Ask any bank clerk what people get wrong most often with cheques, and the answer is surprisingly simple: they don’t look at the bottom line. There are a bunch of numbers.

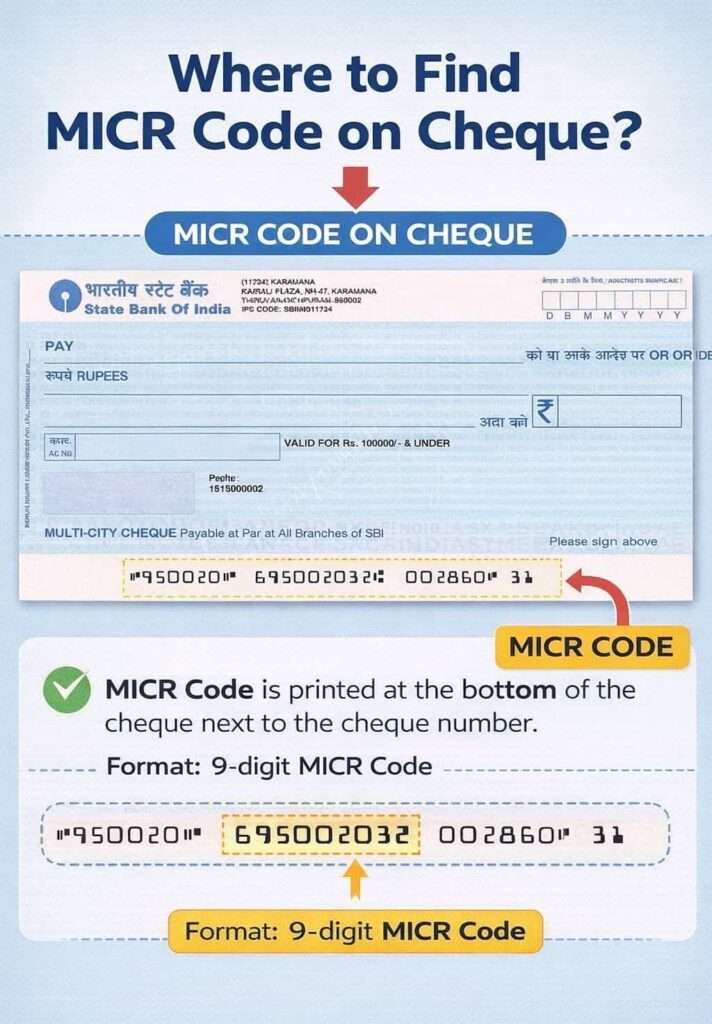

Where Is the MICR Code?

On an Indian cheque leaf, the MICR code is printed on the bottom-most line and on a white background. It appears that it uses a distinct machine-readable font and magnetic ink. It appears just between the cheque number and other transaction-related codes.

Unlike IFSC or branch details printed at the top, the MICR code is deliberately placed at the bottom so that it can be read by automated cheque-processing machines without the need for manual intervention.

If I talk in more depth, the cheque number usually goes 6 numbers, then MICR comes out with a total of 9 digits, then the transaction-related codes, which go 2 to 3 digits. The positions are –

In most cheques, the bottom line contains three visible parts:

- The cheque number (usually on the left)

- The 9-digit MICR code (in the centre)

- Additional bank or transaction identifiers (on the right)

As per the RBI, this placement is consistent across public sector banks, private banks, cooperative banks, and regional rural banks in India. Almost all banks in india for cheques. This is mandated standardisation for all automated cheque processing via the Electronic Clearing System (ECS).

Quick tip – If you are holding a cheque book, here’s a small insider insight: Check the last cheque leaf first. The print is usually cleanest there, especially in older cheque books where earlier leaves may be smudged.

What is a 9-Digit MICR Number on cheques?

