To remove a lien amount from your bank account, you first need to identify why the hold was placed and then clear the pending issue, payment, or verification requirement linked to it.

A lien means the bank has temporarily blocked part of your balance. You can see the money in your account, but you cannot withdraw or transfer that specific amount until the bank releases it.

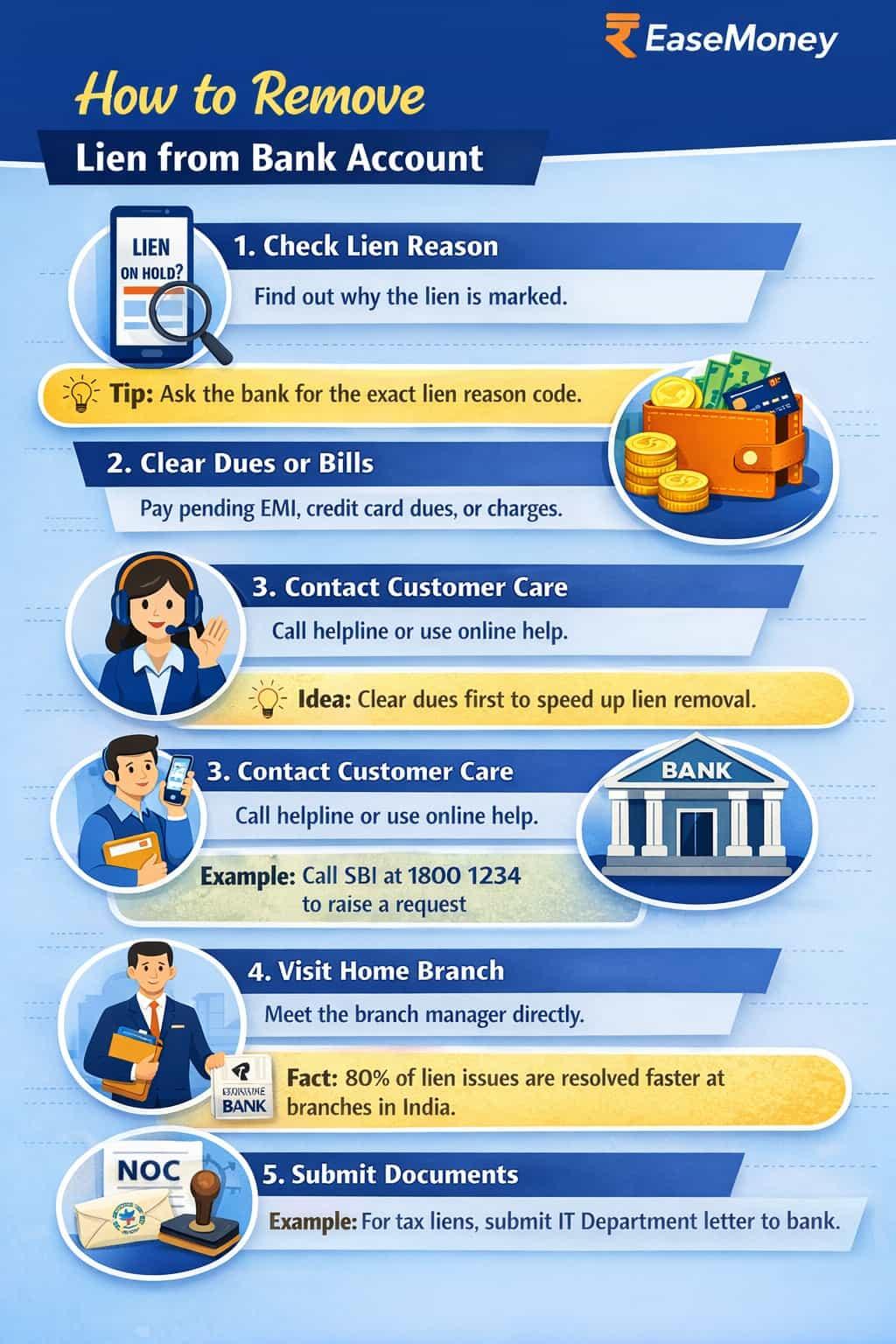

📌 Quick Steps to Remove Lien Amount

💡 Human Tip: Many users panic without checking the actual reason. Small lien amounts like ₹300–₹700 are often linked to debit card AMC charges, minimum balance penalties, or auto-debit processing delays.

