What is NRI Banking?

NRI banking simply means special banking arrangements in India for Non-Resident Indians who are living or working outside the country for a longer period (generally more than about 182 days in a financial year — April to March).

When you shift abroad, your money life usually does not shift completely. Salary may come in Dubai, UK, Canada, Africa, or Australia, but expenses still remain in India — parents’ support, property EMI, investments, insurance, or rent collection. A normal resident savings account is designed only for people staying in India, so banks give different accounts suited for this situation.

Banks mainly provide two types:

- NRE Account (Non-Resident External) — used to transfer foreign earnings to India. Money is fully repatriable (you can send it back abroad), and interest earned is tax-free in India.

- NRO Account (Non-Resident Ordinary) — It is used for income that arises inside India, such as house rent, pension, dividends, or FD interest.

In simple words: you live abroad, but part of your financial activity continues in India. NRI banking acts like a legal bridge, so both sides work smoothly under RBI rules.

You go abroad for work and life gets busy, so you continue using your Indian savings account exactly the way you always did.

I moved abroad, but still using my Indian savings account — is it a problem?

Yes — and this is actually a very common problem. Initially, nothing looks wrong:

- ATM withdrawals work

- UPI works

- The family uses the account normally

Because of this, many people assume conversion is optional.

However, under the Foreign Exchange Management Act (FEMA), 1999, once your residential status becomes Non-Resident Indian (NRI), a regular resident savings account is not the correct category anymore. The bank has to redesignate it. This rule applies across all banks — public or private.

1. What typically happens later

Banks do not act immediately. Accounts often run normally for months. But during periodic verification — KYC renewal, passport update, PAN linking, or detection of foreign remittance — the system identifies the overseas status.

After that, you may suddenly notice:

- debit card disabled

- online banking restricted

- transfers held for review

- sometimes a temporary freeze

This surprises people because the account worked earlier. The reason is not a penalty. it is regulatory compliance triggered by verification.

2. Risks and penalties

Ignoring the change can create complications:

- FEMA penalty: up to three times the balance amount, or roughly ₹2 lakh, where the amount cannot be determined

- Continuing fine: As per the RBI rules, there is up to ₹5,000 per day while non-compliance continues

- Operational freeze: transactions can be restricted until the status is corrected

- Tax complications: Incorrect account usage can cause reporting and taxation questions later

Most customers never reach this stage, but when it happens, your process becomes paperwork-heavy to resolve from abroad. You do not need to close Indian banking. You just need to adjust it properly: Convert your existing savings account into an NRO account and open an NRE account

Practical tip: Doing this early, ideally within a few months of moving, prevents almost all future banking interruptions. Many NRIs only act after the account stops working, which makes the process slower.

Who becomes an NRI — and why the bank asks you to change the account

NRI status is not decided by a passport. It is decided by residence. You are treated as an NRI if:

- You stay outside India for more than 182 days in a financial year, or

- You leave India for employment, business, or long-term settlement abroad

Even students going abroad for higher education are treated as NRIs for banking purposes because the intention is a long-term stay.

So when the bank asks to convert your account, it is not a punishment or a special action against you. Banks are required to maintain the correct classification of accounts.

Simple meaning: You are still allowed to keep money in India and operate banking normally — you just need the correct NRI account structure so everything remains legal and smooth long-term.

