What is a Savings Account?

A savings account is a simple and secure bank account where individuals keep their money safely and also earn small interest on it. It is one of the most basic tools in banking, giving easy access to money anytime through ATM, online transfer, or branch.

- Safe place to store money – The bank and RBI give trust here.

- Earn interest on balance

- Easy access anytime using mobile app or via branch.

1. How a Savings Account Works

- Interest earning: Your bank gives around 3% to 7% per year, calculated on daily balance and added monthly or quarterly.

- Easy access: Money can be used through ATM card, UPI, net banking, or mobile app

- Safety: Your amount is protected, and in India insured up to ₹5 lakh per person by the DICGC Scheme (RBI).

- Limits: Some banks allow 3–5 free withdrawals, and minimum balance is required for avoid any fee.

- Banking tools: Banking tools are basic part of savings account now. Almost every account comes with debit/ATM card, cheque book, and access to net banking or mobile app for payments and transfers.

- Debit/ATM card for cash withdrawal and shopping

- Chequebook for offline payments when needed

- Net banking and mobile app for bill payment, UPI, NEFT, IMPS

For example, if ₹10,000 kept in account, small interest keeps adding slowly plus your balance is secured.

2. Savings Account vs Current Account

Main difference is simple — savings account is for personal use and saving money, while current account is for business where transactions happen daily in high number.

| Feature | Savings Account | Current Account |

|---|---|---|

| Primary User | Individuals, salaried, students | Business owners, firms |

| Interest | Earns around 3%–7% | Usually no interest |

| Transactions | Limited monthly use | Unlimited deposits and withdrawals |

| Overdraft | Not common | Available to use extra funds |

| Min. Balance | Lower requirement | Higher balance needed |

Tip for You: Choose account type based on usage, not just bank suggestion or upgraded offers.

What are the Top 10 Features of Savings Account

In 2026, savings account is not just a place to keep money safe. Earlier it was like money locker, but now it works more like full financial hub. You get earning, spending, tracking, everything in one place.

- Monthly interest credit = Most banks still give interest quarterly, but some private banks like IDFC FIRST Bank now give monthly. So money grows little faster because compounding happens early.

- Auto-sweep facility = if balance goes above ₹25,000 or set limit, it automatically moves into FD for higher interest. But if you spend more, it comes back instantly, so payment not fail.

- Zero fee banking = Banks like IDFC FIRST give zero charges on ATM withdrawal (any bank), IMPS/NEFT, cheque book. But in many banks, these still have small charges. Most Small Finance banks offer low hidden charges and Zero balance.

- Higher interest slabs = Small finance banks like AU, Equitas, Ujjivan giving up to 7–8% on higher balance like ₹1 lakh or ₹5 lakh. But big banks usually give less.

- Cardless cash withdrawal = Apps like SBI YONO or ICICI iMobile allow cash withdrawal without debit card, using one-time code. Useful if card not with you.

- Video KYC account opening = Account can open from home in minutes. Bank person verifies on video call, so no branch visit needed.

- Specialised “Nari Shakti” OR Women’s Accounts = Banks like ICICI, Canara offer accounts with extra benefits like cancer insurance, cashback, lower locker charges.

- 3-in-1 account = Savings + Demat + Trading linked together. You can invest in shares or mutual funds directly from same account.

- AI money tracking = Apps like Jupiter or Fi track spending, show where money going, and even suggest saving habits.

- Kids/junior accounts = For children above 10 years, with restricted debit cards and spending control. Parents can monitor everything easily.

For example, if someone keeps ₹50,000, auto-sweep can earn more than normal savings without extra work.

