Let’s start with a Quick Fact – The bank records a cheque number before the cheque book reaches your hands. Even if you never use that cheque, the bank already knows it exists, who it belongs to, and what should happen if it ever appears.

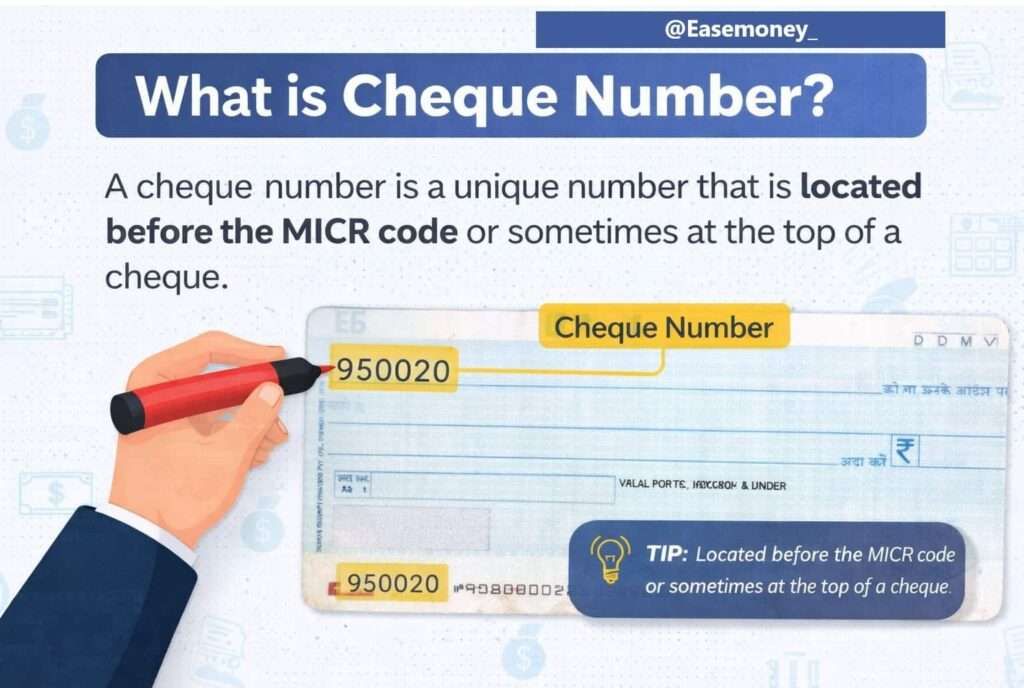

What is a cheque number?

A cheque number is a unique serial identity given to one specific cheque leaf. In your chequebook, every leaf has 1 unique number. In banking terms, a cheque number represents one-time permission to move money. It is a 6-digit (sometimes 7-digit) number. After the RBI rules, it was fixed at 6 digits for almost all banks in india.

The primary focus of that is simple: it helps both the account holder and the bank track to verify individual transactions. It is only printed on each leaf, not on the cheque book or bank statements.

As per the IndusInd Bank summary blog, the cheque number is part of the Magnetic Ink Character Recognition. It is printed alongside MICR by special magnetic ink. This allows high-speed sorting and electronic processing by bank machines. It reduces all the manual errors and makes CTS faster.

Let’s go with an Example – Suppose your chequebook is 50 pages, and the cheque numbers: The first leaf is 734201 to and the last leaf 734250.

Cheque number 734219 means:

- It belongs only to your account

- It can be used only once

- Once used (paid or bounced), it can never be reused

Even if:

- The amount has changed

- The payee name is different

- The signature looks similar

The system still identifies the cheque only by its number.

My Quote here – Most people notice the money written on a cheque. Banks notice the number. But,Years later, when memories fade, and ink loses colour, only one thing still speaks clearly inside banking systems, the cheque number. It is digital as well as paper.

Decoding the cheque number: what each digit means

Unlike account numbers or MICR, cheque numbers don’t encode any of your personal information digit by digit. Their meaning is contextual, not mathematical. But, as I already said, it’s part of the MICR line at the bottom.

What matters is:

- the sequence

- the range

- the mapping

This tells the bank:

- It falls within an issued series

- It belongs to a specific cheque book

- It is linked to a specific account

Banks do not “read” cheque numbers — they look them up.

That’s why two banks can issue the same cheque number without conflict. Uniqueness exists within the bank’s internal system, not nationally.

Confusion Solved: Cheque routing number is it same or different

In India, there is no separate cheque routing number like in the US. The cheque number is different from the routing number. The simple explanation for you is that in India, the equivalent function for electronic transfers is performed by the IFSC Code and for cheque processing by the MICR Code.

