What Is Meant by a Cancelled Cheque?

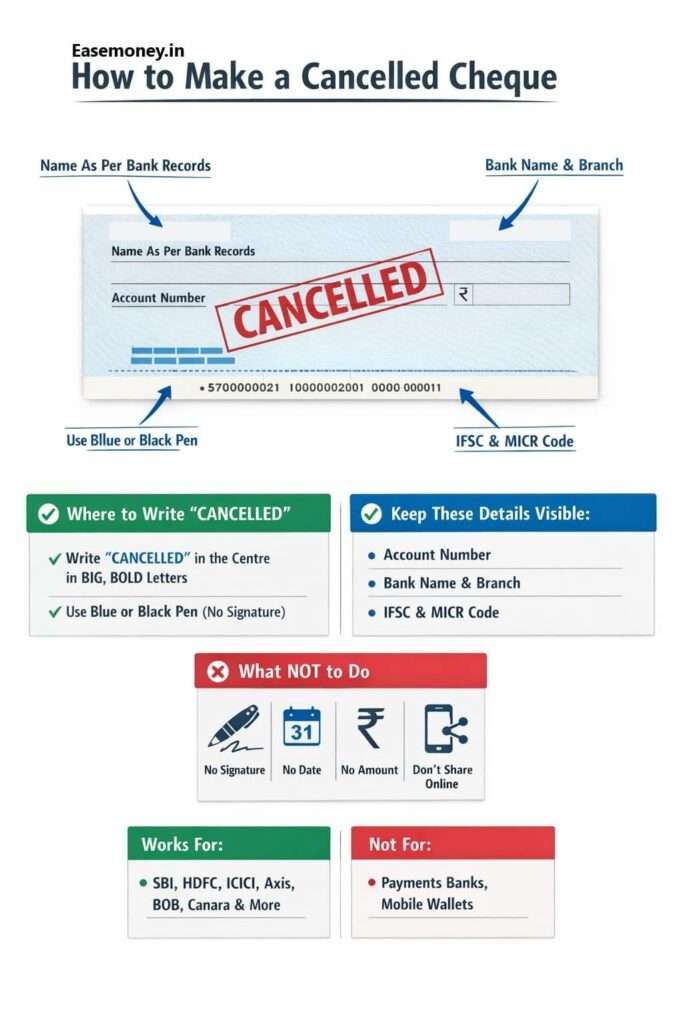

A cancelled cheque is a normal cheque leaf from your active cheque book, on which you write the word “CANCELLED” clearly across the front. Also, it has two parallel lines across it; however, the lines are not mandatory. Those words and lines make it invalid for payments.

You do not sign it. You do not write any amount or date. Once cancelled, the cheque cannot be used to withdraw money.

Its only job is to show your bank account details in a bank-verified format. In india, it is quite popular and required almost daily financial work for KYC, EPF Withdrawal, Utility & Bill Payments, and Government Subsidies.

For example:

If you have an SBI savings account and your cheque has your name printed, the cancelled cheque will show:

- Your name (as per the bank printed)

- Account number

- Bank name and branch

- IFSC and MICR codes

That’s why companies, banks, NBFCs, Fintech Firms, and government offices trust it more than handwritten details. It is mostly required to verify your accurate information as per the printed, bank-issued account metadata. If we simplify it to two or three words, its purpose is verification only.

Who Started the Cheque System and How Cancelled Cheques Came In

Where Cheques Originally Came From (World And India)

The Idea of cheques is not new, as we know. Long before modern banks and paper document-based banks existed, traders in ancient Persia used written payment orders called Sakks. These allowed money to be transferred without carrying cash.

However, the printed and personalised cheque, as we know it today, is a British banking innovation.

In India, formal cheque usage began in 1833, when the Bengal Bank (also called Bank of Bengal, today, we know it as State Bank of India, SBI, changed in 1955) introduced cheque facilities.

At that time:

- Cheques are mainly used by merchants, Big business owners, and British businesses.

- Everything was manual and paper-based.