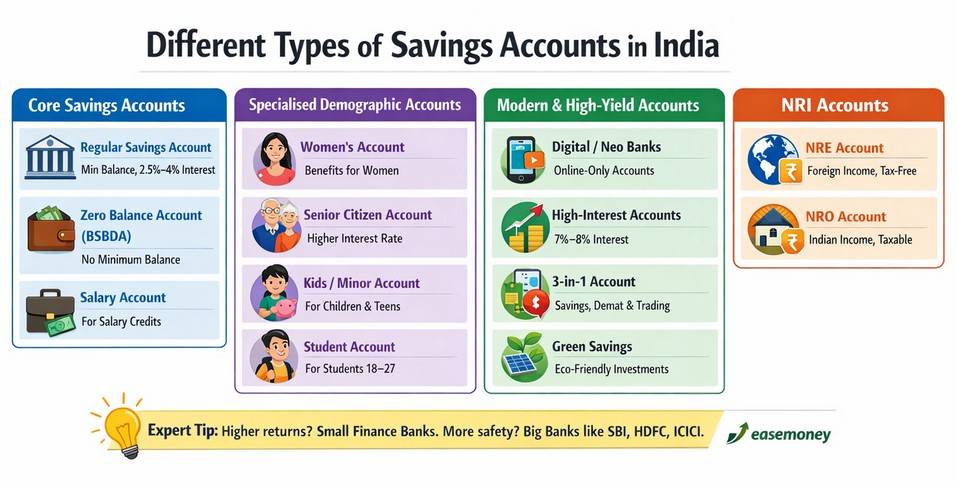

Different types of Savings Accounts in India

In India, savings accounts are mainly divided based on who is using it (like student, senior citizen, woman) and also on what features it offers (like zero-balance, digital-only, or high-interest type).

1. Core Savings Account Categories

- Regular savings account = Most common type. You have to maintain minimum balance (MAB), and interest usually comes between 2.5% to 4%. Simple and used by most people.

- Zero balance OR BSBDA account = No need to maintain balance. Banks like SBI and Union Bank provide this mainly for financial inclusion. Good for students or low-income users. As per RBI, BSBDA is the best option till now for basic savings almost no charges.

- Salary account = Opened by employer for monthly salary credit. Mostly zero balance and sometimes gives extra benefits like free insurance or better loan offers.

2. Specialised Demographic Accounts

- Women’s savings account = As per it names, it mainly designed for all required benefit for a women. benefits like health insurance, higher cashback on shopping, and lower locker rental fees..

- Senior citizen account = For age above 60. Gives around 0.50% extra interest, plus priority service and doorstep banking.

- Kids/minor account = Designed for children to learn money management, with spending limits and their own debit card.

- Student/campus account = For age 18–27. Usually low or zero balance, with more focus on digital usage.

3. Modern & High-Yield Variants

- Digital OR neo-bank accounts = Fully online accounts opened through video KYC. Apps like Jupiter, NiyoBank, or Fi give AI-based expense tracking and saving tools.

- High-yield or privilege accounts = Small finance banks like Ujjivan, North Small Finance Bank, and Equitas offer higher interest, sometimes 7%–8%, if balance is higher.

- 3-in-1 account = Combines savings, Demat, and trading account. Useful if you invest in shares or mutual funds.

- Green savings accounts = Banks like SBI and Bank of India (Harit Jama Yojana OR GREEN Scheme) use deposits for eco-friendly projects like renewable energy.

4. NRI (Non-Resident Indian) Accounts

These accounts are for Indians living outside India but still managing money here. Type depends on where income is coming from. These are NRI Banking accounts.

- NRE (Non-Resident External) = Used for depositing foreign income in INR. Interest is tax-free in India, and money can be fully sent back abroad anytime.

- NRO (Non-Resident Ordinary) = Used for income earned in India like rent or dividends. Interest is taxable, and transfer outside India has some limits.

For example, if salary coming from abroad, NRE is better, but for rent income in India, NRO is used.

Read – NRE vs NRO Account Difference

Expert Tip For You = if someone wants higher return, small finance bank account works better, but if safety and trust needed, people still prefer big banks like SBI, HDFC, OR ICICI. as per the RBI news, These three big bank hold the Too-Big-To-Fail tag.

What are the Savings Account Interest Rates in India (2026)

As of 2026, savings account interest rates in India mostly range between 2.50% to 3.50% in big public and private banks. But if you see small finance banks, they are giving much higher rates, sometimes going up to 7.5%–8.0% on higher balances.