The routing number does not work in the Indian Banking system. Also, let me clarify it, the cheque number does not route the cheque, but it identifies the cheque.

This difference matters, especially for Indian users reading foreign content.

Do different types of cheques affect the cheque number?

The cheque number never changes, but how banks treat it changes. If you have a bearer, order, account payee, post-dated or any other cheque, the cheque number remains the same and single-use. The only change that happened here is the instruction layer. Your Bank first validate the cheque number, then the cheque type rules. This is how CTS works in india.

Does cheque number expire or become invalid over time?

Cheque numbers themselves do not expire, but their usability depends on cheque validity.

- A cheque leaf is usually valid for 3 months from date written

- After that, the cheque number remains in system but cannot be used for payment

👉 So the number stays active in records, but the cheque becomes unusable.

The Difference: Transaction ID vs cheque number

In very simple words, the A cheque number creates the event. A transaction ID records the outcome.

- Cheque Number: It exists before any transactions happen; it works chequebook by chequebook. not transaction by transaction.

- Transaction ID: It is generated after the transaction is initiated or created, and it identifies the result, quick example for you – failed, successful or pending.

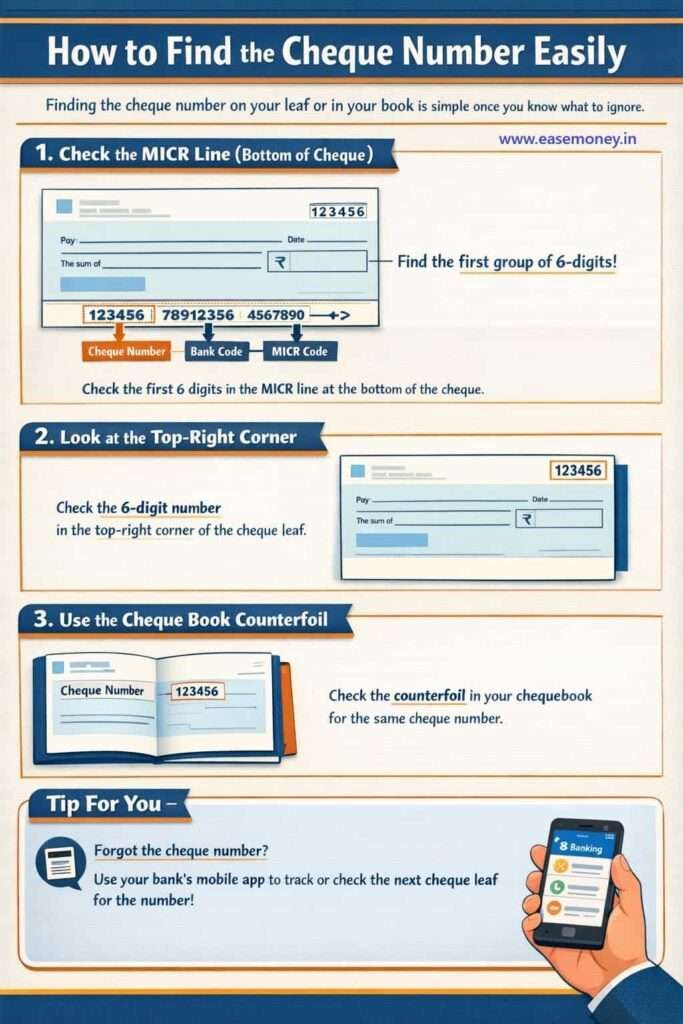

How to find the cheque number easily

Finding the cheque number on your leaf or in your book is simple once you know what to ignore.

1 Step – Check the MICR line (bottom of cheque)

In India, all banks have 1 strict printing. At the bottom, you will see a string of numbers in magnetic ink. To get your number, check the first group of 6-digits. It is your cheque number. This is just before the MICR, which is 9 digits.

2 Step – Look at the top-right corner

This is another option you will have, check the top right corner of the leaf. not IFSC code, but a 6-digit printed or not.

3 Step – Use the cheque book counterfoil

Each cheque leaf has a counterfoil printed with the same cheque number. This exists because humans forget; systems do not. Most Indian banks offer a good personalised chequebook with a good counterfoil.

Tip For You – if you submit the cheque but later forget the cheque number, you can use your bank mobile banking app to track it or check your chequebook next leaf number to calculate it.

Which is the cheque number on a cheque leaf or cheque book?

This confusion exists because a cheque contains multiple numbers, codes, symbols, and more. So, let’s divide all numbers one-by-one to make like easy for even small kids. Here are the numbers you see on a cheque –

- Cheque number

- Short (6–7 digits)

- Top-right corner or bottom

- Unique to the leaf

- Near to MICR and white background, simple black digits.