Between 2008 and 2013, cheque clearing in India changed completely with the introduction of the Cheque Truncation System (CTS).

How Cancelled Cheques Entered the System

The idea of a cancelled cheque is not historical. It developed much later as a procedural tool for:

- KYC

- Salary processing

- Account verification

- Loan and investment onboarding

- Safe and quick basic account details access

It is an administrative requirement, not a payment instrument.

The Role of a Cancelled Cheque in Modern Banking

A cancelled cheque serves one clear purpose: to prove that a bank account exists and belongs to you. It allows institutions and Banks to see verified bank data without risking money withdrawal or any other risks; however, this is still a low-risk factor due to monetary transactions. It is true, that it exposes sensitive personal banking details. It does not authorise payment, withdraw money, or transfer funds.

A cancelled cheque is mainly used for:

- KYC compliance

- Linking bank accounts

- Avoiding payment errors

- Preventing fraud caused by wrong account details

Who Commonly Asks for a Cancelled Cheque

Here’s where real life comes in.

1. Employers & Payroll Teams

Salary credits, reimbursements, and bonus payouts — all rely on correct bank data.

- Payroll errors are expensive and embarrassing.

- Cancelled cheques reduce those errors.

2. Banks & NBFCs

Loans, ECS mandates, EMI setups — banks want the same account for:

- disbursal

- repayment

A cancelled cheque keeps both sides aligned.

3. Mutual Funds & Demat Accounts

AMC systems still prefer cancelled cheques because:

- names match bank records

- IFSC is printed, not typed

- audit teams accept it easily

4. Government & EPF

PF withdrawals, DBT credits, refunds — cancelled cheques are still accepted when systems are not fully auto-linked.

In most real daily life situations is required, for example, when you do a high-value RTGS transfer such as 20 lakh or 50 lakh, it is best practice to ask your beneficiary to share a cancelled cheque. Because RTGS does not forgive mistakes. If ₹50 lakh goes to the wrong account, recovery is slow and painful.

Risk & Misuse

A cancelled cheque cannot be used to withdraw money, but that does not mean it is risk-free. The risk is not theft — the risk is misuse of information. If someone has your cancelled cheque, they can see: Account number IFSC & MICR Your name and bank Using this, a fake ECS or auto-debit mandate attempt can be made. Most banks block it, but the attempt itself causes trouble, reversals, or panic.

Quick Example: Wrong salary or refund credit to your account (if misused by HR or vendor)

That’s why banks treat cancelled cheques like identity proof, not casual documents.

How to Create a Cancelled Cheque That Won’t Be Rejected

In daily Banking life, Many cancelled cheques get rejected for small mistakes. Here’s the correct and safe method, step by step.

Step 1: Take a Blank Cheque Leaf

- Use a cheque from the same account you want to verify

- You have to select a cheque with your name printed (not handwritten)

- You can use an old cheque, older than 3 months, but same bank account, not an issue here.

Step 2: Write “CANCELLED” Clearly

- Use a blue or black pen

- Write in capital letters

- Most important use “LL” in the cheque and spell correctly.

- Draw it diagonally across the cheque (optional)

- Do not cover IFSC or account number

3 Step: What NOT to Do

- No signature

- Not add date

- Do not use a cheque from a closed account

- Do not share publicly on social media

- No amount

- Your payee name (if printed, it’s okay, but you don’t need to write)

- No hiding any information while submitting or uploading to any trusted firms.

- Do not send blurred images

- Do not upload cropped photos

Only the word CANCELLED should be written.

4 Step: Scan or Take a Clear Photo

If uploading online:

- Place the cheque on a flat surface

- Good lighting, no shadows

- Full cheque visible

- Your IFSC and MICR line must be clear

- You can use Document generator Apps for that to capture it as a printed copy.

Practical Tips That Reduce Rejection with Infographic

- Do not fold the cheque

- Avoid overwriting

- Do not use a pencil

- Use the original cheque, not a photocopy (unless asked)

Bank-Wise: How Cancelled Cheques Are Usually Created

All regular banks follow the same cancelled cheque method, but cheque availability differs.