📂 Common Lien Categories

UPI reversal, refund processing, IPO ASBA block, failed ATM transaction, or system reconciliation.

EMI overdue, credit card dues, cheque bounce charges, debit card fees, or minimum balance penalties.

Cybercrime complaints, betting transactions, mule account suspicion, court orders, or income tax holds.

⚠️ Important: Investigation-related or legal liens cannot be removed by customer care alone. These usually require branch verification, authority clearance, or legal resolution.

📌 RBI Help: If your bank does not explain the lien properly or delays resolution even after payment clearance, you can escalate the complaint through RBI Sachet.

📖 Read below: Bank-wise lien removal methods for SBI, HDFC, Axis, ICICI, Kotak, Union Bank, and other Indian banks.

Handling Specialized Banking Liens & Legal Holds

1. Cybercrime or Fraudulent Activity Flag

If your account is marked with a “Cyber Cell” or “PMLA” hold, the bank’s internal team has no power to release it.

- The Action: You can call the National Cyber Helpline (1930) or visit

cybercrime.gov.into find your case number. - The Fix: You must provide “Source of Funds” proof to the investigating officer. Only after the police send a De-freeze Order or NOC directly to the bank will the funds be released.

2. Court, Income Tax, or SEBI Orders

These are legal mandates (Garnishee Orders) where the government directs the bank to freeze specific funds.

- The Action: Consult a legal advisor to obtain a Revocation Order or a formal stay from the concerned court/department.

- The Fix: Submit the certified physical copy of the order to your bank’s Legal & Compliance Department.

3. IPO (ASBA) & Mutual Fund Liens

These are “Self-Inflicted” but temporary holds used as collateral.

- IPO/ASBA: Funds are unblocked automatically within 24 hours of the “Basis of Allotment” if you don’t receive shares. If stuck, contact the IPO Registrar (e.g., Link Intime or KFintech).

- Mutual Fund/LAS: If you took a “Loan Against Securities,” the lien stays until the loan is closed. You need a Lien Release Letter from the lender to update your AMC records.

4. Social Security & Government Scheme Liens

Sometimes liens appear due to pending premiums for schemes like Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY).

- The Fix: These are usually small amounts (₹20–₹436). Ensure your account has a positive balance; the bank will debit the amount and remove the hold automatically.

Pro-Tip: If the bank says a “Nodal Agency” placed the hold, don’t waste time at the local branch. Ask for the “Transaction ID” and the “Ordering Authority’s Name” to start your resolution outside the bank.

Timeline for Lien Removal

After clearing dues or submitting documents, banks usually take 24 to 72 hours for automatic updates. If you submitted a manual request through branch, email, or customer support, processing may take 3 to 7 working days.

| Stage | What Happens |

|---|---|

| Day 1-2 | Bank checks payment or submitted documents |

| Day 3-5 | Lien amount becomes zero and balance is released |

| 3-7 Working Days | Manual verification requests get processed |

| 15-90 Days | Cyber Cell or court-related cases may take longer |

Important

Legal or cybercrime-related liens depend on approval from authorities, so delays are common in such cases.

Bank-Wise Lien Removal Time (Realistic Data)

| Bank | Where Lien Shows | Normal Removal Time |

|---|---|---|

| SBI | YONO / NetBanking | 24 hrs – 7 days |

| Axis Bank | Mobile app / Help Centre | 2 – 5 days |

| Kotak Bank | NetBanking → Lien Inquiry | 3 – 7 days |

| HDFC Bank | “Amount on Hold” | 24 – 72 hrs |

| Union Bank | NetBanking / Branch | 3 – 10 days |

Tip: Open your mobile banking app, check the lien section and always check the Available Balance, not the total balance.

Ways to Check the Reason for the Lien

To find out why a lien amount has been marked on your account, first check your bank app, net banking portal, or account statement for remarks linked to the blocked amount.