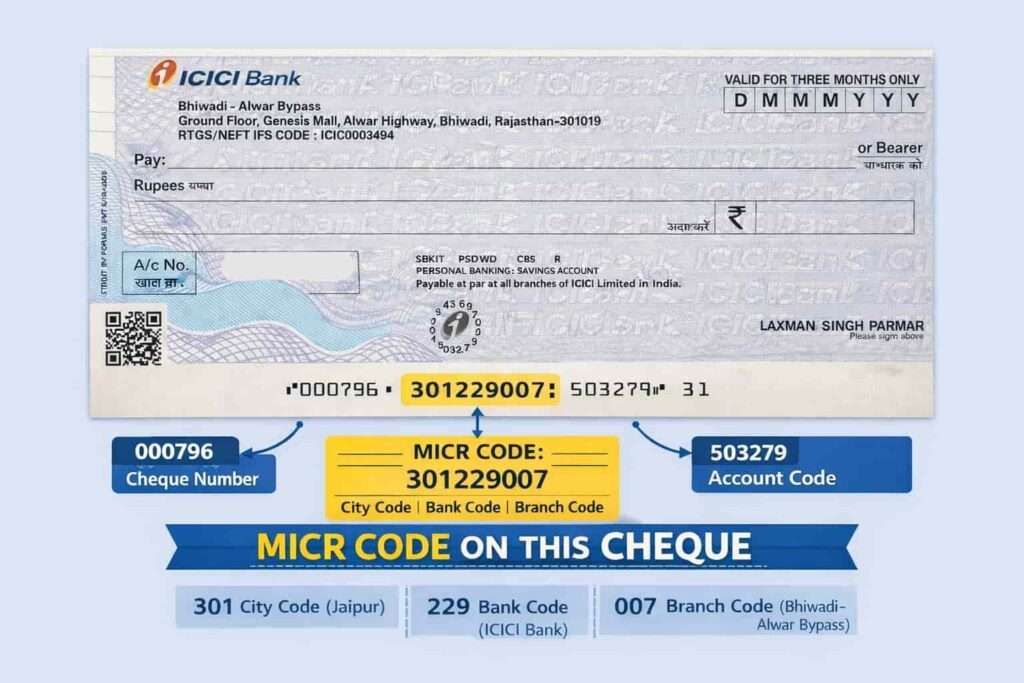

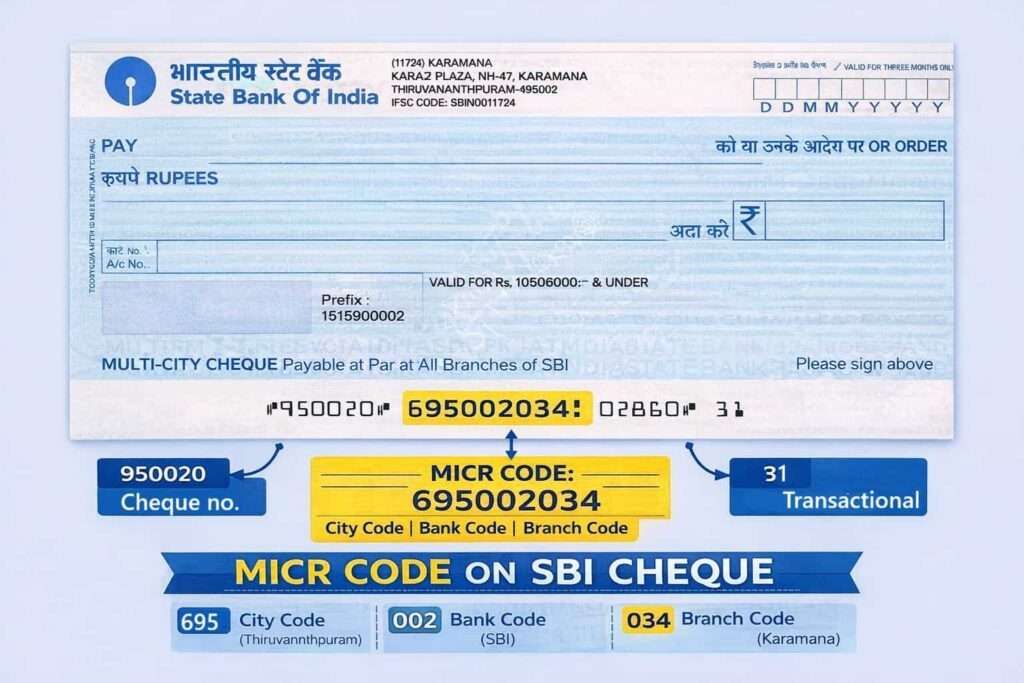

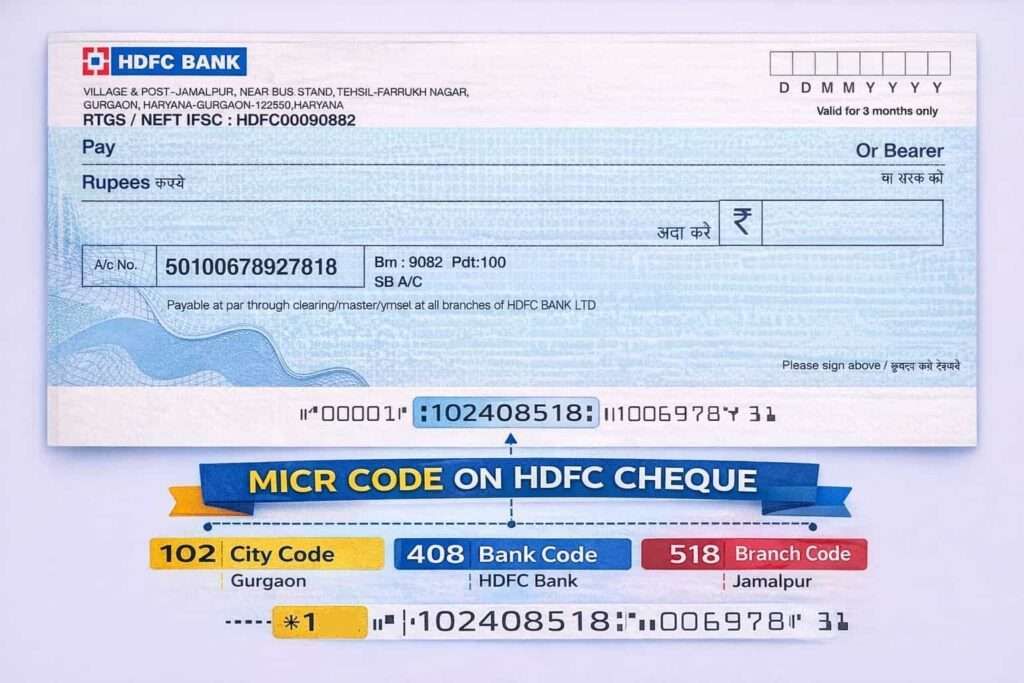

As I already said, A MICR number is a 9-digit numerical code. But let’s decode it; these numbers uniquely identify the city, bank, and branch associated with a cheque. It is not random, nor is it customer-specific. But, by choice, it acts as a routing identifier used exclusively by the banking system.

9-Digit Code Structure Explained

The MICR code is divided into three equal parts:

- First 3 digits: City Code – This represents the city where the bank branch is located. It is closely aligned with the city’s PIN code system, though it is not identical. Let me tell you simply, if your cheque MICR starts with 301 or 302, it means it is from Jaipur. Jaipur PIN code also starts with the same.

- Middle 3 digits: Bank Code – This identifies your bank itself. If I give you a few names, State Bank of India, ICICI Bank, and HDFC Bank, they all have unique bank codes.

- Last 3 digits: Branch Code – This tells the exact branch within that city. However, it is different from the IFSC Code itself.

Together, these digits allow automated systems to route cheques precisely without human intervention. It does not care who you are, how much money is involved, or why the cheque is issued. It only answers one question with certainty:

- “Which branch should this cheque reach — without a human touching it?”

How MICR Works

MICR stands for Magnetic Ink Character Recognition. The defining feature of MICR is not the number itself, but the ink used to print it. This ink has iron oxide. It allows machines to read characters magnetically, even if the cheque is stamped, signed over, or partially marked. Rarely stop cheque processing, as long as the MICR line is intact. This means – Pen marks do not block recognition, and Machine accuracy remains high even with wear and tear. So, it is fully safe.

Here’s a small detail most articles miss: MICR readers do not “read” digits the way your eyes do.

They read:

- magnetic waveforms

- signal strength

- spacing consistency

That’s why, in India, MICR technology became the backbone of cheque clearing. Also, it was long before digital banking gained popularity. It enabled banks to automate and speed up what was previously a slow, manual, and error-prone process.