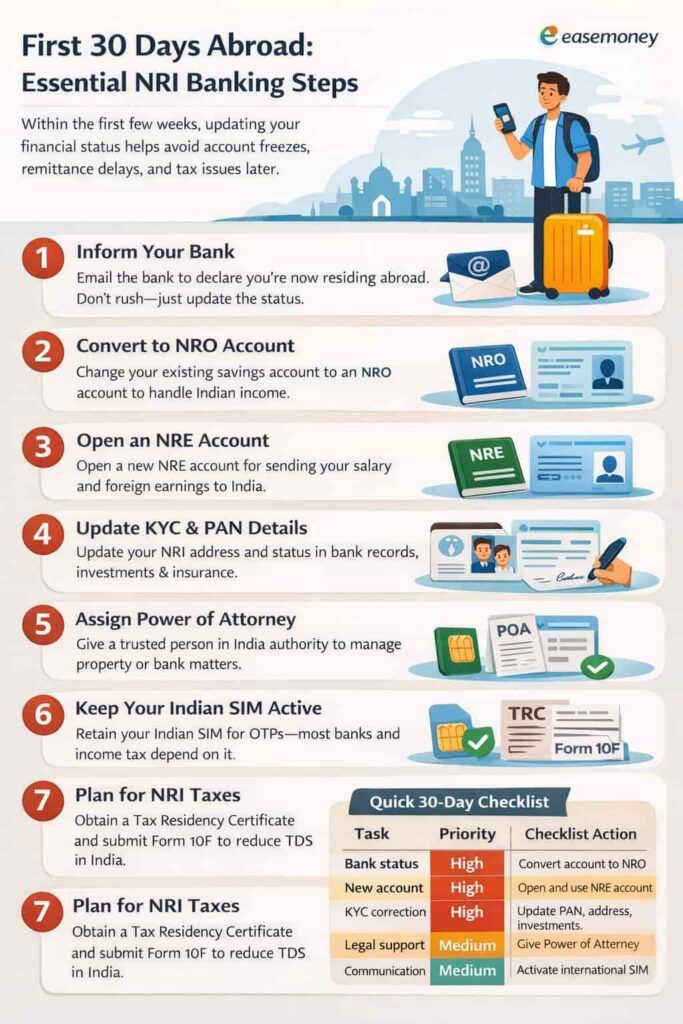

What to do in the first 30 days after going abroad

The first month abroad is actually your financial setup period. If you organise banking now, later you usually never face account freeze, remittance delay, or tax confusion.

You don’t have to panic on day one — but within 2–4 weeks, you should update your Indian financial status. According to the Foreign Exchange Management Act (FEMA), 1999, your residential status changes the moment you leave India for employment or a long-term stay. Banks then expect you to regularise your accounts.

Here is the Step-by-Step process –

1 Step: Inform your bank first

You can email the branch or raise a request through net-banking, saying you are now residing outside India. You are not closing the account — only changing its category to NRI type. The bank will guide the conversion process. First, contact your bank’s customer care or live chatbot to convert it. Most banks, such as HDFC, allow direct Account type change via Netbanking.

2 Step: Convert your savings account to NRO

Your existing savings account becomes an NRO account. Normally:

- Account number remains the same as before.

- ATM card continues or changes to an international card.

- Internet banking continues

You will use this for Indian income: rent from the property, dividends, pension, OR family deposits.

3 Step: Open an NRE account (very important)

After that, open a separate NRE account. Use it for:

- Sending your salary to India

- supporting family

- online payments or EMI

- savings in INR

Benefit: interest in NRE account is tax-free in India, and money can be sent back abroad when required (as per RBI remittance rules).

4 Step: Update KYC & PAN details

This is the step many people skip — and later face redemption or withdrawal issues. Update your overseas address and NRI status in:

- bank records

- Demat account

- mutual funds

- insurance policies

As per RBI KYC guidelines and SEBI investor rules, records must reflect correct residency to avoid incorrect taxation or transaction holds.

5 Step: Appoint a trusted person (Power of Attorney)

If you own property, a locker, or physical paperwork in India, appoint a trusted family member through a Power of Attorney (PoA). This helps for:

- document signing

- property registration

- bank locker operation

Otherwise, small work may require international travel unnecessarily.

6 Step: Keep your Indian mobile SIM active

Very practical point — keep your Indian SIM with international roaming. Most Indian banking OTPs, Aadhaar verification, DigiLocker, and income-tax login still depend on that number. Without it, online banking becomes frustrating.

7 Step: Tax and reporting basics

Within a few months, also arrange:

- Tax Residency Certificate (TRC) in your new country

- Form 10F submission in India

According to the Double Taxation Avoidance Agreement (DTAA) rules, this helps reduce high TDS (often around 30%) deducted on NRO interest.