1. Net Banking or Mobile Banking App

- Open the Account Summary or Balance Details section.

- Look for terms such as:

- “Lien Amount”

- “Blocked Amount”

- “Hold Balance”

- “Debit Freeze”

- Some banks also provide a separate “Lien Details” or “Lien Enquiry” option.

2. Account Statement

- Download your latest bank statement.

- Check the remarks or narration section for:

- “Lien Marked”

- “Amount Blocked”

- “Debit Freeze”

3. SMS and Email Alerts

- Search for messages from your bank, Income Tax Department, Cyber Cell, or other authorities.

- Banks often send alerts when a lien or debit freeze is applied.

4. Visit Your Bank Branch

- If the reason is still unclear, visit your home branch.

- Ask the relationship manager or bank officer for complete lien details and the authority behind the hold.

Common Reasons for a Lien Amount

| Source of Lien | Common Reasons |

|---|---|

| Loan or Credit Card Dues | Unpaid EMIs, overdue credit card bills, overdraft defaults |

| Tax Authorities | Pending Income Tax or GST dues |

| Cyber Crime Investigation | NCRP complaints or Cyber Cell investigations |

| Court or Legal Orders | Court directives linked to legal disputes |

| Internal Bank Issues | Minimum balance penalties or pending KYC updates |

| Investment or Security Hold | IPO/ASBA applications or loans against FD/investments |

Third-Party App Mandates: Sometimes a hold is placed because an auto-pay mandate was set up on a UPI app but failed due to technical issues

Documents Needed for Lien Removal

| Document | Why Needed |

|---|---|

| Aadhaar Card or PAN Card | Identity proof for bank verification |

| Lien Amount Screenshot / SMS | Shows the blocked amount details |

| Payment Receipt or No Dues Certificate | Proof that pending dues are cleared |

| Written Request Letter | Request to remove the lien from account |

| Police or Cyber Cell NOC (if applicable) | Needed in cybercrime or fraud cases |

Important Points

- Name on ID proof should match bank records.

- Mention account number and CRN in the request letter.

- Keep photocopies of all submitted documents.

- For cybercrime liens, banks usually cannot remove the hold without official NOC approval.

Tips to Prevent Future Liens

To avoid future fund freezes in 2026, follow these high-utility habits:

- Maintain Buffer Balance: Always keep ₹2,000 above your Minimum Average Balance (MAB) to prevent “Shortfall” liens from automated bank charges.

- Track Auto-Debits: Review your ECS/NACH mandates monthly. A single EMI or SIP bounce is the #1 cause of immediate account holds.

- Verify Large Inward Credits: If receiving unexpected high-value transfers, keep source-of-fund proof ready to prevent AML (Anti-Money Laundering) flags.

- Update KYC: Complete Re-KYC via the app every 2 years; banks now use “preventive liens” to force compliance.

Frequently Asked Questions

Why does my bank show a lien even after I paid my EMI?

This happens due to backend delay. In most banks, EMI payments sync within 24–72 hours. Tip: keep payment proof and ask branch staff to check the system lien remark.

Can a bank place a lien without informing me by SMS or email?

Yes. Around 60–70% lien cases have no alerts. Banks usually notify only during transactions. Idea: always check available balance, not ledger balance, before UPI or ATM use.

How long should I wait before escalating a lien issue?

Wait 5 working days after clearing dues. If not resolved, escalate to nodal officer. Branch experience shows early escalation reduces resolution time by 40–50%.

Do I need to submit a lien removal letter to the bank?

Yes, in stuck cases. A simple lien removal request letter with account details and payment proof helps branches act faster. Branch managers often insist on it for manual clearance.

What happens if I ignore a lien for many weeks?

Ignoring lien risks auto-debit, credit score impact, or full account freeze in fraud cases. Tip: unresolved liens beyond 30 days often trigger compliance or recovery escalation automatically.

Can a small unpaid charge like ₹300 really cause a lien?

Yes. Banks routinely place liens for ₹200–₹500 charges like AMB penalty or debit card fees. Idea: review quarterly statements to avoid surprise lien marks later.

Hope you liked the content. Explore smart options below 👇

🔥 Recommended