Real system behaviour (bank-level):

- MICR is scanned first before signature verification

- If MICR fails → cheque may not move forward in pipeline

- If MICR passes → then CTS image + signature checks happen

This means MICR is not just a code — it is the entry gate of cheque processing.

How to Find MICR Code on an All Check or chequebook in India

Finding the MICR code on a cheque does not require you to have any banking knowledge. In simple words, the code is always printed, never handwritten, and never hidden.

To locate it, simply take your cheque on hand and –

- Turn the cheque horizontally and look at the lowest printed line

- Look for the only 9-digit uninterrupted number printed in a special font

- You can ignore logos, signatures, dates, and payee details

If the cheque is part of a cheque book, every cheque in that book will carry the same MICR code, because the branch does not change. A common misconception is that the MICR code changes from cheque to cheque.

A common misconception is that the MICR code changes from cheque to cheque. In reality:

- All cheques in the same cheque book carry the same MICR code

- The MICR code is branch-specific, not cheque-specific

- Only the cheque number changes with each leaf

This consistency helps banks correctly, it allows the process of large volumes without recalculating routing details every time someone deposits cheques.

In case the cheque is damaged or unclear, the MICR code can also be verified using:

- Bank-issued cheque book stubs

- Official bank websites

- RBI-authorised banking portals

- You can use the internet to find the correct MICR code, but safely

Note: If someone gives you a cheque, always check the MICR code on that. If it is hidden or not correctly printed, reject it and give bit ack to them.

MICR Code on ICICI, SBI, and HDFC Cheques (What to Observe)

Are you thinking, why are we talking about SBI, ICICI, and HDFC only? Let me tell you, in 2025, the Reserve Bank of India (RBI) announced the Domestic Systemically Important Banks, and these 3 banks are considered the backbone of India’s financial system. They hold most of the daily cheque transaction market value.

1. ICICI Bank Cheques

ICICI prints MICR codes with clear spacing, making them easier to identify even for first-time users. This reduces rejection during CTS scanning.

2. SBI Cheques

Given SBI’s scale, MICR accuracy is really important. Even a one-digit mismatch can route a cheque to the wrong clearing zone — which is why SBI MICR formatting is highly standardised.

3. HDFC Bank Cheques

HDFC integrates MICR tightly with CTS image quality checks. Cheques with damaged MICR lines are flagged faster than in traditional clearing.

These differences are not visible, but they matter operationally. Also, the formatting is simple and the same, so, thing special they do at large, but they do more practical and easier for all.

MICR Code vs IFSC: Clearing vs Transfers

MICR and IFSC codes sometimes confuse users, but their purposes are fundamentally different, and they look different as well.

- MICR is used for cheque clearing, and it is only 9 digits

- IFSC is used for electronic fund transfers (NEFT, RTGS, IMPS) and it is 11-digits.

MICR is read by machines during physical or image-based clearing. MICR love to live quietly in the background. But IFSC is entered manually or digitally during online transfers. One does not replace the other. IFSC interacts directly with users.

Real-Life Mistakes Banks See Every Day

From actual banking counters, these common errors are real-life issues that delay your payments via cheque:

- Writing IFSC where MICR is asked

- Assuming the cheque number equals MICR, but it is not, the cheque number is only 6 digits long.

- Submitting torn cheques with damaged MICR lines, as we already talked, this is important ink.

- Believing MICR is outdated because UPI exists.

- Using the old branch MICR after relocation

1. What Happens If MICR Code Is Wrong or Damaged?

This is something most users ignore until a cheque actually gets rejected.

Even though MICR is machine-based, it is also very sensitive to damage and accuracy. If the MICR line is incorrect or unreadable, the cheque may not even enter the clearing system properly.

Here’s what actually happens in real scenarios:

- Cheque gets rejected during CTS scanning stage

- Bank marks it as “technical return”, not financial bounce

- You may not face Section 138 directly, but payment gets delayed

- The cheque might need to be reissued again

2. Practical Insight (Important)

Unlike a signature mismatch or low balance, MICR errors are routing failures, not intent-based issues.

- No legal case starts immediately

- But repeated errors can create trust issues between parties

- Businesses often reject cheques upfront if MICR looks unclear

Tip: Always avoid folding, scratching, or stamping over the bottom line of a cheque.