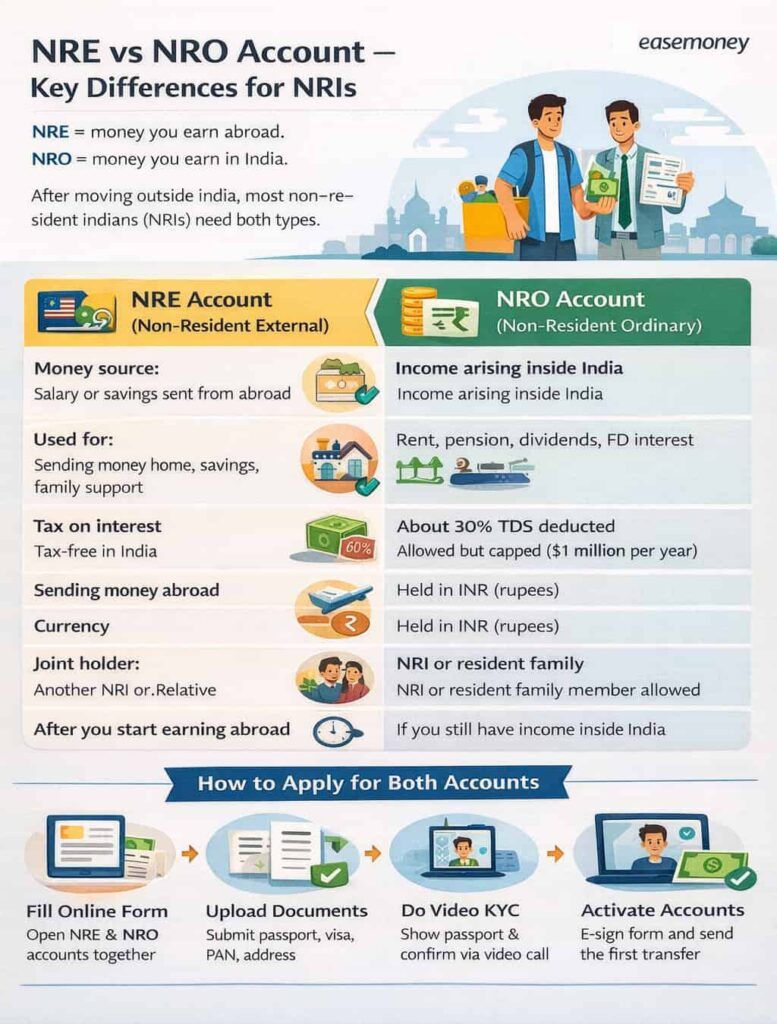

NRE vs NRO Account — What is the Difference Between Them?

The easiest way to remember:

- NRE = money you earn abroad,

- NRO = money you earn in India.

When you move outside India, you usually need both — not just one.

| Feature | NRE Account (Non-Resident External) | NRO Account (Non-Resident Ordinary) |

|---|---|---|

| Money source | Salary or savings sent from abroad | Income arising inside India |

| Used for | Sending money home, savings, family support | Rent, pension, dividends, FD interest |

| Tax on interest | Tax-free in India | About 30% TDS deducted |

| Sending money abroad | Fully allowed anytime | Allowed but capped (up to about $1 million per year) |

| Currency | Held in INR (rupees) | Held in INR (rupees) |

| Joint holder | Another NRI (or resident relative – specific rules) | NRI or resident family member allowed |

| When you need it | After you start earning outside India | If you still have income inside India |

How to Apply for NRE & NRO Accounts Digitally

In 2026, most banks (SBI, HDFC, ICICI, etc.) have fully online onboarding. You normally don’t visit a branch anymore.

- Fill the online form = Go to the bank’s NRI banking page and select “Open NRE/NRO account”. You can open both in the same application, no need to apply twice.

- Upload documents = You will upload clear scans/photos of:

- Passport (photo and address page)

- Visa/work permit/residence permit

- Overseas address proof (utility bill, bank statement, or rental agreement)

- PAN card

- Make sure names match exactly; this is where most applications get delayed.

- Video KYC (important step) = Bank schedules a short 5-minute video call. During the call, you:

- show original passport on camera

- confirm details

- Sign on blank paper and display it

- This replaces physical branch verification.

- E-sign confirmation = You approve the form using OTP on email or your Indian mobile number. (So keep your Indian SIM active — many people realise this only here.)

- Activate the account = This is the final step.

- For an NRE account, you must send the first transfer from your foreign bank (even a small amount works).

- The NRO account becomes active automatically after approval.

- Usually accounts open within 2–5 working days.

Useful tip: Link your PAN with NRI status during application. If PAN is missing or mismatched, banks deduct a higher tax on NRO interest, and later refund becomes paperwork-heavy.

NRE & NRO Account — KYC, Eligibility & Requirements

Opening an NRI account in 2026 is mostly online. Banks now use Video-KYC, so you normally don’t visit a branch. You just upload documents and verify on a short video call.