Interest is calculated daily in most banks, but credit timing can differ. Earlier it was mostly quarterly, but now some banks started monthly credit also, which helps in better compounding.

Chart for Savings A/C Interest Rates

| Bank Category | Bank Name | Interest Rate (p.a.) |

|---|---|---|

| Public Sector | State Bank of India (SBI) | 2.70% – 3.00% |

| Union Bank of India | 2.75% – 4.20% | |

| Bank of Baroda | 2.75% – 4.50% | |

| Private Sector | HDFC Bank | 3.00% – 3.50% |

| ICICI Bank | 3.00% – 3.50% | |

| Axis Bank | 3.00% – 3.50% | |

| IDFC FIRST Bank | 3.00% – 7.25% (monthly credit) | |

| IndusInd Bank | 3.00% – 7.00% | |

| Small Finance | Equitas SFB | Up to 7.80% |

| Suryoday SFB | Up to 7.75% | |

| ESAF SFB | Up to 8.00% |

Top Banks for Savings Account in India

Banks perform differently based on user need, not just interest rate.

- Best for maximum return = Small finance banks like ESAF and Equitas leading with 7.8%–8.0%, while AU Small Finance Bank offers tier-based high returns with monthly payout option.

- Best for monthly income flow = IDFC FIRST Bank stands out because it credits interest monthly and also gives zero fee on many services.

- Top for stability and branch access = SBI has the largest branch network in India, plus digital support like YONO app, making it reliable for all types of users.

- Best for digital-first users = Kotak Mahindra Bank (811 account) gives instant digital opening, while HDFC Bank is known for strong service and wide ATM network.

- Best for tech-focused users = CICI Bank offers strong mobile banking through iMobile Pay, combining banking, bill payments, and investment in one place.

How to Choose the Best Savings Account

Choosing a savings account now is not just about nearby branch. It is about how your money works when it is sitting idle. Small details here make big difference later.

1. Check Interest Rate Slabs

Don’t just see “up to 7%”. Banks use slabs. Like 3% on ₹1 lakh, 7% only above that. Choose based on your actual balance.

2. Verify Interest Credit Cycle

Most banks give quarterly interest, but some like IDFC FIRST, AU give monthly. Monthly credit means faster compounding and regular small income.

3. Evaluate Auto-Sweep Facility

If balance crosses ₹25,000, it moves to FD and earns 7–8%, but still withdraw anytime. Good for idle money use.

4. Compare Minimum Balance

- Metro: ₹10,000–₹25,000

- Digital: ₹0 (Kotak 811, AU)

Check penalty also, sometimes charges eat interest.

5. Check Zero-Fee Banking

Some banks charge for ATM, IMPS, SMS. Better choose account with zero charges on basic services.

6. Test Mobile App

App should allow FD opening, UPI control, quick account access. If app slow, daily use becomes problem.

7. Look for 3-in-1 Option

If you invest, choose account with Demat + trading link. Makes money transfer easy and fast.

8. Confirm Safety

Bank should be RBI regulated. Deposit insured up to ₹5 lakh (DICGC). If amount higher, better split in two banks.

Insight For You: Small features like monthly credit or zero fee can save more than higher interest in long run.

What is the Easemoney savings account finder tool?

The Easemoney savings account finder tool is a simple interactive web tool that helps you choose the right bank account based on your balance, usage, and what you actually need. Instead of checking many banks one by one, this tool takes your input and shows best options quickly.

It is not like normal comparison list. This works more like decision system — checking minimum balance, interest rate, digital features, and your usage pattern, then suggesting accounts that fit properly.

In simple terms, it saves time and helps avoid wrong account choice.

