) NRO Account

NRO accounts have different rules.

- Funds can be sent abroad, but limits apply

- Maximum remittance allowed is USD 1 Million per financial year

- Applicable taxes must be paid before the transfer

Documents Required

For larger NRO remittances, banks may ask for:

- Form 15CA

- Form 15CB certified by a Chartered Accountant

- Supporting documents showing the source of funds

📌 Example: Let’s say priya works in Canada and has ₹25 lakh from property sales and rent income in her NRO account. She can transfer the money abroad, but the bank may ask for tax documents and CA certificates before processing the request. The same process is usually not required for money held in an NRE account.

4. Tax Rules for NRE and NRO Accounts

The tax treatment of NRE and NRO accounts is very different. This is one of the main reasons NRIs often maintain both account types.

(a.) NRE Account: Interest is Tax-Free in India

Interest earned on NRE Savings Accounts and NRE Fixed Deposits is generally exempt from Indian income tax.

- No tax on interest earned in India

- No TDS deduction by the bank

- Popular choice for overseas salary and savings

(b.) NRO Account: TDS Applies on Interest

Interest earned on an NRO account is taxable in India.

- TDS is deducted by the bank

- The standard TDS rate can be as high as 30.90%

- Tax may apply from the first rupee of interest earned

DTAA Benefit Can Reduce Tax

Many countries have a Double Taxation Avoidance Agreement (DTAA) with India. If eligible, NRIs can submit:

- Tax Residency Certificate (TRC)

- Required declaration forms

- Other documents requested by the bank

This may help reduce the effective tax rate on NRO interest income.

📌 Example: Mr. Raj earns ₹1,00,000 as interest from his NRO Fixed Deposit. Without DTAA benefits, the bank may deduct around ₹30,900 as TDS. If Raj submits a valid TRC and qualifies under DTAA rules, the tax deduction could come down significantly, helping him keep a larger share of his interest income.

5. Joint Account Rules for NRE and NRO Accounts

If you want to open a joint account, the rules are different for NRE and NRO accounts.

(a.) NRE Account

NRE accounts have stricter rules.

- Joint holders must be NRIs or OCIs

- Resident Indians cannot be added as joint holders in a regular NRE account

- Mainly used by family members living outside India

(b.) NRO Account

NRO accounts offer more flexibility.

- An NRI can open a joint account with a resident Indian relative

- Useful for managing property income, rent, bills, and other local transactions in India

- Commonly used by NRIs who want a parent, spouse, or close family member to help manage finances

Operating Instructions Matter

When an NRI and a resident relative open a joint NRO account, banks generally use a “Former or Survivor” arrangement.

This means the NRI remains the primary account holder and operates the account during their lifetime. The resident joint holder gets access according to the account mandate and bank rules.

📌 Example: Amit works in Australia and owns a house in Pune. He opens a joint NRO account with his father so rent payments can be received and property expenses can be managed locally. This makes day-to-day banking easier without Amit having to handle every transaction from overseas.

6. How to Open an NRE or NRO Account Online

Opening an NRI account is much easier today than it was a few years ago. Most banks allow the entire process to be completed online.

1. If You Already Have an Indian Bank Account

After becoming an NRI, you should update your account status with the bank.

- Log in to your Net Banking or Mobile Banking app.

- Open the Service Request section.

- Select the option to convert your resident account into an NRI account.

- Upload your Passport, Visa or Work Permit, and Overseas Address Proof.

- Submit the request and wait for the bank’s verification.

2. If You Are Opening a Fresh NRE or NRO Account

- Visit the bank’s NRI banking page.

- Fill in the online application form.

- Select whether you want an NRE Account, NRO Account, or both.

- Upload your PAN Card, Passport, Visa, Photograph, and Overseas Address Proof.

- Complete the verification process as instructed by the bank.

- Once approved, your account will be activated.