Who can open

You can apply if you fall in any category:

- NRI (living abroad for job, business, or studies — usually 182+ days outside India)

- OCI / PIO card holders

- Seafarers or offshore employees working on foreign ships or rigs

- Age: 18+ for an independent account

- Minors can open accounts through their parents/guardians

Required documents

| Document | What you upload |

|---|---|

| Identity | Passport (mandatory) |

| Status proof | Work visa/student visa/residence permit |

| Overseas address | Utility bill, foreign bank statement, or rent agreement |

| Indian proof | Aadhaar / Indian address (mainly for NRO) |

| Tax ID | PAN card (important for correct TDS) |

| Photo | Passport-size digital photo |

Important requirements

- NRE needs the first funding from abroad

- Typical minimum balance: ₹10,000–₹50,000 (varies bank)

- Joint account allowed with NRI or resident relative (“former or survivor” basis)

Tip: Match your name exactly with your passport and PAN — small spelling differences often delay approval.

How to send money to Parents OR family in India & NRE withdrawal rules

Once your NRI setup is done, sending money home becomes very easy. You don’t need to hand over ATM cards or depend on relatives travelling. You can do it yourself from your phone.

1. Normal transfer flow

- Salary comes into your overseas bank

- You send funds to your NRE account

- Then transfer to the parents’ savings account in India

You can also send directly from abroad, but many people still prefer NRE first because it keeps the money source clear.

2. Transfer methods you can use

- IMPS – instant, anytime

- NEFT – a few hours

- RTGS – same day for bigger amounts

- Parents can withdraw cash immediately after the credit.

| From country | Typical time |

|---|---|

| UAE/Gulf | minutes–2 hours |

| UK/Europe | same day |

| USA/Canada | same or next day |

Parents normally don’t pay tax because support from children is treated as a family gift.

3. Can the family withdraw from your NRE account?

Yes, but not automatically. Unlike a normal joint savings account, relatives cannot freely operate it just because they know the details. You must authorise them. You can:

- Appoint a Mandate holder or

- Give Power of Attorney (PoA)

After that, they can withdraw cash, deposit cheques, or pay household expenses in India. However, they cannot send money abroad, gift it to themselves, or close the account. If you only add a joint holder, control usually comes fully only after your lifetime.