How to Use the Savings Account Tool

- Step 1: Select your balance type (zero, low, medium, high)

- Step 2: Choose usage (UPI, cash, mobile app)

- Step 3: Pick purpose (daily use, savings, salary)

- Step 4: Select problem to avoid (penalty, branch visit, charges)

- Step 5: Choose benefit (high interest, basic, digital)

- Step 6: Select bank type (government, private, digital)

- Step 7: Choose user type (student, salaried, general)

- Step 8: Select opening method (online or branch)

- Step 9: Click “Find My Match”

- Step 10: Compare results and open account directly

For example, if someone selects zero balance + digital use, tool shows accounts like Kotak 811, Fi Zero Balance, or similar options.

Savings Account Charges You Must Know

Your savings account gives interest usually, but banks also recover money through different charges, penalties, and products. Many people don’t notice these, but yearly it can go into thousands if not careful.

- Minimum balance penalty (MAB) = If balance goes below ₹10,000 (urban), bank may charge ₹100 to ₹600 per month.

- ATM transaction charges = Usually, 5 free (same bank) + 3 free (other bank in metro), after that ₹21 per withdrawal, ₹10–₹11 for balance check

- Debit card annual fee = It has around ₹150 to ₹500 + GST depending on card type.

- IMPS/NEFT/RTGS charges = Online mostly free, but branch transactions cost. IMPS may charge ₹1 to ₹25.

- SMS alert charges = Around ₹15 to ₹25 + GST per quarter.

- Cheque book charges = First 10–25 leaves free, then ₹2 to ₹5 per cheque

- Cash deposit/withdrawal at branch = After 3–5 visits or ₹2 lakh limit, around ₹150 per transaction.

- Account closure charges = Closing within 1 year may cost ₹200 to ₹500. learn – how to close account without charges.

- Duplicate statement/passbook = Physical copy costs ₹50 to ₹100 per page.

- Debit card replacement fee = New card cost around ₹200 to ₹500.

Quick tip: if you misses minimum balance for 6 months, charges alone can cross ₹1,000 easily.

How to Avoid These Charges

- Simply, use your UPI app and net banking instead of branch or charges based System, such as RTGS form at branch.

- Choose zero balance account like Kotak 811 or AU Digital

- Check banks like IDFC FIRST offering zero-fee services or any special Limited time offer.

Zero Balance vs Regular Savings Account

Main difference is commitment. Regular savings account needs fixed balance always, but zero balance account gives full freedom, you can keep ₹0 without penalty.

Quick Comparison

| Feature | Zero Balance Account (BSBDA) | Regular Savings Account |

|---|---|---|

| Minimum Balance | ₹0 | ₹1,000 to ₹25,000 |

| Penalty | No charge | ₹100 to ₹600/month |

| Interest | 2.5% – 3.5% | Can go higher (up to 7%) |

| Transactions | Limited (like 4/month) | Mostly flexible |

| Target User | Students, beginners | Salaried, frequent users |

| Features | Basic tools | More benefits + perks |

Which One Should You Choose

Zero Balance Account if:

- Just starting or student

- Balance not stable

- Only using UPI or basic withdrawal

- Options: Kotak 811, AU Digital, SBI BSBDA

Regular Savings Account if:

- Can maintain ₹10,000+

- Want better interest and compounding

- Need cheque book, higher limits, premium cards

- Options: HDFC, ICICI, IDFC FIRST

Pro Tip for now: Many banks now offer “Digital Savings Accounts” that are zero-balance but still offer premium app features. Always check if a “Digital” variant is available before committing to a high-balance regular account.

Documents Required to Open Savings Account

In 2026, opening a savings account in India follows RBI KYC rules. Bank will ask for identity and address proof, so documents should match properly, otherwise your process can take longer.

1. Mandatory Documents

- PAN Card → Compulsory for normal accounts, if not available then Form 60 required

- Aadhaar Number → Mostly used as ID + address proof

- Photographs → 2–3 passport size photos needed

2. Officially Valid Documents (OVDs)

You must give at least one OVD. If one document has both photo and address, then no extra needed.