- Account number

- Longer

- Identifies where money comes from

- You will find it in the box, near the signature section.

- MICR code

- Printed at the bottom, and it is longer than the cheque number, it is around 9 digits, it tells all about the cities, branch, and bank code.

- Identifies bank + branch

- IFSC code

- Printed or prefilled at the top of the cheque, near the address of your bank branch.

- Used for electronic transfers

- CIF number (not always printed)

- Identifies customer relationships

- It is usually not printed on leaves, but some banks print it on the chequebook front page.

History: When did cheque numbers start in India?

Cheques existed in India even before independence, but cheque numbering was not always central at first.

- Before the 1950s: All the cheques went through Manual ledgers, and there was minimal reliance on numbers.

- 1960s–1970s: Growing use of serial numbers

- 1980s: Public sector expansion made numbering important

- Late 1990s: MICR clearing increased dependency, this push the all cheque number system in real.

- Early 2000s: Core banking systems made cheque numbers mandatory, this is the final stage when cheque numbers became too important for track or identity.

- 2010 onwards: CTS made cheque numbers digitally critical

From this point, a cheque without a valid number effectively became unusable.

How cheque numbers work behind the scenes

1 Step – The Series Generation Stage

- Your Bank generates a range of cheque numbers for each chequebook you applied for via online or a branch. such as 910201 to 910225

2 Step – Account mapping

This range of numbers is mapped internally with your bank account and your home branch. Bank Internal system scan and says Cheque 910219 belongs only to this account.

3 Step – Status initialisation

Every cheque number starts with: UNUSED tag, but later, as per the transaction that happens by you, it converts that.

4 Step – The cheque is issued by you

Once deposited by the payee, the cheque is scanned in the CTS modern system by Indian Banking.

5 Step – System validation

The system checks:

- Does this cheque number exist?

- Is it unused?

- Is it linked to this account?

6 Step – Instruction checks

Only after number validation, such as MICR and Cheque number:

- signature

- date

- balance

- cheque type

7 Step – Outcome tagging

Cheque number is permanently tagged as:

- PAID

- RETURNED

- STOPPED

This tag never disappears.

What happens if a cheque number is invalid or already used

The system does not “try again” — it rejects immediately.

- If the cheque number is not found in issued series → rejected

- If already marked as PAID or STOPPED → rejected

- If cheque book is closed or blocked → rejected

Banks rely on cheque number first. If this fails, other checks (signature, balance) are not even processed.

When a cheque number is required in daily life

A cheque number is really important when money via cheque needs to be traced, stopped, proven, and disputed. This is everyday work and required at these stages for you and your bank.

- To track cheque payments

- For cheque return/bounce reference

- For bank records and dispute resolution

- If you lose a cheque or change your mind, your bank will require the cheque number to stop payment only that leaf.

- Banking forms, such as sometimes it require Refund processing.

- When you fill out the deposit slip at the branch, it must be required.

- Needed while filling a request or generating complaints

FAQs

How to confirm a cheque number?

The safest way for you is to match the top-right number with the counterfoil or MICR line. If all three align, that cheque number is correct and uniquely tied to your account.

What does “VOID” mean on a cheque?

“Void” means the cheque’s payment permission is cancelled, not its identity. The cheque number, account details, and MICR remain valid for verification and KYC purposes.

Is a cheque number always 6 digits in India?

Mostly yes, but not always. Indian banks commonly use 6 digits, while some newer cheque books use 7-digit numbers. RBI mandates uniqueness, not a fixed length.

Can two cheques have the same cheque number?

Yes across different banks, but never within the same bank system for the same account. Internally, each cheque number is mapped uniquely and cannot repeat.

What happens if I write the wrong cheque number on a form or deposit slip?

The bank may fail to trace your cheque, delay processing, or ask for clarification. Wrong cheque numbers don’t move money, but they definitely slow resolution.

Does a cancelled cheque still have a cheque number?

Always. Cancellation only blocks payment. The cheque number still exists and is often the reason cancelled cheques are accepted as proof of account ownership.

Can I stop payment without knowing the cheque number?

You can, but it’s risky. Without the exact cheque number, banks may block a wider range, or ask for written confirmation to avoid accidental misuse.

How to Get the HDFC or SBI cheque number?

State Bank of India and HDFC cheque numbers are usually 6 digits, printed clearly on the bottom of the cheque and in the MICR line with white background, it almost same as other banks do.

Hope you liked the content. Explore smart options below 👇