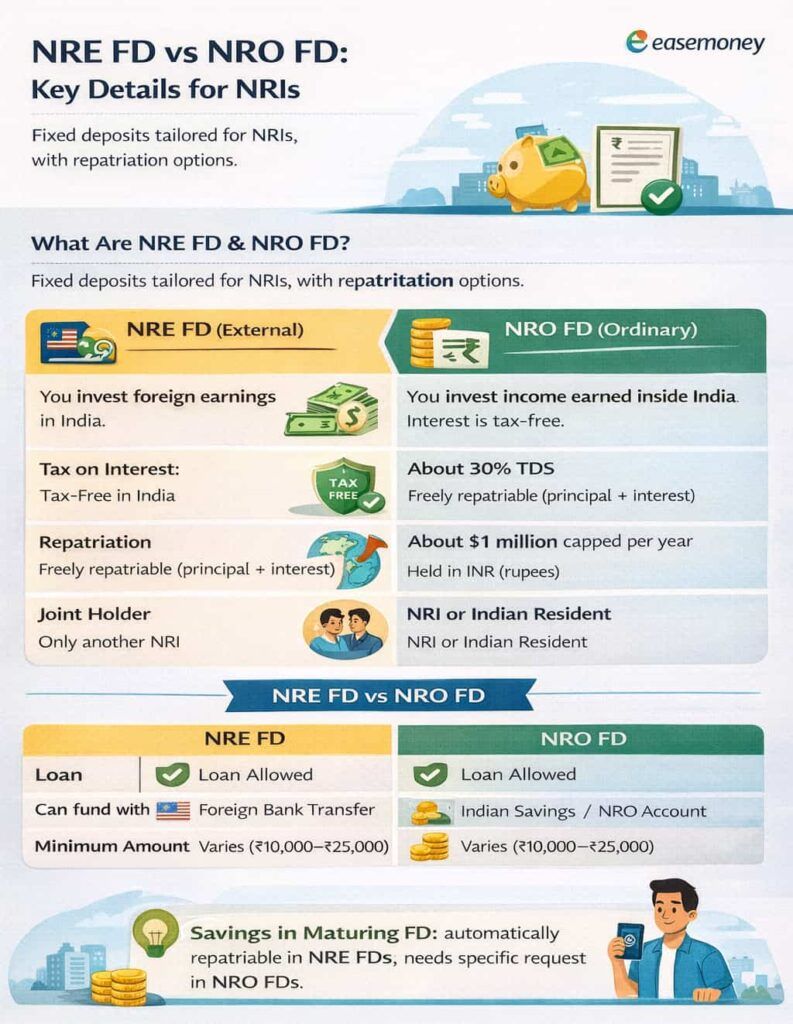

NRE FD vs NRO FD — which is better for savings

In 2026, the choice mainly depends on where your money comes from and whether you may need it back abroad later.

| Feature | NRE FD | NRO FD |

|---|---|---|

| Source of money | Foreign salary/savings | Indian income (rent, pension, dividends) |

| Tax on interest | 0% tax in India | ~30% TDS (can reduce with DTAA) |

| Repatriation | Fully transferable abroad | Limited to about $1M/year |

| Minimum tenure | 1 year | 7 days onwards |

- If you are saving money earned overseas, an NRE FD is usually better. Interest stays tax-free and you can move both principal and interest back to your foreign account anytime.

- But if the funds come from India, you normally cannot place them into NRE. Then NRO FD is the correct option, even though tax applies.

What about FCNR deposits?

Some banks also offer FCNR (Foreign Currency Non-Resident) fixed deposits. This is different from NRE/NRO because the money stays in foreign currency like USD, GBP, EUR or AED instead of converting into rupees.

Simple idea:

- NRE FD → money becomes INR

- FCNR FD → money stays in foreign currency

Many NRIs choose FCNR if they are worried about the rupee value falling. Your savings remain in dollars or other currency, and the interest is also tax-free in India while you are an NRI.

FCNR is useful if you may return abroad later or want to keep part of your savings in foreign currency. But if your future expenses are mostly in India — property, family support, investments — most people prefer an NRE FD instead.

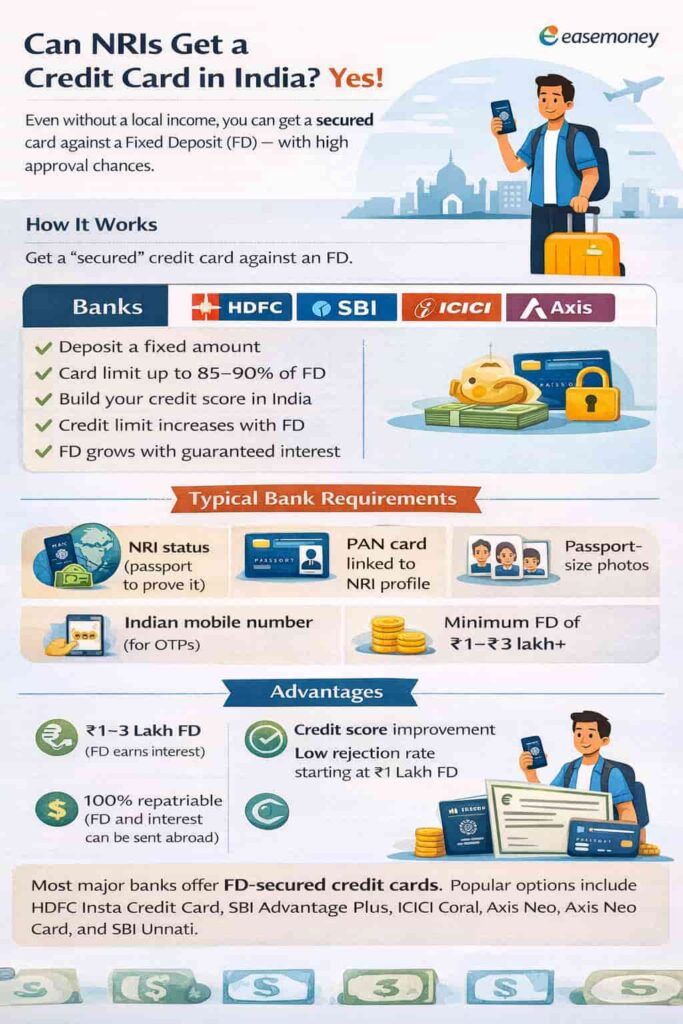

Can NRIs get a credit card in India?