Cancelled Cheque by Bank (General Practice)

| Bank | Cheque Book Availability | Cancelled Cheque Method |

|---|---|---|

| SBI | Issued for savings & current accounts, You can get 1 free 25 pages ever year. apply via YONO App | Write CANCELLED on cheque leaf |

| HDFC Bank | You can use internet banking or request via Mobile App. | Same |

| ICICI Bank | ICICI Mobile Banking App, Safest option. | |

| Axis Bank | Available via branch/app | |

| Bank of Baroda | Issued for savings accounts | |

| Union Bank | You can WhatsApp Banking number 9666606060, say hi and order it directly. | |

| Canara Bank | Cheque book available | |

| Paytm Payments Bank | You can download a Photo of cancelled cheque in the Paytm App |

There is no special “cancelled cheque” issued by banks. You always create it yourself.

Read: How Do You Write a Cancelled Cheque for Your Bank Account? – Top 8 Banks Image Example

What About Payments Banks and Small Finance Banks?

This is where confusion starts.

Payments Banks

Payment banks do not issue cheque books.

Examples:

- India Post Payments Bank, IPPB, recently in July 2020, discontinued inward and outward cheque services for all customer types.

- Airtel Payments Bank

- Paytm Payments Bank

For these accounts:

- Cancelled cheque is not available

- Institutions accept alternatives like:

- Bank confirmation letter

- App-generated account details

- Passbook or statement

Small Finance Banks

Most small finance banks do issue cheque books, but sometimes only after full KYC.

If a cheque book is issued, the cancelled cheque method remains the same. you can apply a cheque book via Netbanking or mobile app. it also works in NEO Banks, such as NiyoX or Jupiter Money.

Alternatives to a Cancelled Cheque (When You Don’t Have One)

Many organisations now accept alternatives, especially for digital users.

Common Accepted Alternatives

- Bank passbook (first page)

- Bank statement (PDF)

- Bank-issued account confirmation letter

- Cancelled cheque + self-attestation note

- Online account verification via net banking

However, a cancelled cheque is still preferred because:

- It is simple

- It is bank-printed

- It reduces manual errors

FAQs

Is it okay if my cheque doesn’t have my name printed?

Sometimes yes, sometimes no. Many fintech apps accept it, but traditional banks and HR teams prefer name-printed cheques to match records without extra clarification emails. however, you don’t need to write it. it will works as per rules.

Should I sign the cheque after writing CANCELLED?

Never. A signed cheque, even cancelled, raises red flags. Many institutions will reject it outright because signatures introduce unnecessary risk.

Can a scanned photo from my phone get rejected?

Yes, often. Common reasons are shadows, cropped MICR line, or blur. If possible, scan it flat or click in daylight on a plain background.

Why is cancelled cheque still used in 2026 with UPI everywhere?

Because not every system talks to each other. Payroll, audits, and government processes still rely on simple, visual bank proofs that work everywhere without tech dependencies.

Is a bank statement safer than a cancelled cheque?

Safer for data, yes. But slower to verify. Cancelled cheques remain popular because they’re one-page, bank-printed, and easy for humans to validate quickly.

Can someone withdraw money using my cancelled cheque?

No. Money can’t be withdrawn. But careless sharing can expose your account details. Treat it like an ID proof — share only with trusted banks, employers, or official portals.

What do banks or companies actually do with my cancelled cheque?

Banks use a cancelled cheque only to confirm your bank details. It’s never used for payments. It’s stored like KYC proof and usually kept only until verification or audit checks are completed.

Can I use the same cancelled cheque multiple times for different purposes?

Yes. One cancelled cheque can be reused for multiple verifications like salary, MF, EPF, or loans, as long as the account remains active and details haven’t changed.

Does the cheque series number or leaf number matter in a cancelled cheque?

No. Banks and companies ignore cheque numbers for cancelled cheques. Only printed details like account number, IFSC, and name are checked during verification.

Hope you liked the content. Explore smart options below 👇