- Passport

- Voter ID

- Driving Licence

- Aadhaar Card

- NREGA Job Card

- NPR Letter

3. Address Proof (if old address in OVD)

If address not updated, then these can be used:

- Utility bills (electricity, mobile, gas – within 2 months)

- Property tax receipt

- Pension documents

- Government/employer allotment letter

4. Online / Video KYC Requirements

- Original PAN card (must show in video)

- Smartphone with camera + internet

- Blank paper and pen for live signature

- Aadhaar-linked mobile for OTP

5. Special Cases

- Minor account → Birth certificate + parent KYC

- Small account → Can open with photo + signature only (limited usage)

Keep address updated in Aadhaar to avoid extra document steps. Video KYC made process faster, but original documents still required for verification. in Video KYC, You will need very less physical doucment, but Digilocker and Aadhaar OTP must required.

How to Open a Savings Account (Step-by-Step)

After Video KYC feature and RBI new rules for digital Banking, opening a savings account is very fast. You can do it online in few minutes, or go to branch if you prefer talking to staff. Both ways work, but online is faster.

Option 1: Online via Video KYC (Fastest)

This is best if you want quick setup without visiting bank.

- Select bank & account → Go to bank website or app (Kotak 811, HDFC InstaAccount, SBI YONO)

- Enter details → Mobile number (Aadhaar linked) + email ID

- Verification → Enter Aadhaar + PAN, OTP will come for confirmation

- Fill details → Add job, income, nominee (better to add)

- Video KYC → Bank person joins call

- Show original PAN card

- Sign on blank paper

- Face photo captured live

- Activation → Account active in 2–24 hours, virtual debit card comes instantly

Option 2: Offline at Bank Branch

If you prefer physical process or Aadhaar not linked, this is better.

- Visit branch → Go between 10 AM to 4 PM on working day simply.

- Take form → Ask for account opening form (AOF)

- Fill form → Add personal, address, nominee details

- Submit documents → PAN + address proof (carry original also)

- Photos → 2–3 passport size photos

- Deposit money → If not zero balance, add minimum amount

- Verification → Bank checks details

- Get kit → In 1–3 days, you get debit card, cheque book, passbook

Important Tips

- Always add nominee, it helps family later

- Check name spelling in welcome kit

- Install mobile app and start UPI early

So if speed matters, go online. But if you want clarity or help, branch option still works better.

Top FAQs

Can I keep ₹20 lakh in a savings account?

Yes, you can keep ₹20 lakh, no limit from bank side. But only ₹5 lakh is insured (DICGC). Better split into two banks for safety and balance risk properly.

What are the 4 types of savings accounts?

Main types are regular, zero balance (BSBDA), salary account, and digital account. But banks also offer special versions like women, senior citizen, and kids accounts based on usage.

What is minimum balance in savings account?

Minimum balance depends on bank and location. Usually ₹1,000 to ₹25,000. If not maintained, bank charges ₹100–₹600 monthly, which slowly reduces your savings without notice.

Can I deposit ₹50 lakh in savings account online?

Yes, you can transfer ₹50 lakh online using NEFT/RTGS. But bank may ask source of funds. Large transactions are monitored under RBI rules for security and tax compliance.

Which bank gives zero balance savings account?

Banks like SBI (BSBDA), Kotak 811, YES Bank, AU Digital offer zero balance accounts. Good for students or low balance users who don’t want penalty charges.

Can I deposit large cash in bank account?

Yes, but if amount is high like ₹10 lakh+, bank may report to IT department. You should always have proper source proof to avoid future problem or notice.

Why banks charge ₹500 or ₹590 fees sometimes?

These charges usually come from debit card fee, SMS charges, or not maintaining balance. Many users ignore it, but yearly it becomes big amount if not checked properly.

How much money is safe in bank account?

In India, your money is legally protected up to ₹5 lakh per bank by the Deposit Insurance and Credit Guarantee Corporation (DICGC), a subsidiary of the Reserve Bank of India (RBI).

Is savings account better or FD?

Savings account gives flexibility but low return. FD gives fixed return (6%–8%) but locks money. If you need access anytime, savings better, otherwise FD works for stable growth.