Each mistake causes a delay, and it is not because the system is strict, but because it’s precise. Let’s talk last but not least, how can we ignore the history of MICR?

History and Introduction of MICR

MICR didn’t start in India. It was born in 1950s America. First developed in the 1950s, when banks began looking for ways to automate cheque handling. According to Wikipedia’s cheque history, the system was designed to handle large volumes of cheques reliably, even under imperfect physical conditions of the cheque. It came up from the feedback of the account holders, the cheque is almost like paper, so it cut, bent, wet, and more.

The success of MICR became a global standard for cheque processing

India adopted MICR much later, between 1987 and 1989. but at the perfect time. It is driven by the Reserve Bank of India. MICR-based cheque clearing was introduced in major metropolitan cities such as Mumbai, Delhi, Chennai, and Kolkata in phase 1.

Before MICR, cheque clearing in India was fully based on:

- Manual sorting

- Human verification for long weeks

- Physical movement of cheques between branches

This often resulted in delays ranging from several days to weeks. As noted by the Indian Banks’ Association (IBA), within a few years:

- clearing times dropped sharply

- inter-bank trust improved

- disputes became traceable instead of subjective

What’s important is what didn’t change: India never abandoned cheques.

Evolution of MICR with Cheque Truncation System (CTS)

When CTS-2010 launched, many experts and local people assumed MICR would fade out or drop sharply.

Under CTS:

- Cheque images are scanned

- MICR data is captured digitally

- Clearing occurs electronically

MICR did not become obsolete. But it successfully integrates into CTS workflows. It allows routing accuracy to remain intact even in a digital environment.

At the start of 2026, Cheque clearing with MICR, NCPI, and CTS – their bond makes cheque clearing almost the same day or within a few hours. RBI is working to launch a 3-Hour Confirmation Window for any cheque cleared in india.

FAQs

Why do banks still reject cheques even when the MICR code is correct?

Because MICR is only one checkpoint, not the final authority. Banks also verify image clarity (CTS), signature match, overwriting near the MICR band, and even paper quality. A perfect MICR code cannot save a cheque that fails visual or compliance checks. This surprises most people, but MICR helps routing, not approval.

What is the difference between a MICR and a non-MICR cheque?

A MICR cheque uses magnetic ink for automated clearing, while a non-MICR cheque depends on manual verification, making processing slower, riskier, and often unacceptable in modern clearing systems.

Can I cash a cheque without MICR ink?

In rare cases, banks may allow manual cashing at the home branch, but most clearing systems reject non-MICR cheques due to higher error risk and operational limitations.

Can MICR be read by humans?

Yes, humans can visually read MICR numbers, but the system is designed for machines that read magnetic signals, which banks trust more than manual interpretation.

What are the Advantages and disadvantages of MICR in cheques?

MICR enables fast, accurate cheque clearing with low fraud risk, but at same time, it requires special ink, strict formatting, and becomes unusable if the MICR line is damaged.

What are the two types of MICR?

MICR exists as physical magnetic printing on cheques and as digital MICR data captured during CTS processing, both representing the same routing information.

What happens if I print a cheque without MICR ink?

Banks usually reject such cheques because normal printing lacks magnetic properties, making them unreadable by clearing machines and invalid for standard cheque processing.

Do banks still use MICR?

Yes, banks still rely on MICR daily for cheque routing and clearing, even under CTS, especially for legal, government, and institutional cheque transactions.

Will MICR disappear as cheques decline in usage?

Unlikely in the near future. MICR is deeply embedded in legal payments, government settlements, court-mandated instruments, and institutional finance. Even if retail cheque usage falls, MICR will survive as long as cheques exist — which in India, is longer than people expect.

Why is MICR printed only at the bottom and nowhere else?

Because scanners are built for one fixed reading zone. if banks try to move MICR elsewhere would increase misreads and false rejections. This consistency is intentional and make the all process identical and fast.

Is MICR more trusted than IFSC inside banks?

For cheques — yes. IFSC relies on user input. MICR is machine-read directly from the instrument. That makes MICR less prone to customer error. Internally, banks trust system-read data more than typed data, even today.

Hope you liked the content. Explore smart options below 👇