Yes — in 2026, NRIs can get Indian credit cards, but the process is slightly different from that of residents. Since you usually don’t have an active Indian salary or recent credit history, banks prefer secured cards first.

How can you get one

- FD-backed credit card: Most common method. You open an NRE or NRO Fixed Deposit and the bank issues a card against it.

- Your credit limit is typically 70%–90% of the FD value.

- Relationship OR global banking: If you hold premium accounts with international banks such as HSBC or Standard Chartered (like global banking customers), some banks may approve based on foreign income and profile.

Why is it useful

- Maintains your CIBIL score in India (important if you plan a home loan later)

- Useful for shopping, fuel, and payments during India visits

- You avoid foreign card forex charges on local spending

Simple idea: start with an FD card, use it regularly, pay on time — later banks may offer normal unsecured cards.

What is the 182-Day Rule in NRI?

This rule decides who taxes your income. The Income-tax Department checks each financial year (April 1 → March 31).

- If you stay in India 182 days or more, you are treated as a Resident

- Residents pay tax on worldwide income

- NRIs pay tax only on income earned inside India

Important situation: If you leave India in October, you already stayed around 6 months in that year. So even though you are now working abroad, for that particular year India may still treat you as a resident and your foreign salary can become taxable.

If you return to India permanently

When you come back and start living in India again, your status changes from NRI to Resident. At that point, you should update your finances properly instead of continuing old NRI accounts.

- Declare foreign assets: You can still keep foreign bank accounts or property purchased while abroad, but you must report them in your Income Tax Return (ITR).

- Convert bank accounts: Your NRE and NRO accounts must be redesignated into resident savings accounts. If you still want to keep foreign currency savings, you can open an RFC (Resident Foreign Currency) account and hold dollars or other currency legally.

- Update KYC everywhere: Inform your bank, mutual funds, Demat, and insurance companies about the status change so correct tax deduction (TDS) applies.

Final checklist — what every new NRI should do

When you shift abroad, don’t rush everything in one day, but within the first few weeks you should organise your Indian banking. Small steps now prevent big headaches later.

- Convert savings to NRO: Inform the bank you are living abroad. You keep the same account, but status changes. If you delay, transactions may get restricted during verification.

- Open an NRE account (or NRE FD): Use this for sending your foreign salary. Interest is tax-free and transfers stay clean.

- Update KYC everywhere: Change status in bank, Demat, mutual funds and insurance; otherwise,FAQs withdrawals may stop unexpectedly.

- Give a mandate/PoA to a trusted person: They can handle cheque deposits or branch work while you are away.

- Keep your Indian SIM active: OTPs, Aadhaar, and income-tax logins still depend on it.

- Apply for a TRC: Helps reduce excess tax deduction under DTAA.

FAQs

What is NRI banking actually?

NRI banking means special Indian accounts (NRE, NRO, FCNR) for Indians living abroad. After you stay overseas about 182 days, banks legally require conversion. It lets you send money, invest, and support family safely.

Who is eligible to open an NRI account?

Any Indian citizen working, studying, or running business abroad can open it. Even students in 2026 qualify. OCI/PIO holders also eligible. Minimum age 18; minors allowed through parents as guardian account.

Which bank is best for NRIs in India?

There is no single best bank. If you want easy mobile banking, private banks help. But if parents visit branch often, many NRIs prefer SBI. Choose service convenience, not just interest rate.

How much money can an NRI send to India?

There is no limit for sending personal funds to India. In 2026 many people send ₹50,000–₹2 lakh monthly to parents. Transfers tagged family maintenance normally remain tax-free for receiving relatives.

Which is better — NRE or NRO account?

If money comes from your foreign salary, NRE is better because interest is tax-free and fully transferable abroad. But rent, pension, or dividends earned in India must go only into NRO account.

Can parents deposit or withdraw money in NRO account?

Yes, parents can deposit cash or cheques in your NRO account anytime. Withdrawal also possible locally. But sending money abroad from NRO needs bank paperwork and yearly limit around $1 million.

Why do NRIs still need a NRO account?

Because Indian income cannot legally enter NRE account. Example: if your house rent ₹25,000 monthly comes in 2026, bank credits only to NRO. Without it, deposits may get rejected or frozen.