7. Important NRI Banking Rules You Should Know {#5-costs}

Managing an NRE or NRO account is not difficult, but a few rules should not be ignored.

Update Your Account Status

If you become an NRI, your regular resident savings account should be converted to an NRE or NRO account. Continuing to use a resident account after your status changes can create compliance issues later.

NRO Money Transfer Rules

Money can be sent abroad from an NRO account, but certain limits and documentation requirements apply.

- Annual remittance limit of up to USD 1 Million

- Banks may ask for Form 15CA and Form 15CB

- Applicable taxes must be cleared before the transfer

Keep PAN Details Updated

Your PAN details should remain updated with the bank and income tax records. If PAN-related compliance is not completed, higher tax deduction rates may apply on eligible income.

📌 Common Mistake: Many NRIs update their passport and overseas address with the bank but forget to review their PAN and tax records. This can create problems later while claiming tax benefits or completing remittance requests.

8. FCNR vs NRE vs NRO: Which One Is Used For What?

All three accounts serve different purposes, so choosing the right one depends on where the money comes from and how you plan to use it.

| Account Type | Currency | Tax in India | Currency Risk | Common Use |

|---|---|---|---|---|

| NRE Account | Indian Rupees (INR) | Generally Tax-Free | Yes | Salary and savings earned abroad |

| NRO Account | Indian Rupees (INR) | Taxable | No for Indian income | Rent, pension, dividends, and other Indian income |

| FCNR Deposit | Foreign Currency | Generally Tax-Free | No | Keeping money in USD, GBP, EUR and other foreign currencies |

📌 Reality Check: Many NRIs keep both NRE and NRO accounts together. The NRE account is used for overseas earnings, while the NRO account is used for income generated inside India. FCNR deposits are usually preferred by people who do not want to take any Indian Rupee exchange-rate risk.

Frequently Asked Questions

Can an NRI keep both NRE and NRO accounts?

Yes, and actually most NRIs should keep both. Salary from abroad goes to NRE, but rent or dividend must come in NRO. Keeping only one account later creates transfer and compliance problems.

Which is better — NRE or NRO?

No account is “better.” It depends on the money source. Foreign earnings suit NRE, while India income needs NRO. In real life, people earning abroad but owning property require both together.

Can I transfer funds directly from my NRO account into my NRE account?

Yes, but it is not automated. You can transfer money from an NRO account to an NRE account only within the USD 1 Million annual repatriation cap, and you must present a signed Form 15CA and 15CB to prove that all local taxes on those funds have been paid.

Can money be transferred from NRO to NRE?

Possible, but not direct button transfer. First CA certificate and tax proof needed. After paperwork, bank allows transfer, usually within $1 million per financial year limit per person.

What is the biggest mistake NRIs make?

They continue using old savings account after moving abroad. Bank systems now check KYC regularly. Once detected, account may freeze until converted to NRO, especially after passport or visa update.

Can parents deposit money into an NRO account?

Yes, parents in India can deposit rupees into NRO. It is allowed because it is local money. But that same deposit should not go into NRE, otherwise bank may reverse transaction.

Does an NRE account charge higher maintenance fees than an NRO account?

No. Core minimum average balance (MAB) parameters and baseline transaction fees track the exact same corporate pricing matrices across most major Indian banking institutions.

Can I receive property sale money directly in NRE?

No. Property sale in India always credited to NRO first. After tax calculation and CA certificate, you can transfer abroad. Many people expect direct NRE credit and payment gets delayed weeks.

Why bank deducted tax even when income is small?

Because bank only sees interest amount, not your total yearly income. It deducts 30% TDS automatically. If total income below ₹2.5–3 lakh, filing return gives refund.

I returned to India permanently. Can I continue NRE?

After permanently returning to India, you cannot keep NRE active. Inform bank and change it to resident or RFC account. If you continue using NRE, later KYC review may restrict withdrawals or transfers.

Hope you liked the content. Explore smart options below 👇

🔥 Recommended